Personal Wealth Management / Financial Planning

Three Considerations for Master Limited Partnership Investors Now

What to think about after a rocky two years for MLP investors.

Master Limited Partnerships-largely, Energy pipeline companies-have endured a rough road over the last two years. Photo by Gregor Bister.

August 29 marked exactly two years since the Alerian Master Limited Partnership (MLP) Total Return Index hit 1896.217, its record high.[i] The intervening 24 months have been quite a rollercoaster ride for those who own these securities, and probably not a particularly fun one. After reaching its zenith, the Alerian MLP Index fell a massive -58.2% through February 11, 2016.[ii] Since then, it has rallied back 59.4%, but remains down -33.3% from its peak.[iii] If you hold MLPs, all the back and forth may have you wondering what to do now.[iv] While we can't answer that question outright without knowing you or your circumstances, we can provide some insight into the critical considerations you ought to weigh.

For those less familiar, MLPs were created by Congress in the 1980s in an effort to boost private investment in energy infrastructure-most specifically, pipelines. To attract capital, Congress passed a law allowing for a publicly traded security with limited partnership-like tax benefits-bringing more liquidity and fewer restrictions and thus, more investors. MLPs aren't taxed at the corporate level. Instead, they must distribute at least 90% of profits to their investors, called unitholders, in dividend-like payments. Since taxes don't detract from profits, MLPs often kick off relatively high yields to unitholders.

The last sentence is a primary reason their popularity soared before 2014's oil crash-given low interest rates, financial-product salespeople found a very receptive audience for assets sporting a high yield. Besides, as the shale revolution became more widely known, folks became increasingly bullish about the sector. That's what brought us to this point, where many individual investors have been suffering through a massive downturn in the Energy industry, which directly dinged MLPs.

But what to do now, two years from the high, is the question du jour. Without further ado, here are three points we believe MLP owners should assess today:

1. Why did you buy this security?

This may seem basic, and even perhaps a bit backward looking. But it is a key consideration, as this "why" question can determine whether your thesis to own the MLP is intact.

There are viable reasons to buy MLPs. Perhaps one anticipates rising oil prices and production will lead to bigger pipeline fees and distributions. (That is a valid reason to own, although we don't believe it's very timely today.) But you must be honest with yourself. All too often, the real answer is what we stated above: Investors snapped these up seeking "yield," thinking high dividends made them a "safe" way to fund the cash flow they needed through distributions-as a replacement for (or alternative to) low-yielding bonds.

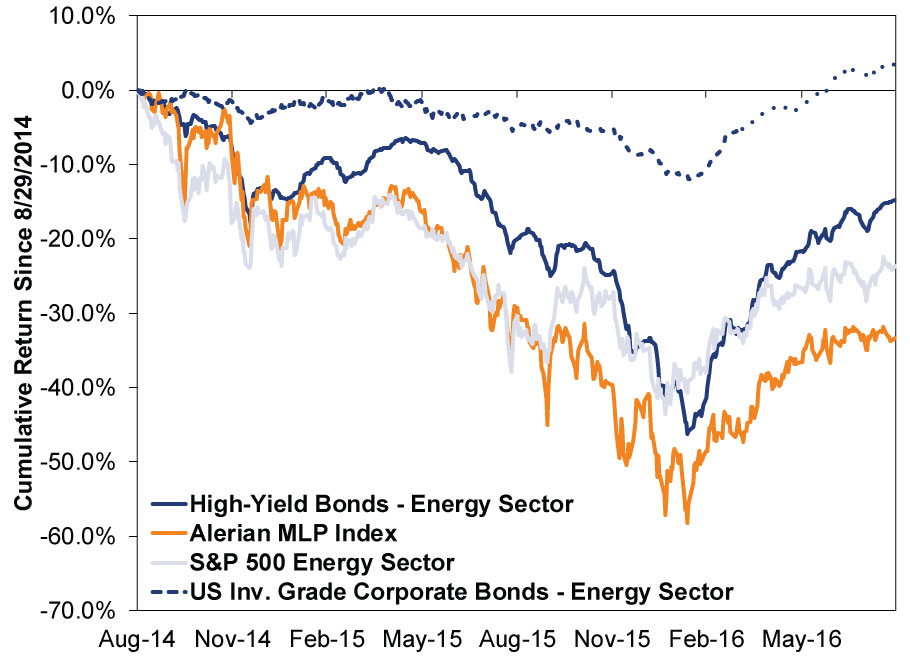

Unfortunately, this pitch was never very accurate. MLPs are listed like stocks. You trade them like stocks. And their prices move like stocks. They are highly correlated to Energy stocks. You know what they say about ducks. When considering your asset allocation-the mix of stocks, bonds, cash and other securities you invest in-it's a mistake to presume an MLP can replace a bond. Their volatility characteristics are totally different! Recent history puts an extra exclamation point on that. Consider Exhibit 1, which shows MLP returns since 2013 versus Energy sector high-yield bonds, high-yield bonds excluding Energy and Energy investment-grade corporates. Nothing bond-like about them!

Exhibit 1: MLPs Can't Replace Bonds

Source: FactSet, as of 8/29/2016. Total returns of Alerian MLP Index, S&P 500 Energy Sector Index, BofA Merrill Lynch US High Yield Energy Sector and US Investment Grade Corporate Energy Sector, 8/29/2014 - 8/29/2016.

2. Where do you think oil prices are heading?

As noted above, before oil prices crashed-and even after the initial punch in late 2014-it was fashionable for many to argue MLPs weren't oil-price sensitive, since they only transport oil from point A to point B. We never thought that accurate, but unfortunately, many investors bought into this logic. So much so that we still occasionally hear it today. Trouble is, it's false.

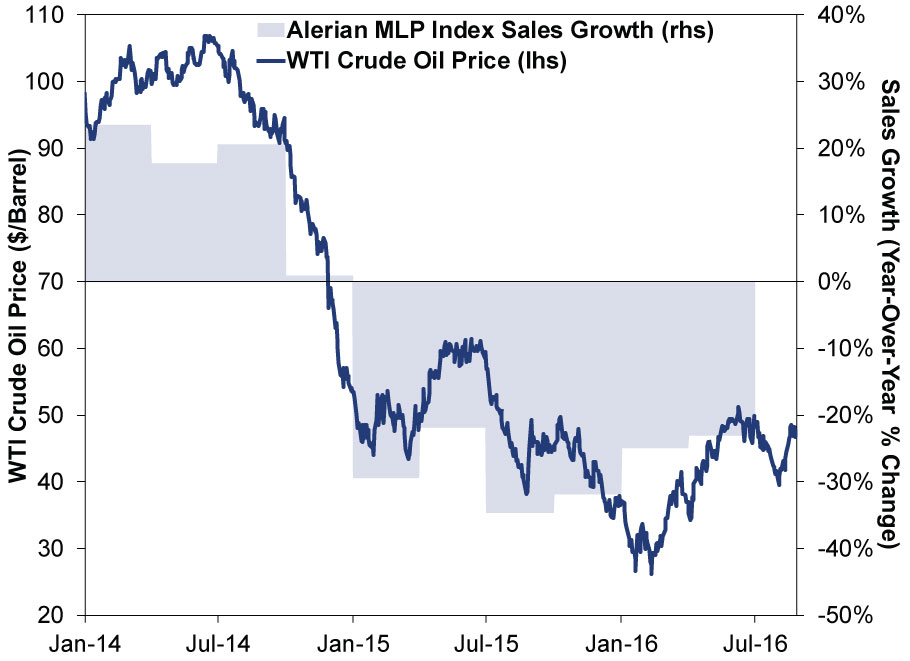

MLPs are directly exposed to oil prices, as the last two years' experience should make clear. Exhibit 2 shows MLPs' revenue growth fell off a cliff during mid- to late-2014. Oil prices crushed pipeline firms' sales.[v]

Exhibit 2: Alerian Energy MLP Sales Growth Slides With Oil Prices

Source: FactSet Earnings Scorecard, as of 8/29/2016. Alerian Energy MLP Index blended sales growth rate, Q1 2014 - Q2 2016. Q2 2016 is shown with 39 of 40 constituent companies reporting.

Oil and gas producers pay fees to pipeline operators to move their products from point to point. When oil prices are high, producers are cash-rich and willing to pay higher fees. They'll also aim to boost output, generating greater volumes and higher demand for transportation services like pipelines.

When oil prices crash, producers are pinched and look to cut costs in any way possible. Hence, when contracts renew, producers are very likely to see this as an opportunity to negotiate a more favorable deal for them-and less favorable for the pipeline. Some existing contracts even set variable fees based on oil prices. It is illogical to presume firms connected to oil prices in this fundamental fashion won't be dinged when oil drops more than 50%.

(A related, albeit tangential, point: Where you think oil is headed shouldn't hinge on where it was.)

3. What share of your portfolio is invested in Energy?

Once you recognize MLPs for what they are-a subset of the Energy sector-it's important to cast them in the proper light. Many investors we've come across draw a false distinction between, say, publicly traded oil firms and MLPs. The result: Portfolios with 15%, 20%, 30% or even more in equity securities directly linked to oil.

The Energy sector comprises only 6.6% of the MSCI World Index and 7.1% of the S&P 500, as of August 29, 2016.[vi] Even if you are bullish on Energy and expect MLPs and Energy stocks to outperform the broader market going forward (again, we don't expect that presently), putting a very large weight in the category is taking on extreme risk-eschewing sector diversification. If your combined weight (stocks plus MLPs) exceeds this mark greatly, that's a call to action for you, in our opinion.

[i] Source: FactSet, as of 8/29/2016.

[ii] Source: FactSet, as of 8/29/2016. Alerian MLP index with reinvested distributions, 8/29/2014 - 2/11/2016.

[iii] Ibid. 2/11/2016 - 8/29/2016.

[iv] Not sure if what you own is an MLP? Check your holdings against this list. These are the MLPs comprising the Alerian Index discussed herein. This isn't all MLPs, but it is quite close.

[v] We show revenues here because earnings data are subject to greater skew through mark downs, cost cuts and more. Revenue growth is a more clean way to see the impact of falling oil and gas prices. That being said, earnings are down huge since 2014 as well.

[vi] Source: FactSet, as of 8/29/2016. Energy sector share of MSCI World and S&P 500 by market capitalization.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today