Personal Wealth Management / Market Analysis

Thoughts on the Oil Bounce

Oil markets appeared to make too much of two small news items Monday.

Oil prices jumped for a third straight day on Monday, capping a 23.9% rise in WTI crude since 8/26.[i]Headlines cited two developments to explain Monday's jump: OPEC's claim that it "stands ready to talk to all other producers" about maybe doing something to achieve "fair and reasonable" prices and a downward revision to the US Energy Information Administration's estimate of year-to-date US output. Read past these soundbites, however, and it doesn't appear anything has materially changed. We suspect oil's rise is another dead cat bounce[ii], not the start of a sustained rebound, keeping Energy firms pressured for the foreseeable future.

Over the past few months, investors have seized on any chatter about an emergency OPEC meeting to address weak oil prices as a harbinger of production cuts. Monday's missive-in the introduction to OPEC's August bulletin-did not address any such meeting, and OPEC remains slated to meet next on December 4. Nor did the statement contain any hints about OPEC cutting output, and it seems beyond speculative to translate any part of it as "will slash production to reduce the global supply glut." Here is the salient passage (boldface ours):

"As the Organization has stressed on numerous occasions, it stands ready to talk to all other producers. But this has to be on a level playing field. OPEC will protect its own interests. As developing countries, its Members, whose economies rely heavily on this one precious resource, can ill afford to do otherwise. Cooperation is and will always remain the key to oil's future and that is why dialogue among the main stakeholders is so important going forward. There is no quick fix, but if there is a willingness to face the oil industry's challenges together, then the prospects for the future have to be a lot better than what everyone involved in the industry has been experiencing over the past nine months or so. Only time will tell."

That sounds an awful lot like the status quo to us. As does a line elsewhere in the brief acknowledging a need to "ride out the storm" and wait for modestly rising demand to boost prices. This is all entirely logical when you consider that aside from Saudi Arabia, few other producers can afford to dial back output given their governments' budgets hinge on oil revenue. For all the excitement over Russian "President" Vladimir Putin and Venezuelan "President" Nicolás Maduro's forthcoming discussion on "possible mutual steps" to boost prices, neither country is in any position to sacrifice oil revenues at the moment. Not when Venezuela has chronic food and toilet paper shortages and Russia faces double-digit inflation. We reckon that meeting would go something like: "Hey I know, why don't you cut output?" "No, why don't you do it?" "No, you do it." "No, you do it." "No, you do it!" Lather, rinse, repeat.

Plus, OPEC-particularly Saudi Arabia-seems to want to maintain market share. We strongly suspect they wouldn't agree to cut unless US producers agreed to cut as well, and that is awfully hard to envision. US producers operate in a free market, with no cartel above them and no government production quotas. The laws of supply and demand govern output in the U-S-of-A-and, for that matter, in all non-OPEC countries with largely private oil industries. Heck, just today, one big Danish firm launched a new project in one of the UK's North Sea fields, emboldened by recent tax industry tax breaks there. They're pouring £3 billion into new offshore rigs and plan to start pumping by 2019. Does that seem like a big cutback?

As for the EIA estimates, we don't really see a there there. Yes, the agency revised down its year-to-date estimates for monthly US production by an average of 70,000 barrels per day. But that is a very slight reduction, and it is due entirely to methodology changes EIA Administrator Adam Sieminski claims "represent a significant improvement" over prior estimates. Instead of basing estimates on tax filings and other stats provided by state agencies (a dataset the EIA calls "lagged and incomplete at the time of initial publication"), they're surveying producers directly to obtain more timely and accurate figures. June's estimates are the first under the new system, but they revised figures for January through May-but not prior years, creating a perhaps artificially high benchmark for year-over-year comparisons. They also haven't finished revising data for West Virginia and Oklahoma yet, so expect a bit more fluctuations in the coming months.

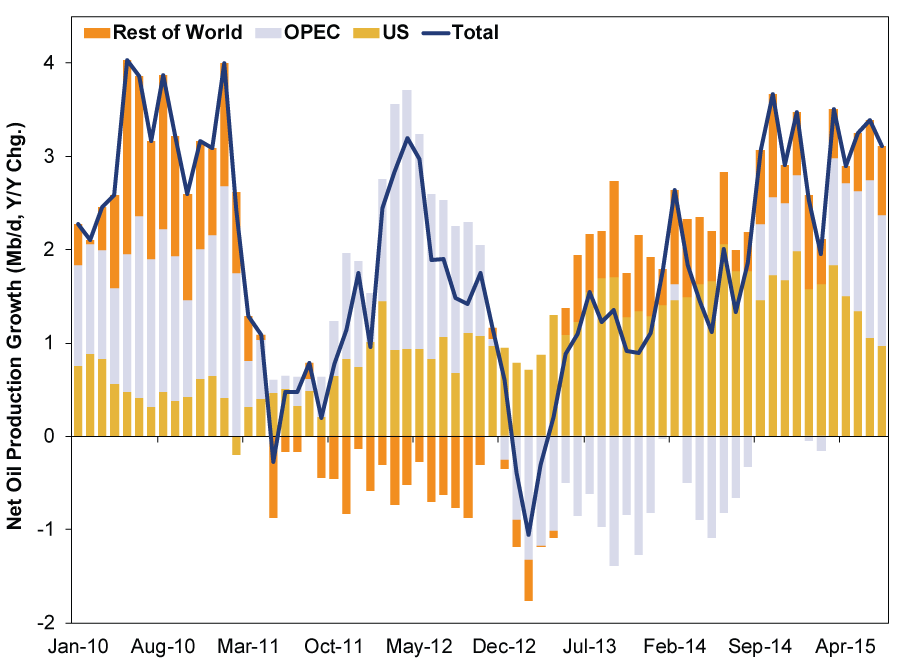

All that said, even with the EIA's revision, global production is growing swiftly. Exhibit 1 shows the year-over-year change in monthly production, in millions of barrels per day. Aside from a brief hiccup in July, production gains are well ahead of the last two years, with OPEC pumping plenty and US growth largely outpacing the shale boom's heights.

Exhibit 1: Global Monthly Net Oil Production Growth

Source: FactSet, as of 8/31/2015. Year-over-year change in monthly net oil production, millions of barrels per day, January 2010 - July 2015.

Meanwhile, as OPEC pointed out, global demand is still growing-just not as fast as supply. Until that changes, oil prices probably remain quite low, though continued volatility wouldn't surprise. Pundits will probably continue reading into OPEC proclamations, but we'd advise readers to watch what producers do, not what they say. Markets move most, over time, on actual supply and demand, not misinterpreted jawboning.

HT: Bradley Rotolo

[i] FactSet, as of 8/31/2015. WTI crude spot price, 8/26/2015 - 8/31/2015.

[ii] This is a technical term for "probably temporary bounce off a bottom with no fundamental underpinning," and it kinda creeps us out, too. DISCLOSURE: We like cats.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today