Personal Wealth Management / Market Analysis

UK OK

Not much has changed from a year ago, except more clarity Brexit doom-mongers are wrong.

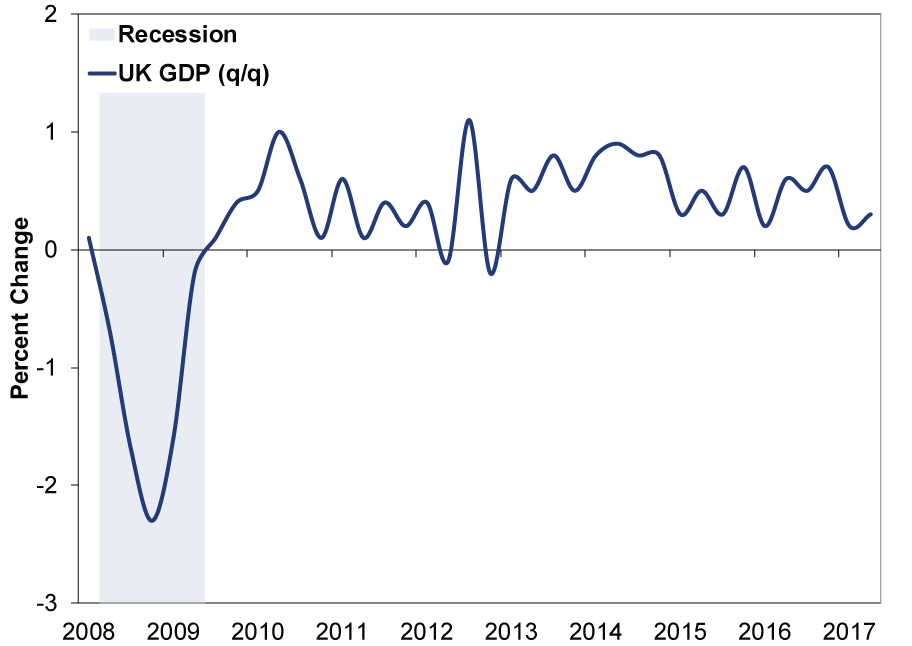

A month after the UK Office for National Statistics (ONS) released its preliminary Q2 GDP estimate-up a ho-hum 0.3% q/q-their second estimate, released last week, stayed the same. We grant you, not very exciting. But to jazz it up, the media provided some context: The G7's laggard! First half growth worst in five years! No contributions from trade or investment! This would have you believe Brexit, the pound's fall, rising inflation-take your pick-is finally biting the UK economy. However, we believe reality is better than sentiment supposes-a low bar for the economy to clear and boost stocks.

Lost in the doom mongering: Q2's 0.3% q/q (1.2% annualized) growth accelerated from Q1's 0.2% (0.9% annualized).[i] (Exhibit 1) Yes, it's tiny and just one quarter, but it illustrates the sentiment disconnect. Pessimists bemoan the UK's two consecutive lackluster quarters-a big slowdown from last year-to wring maximum gloom. Q1 growth did slow substantially from Q4's 0.7%. But that happened from Q4 2015 to Q1 2016, too. Pre-Brexit! This may just be normal data variability, not a Brexit-induced recession developing.

Exhibit 1: UK GDP Fluctuates

Source: Office for National Statistics, as of 8/29/2017.

While headline GDP sped up a tick, consumer spending slowed-from Q1's 0.4% q/q rise to just 0.1%.[ii] Media assumes this is damage wrought by weak-pound-driven inflation, but the slowdown stemmed mostly from a drop in transport spending after a strong Q1. The likely culprit was an April 2017 start to a new Vehicle Excise Duty, which pulled spending forward. That new tax is a one-off, non-Brexit-related event. But weak consumer spending has been an (overwrought) narrative all year. For example, the latest British Retail Consortium report insists UK consumers are tapped out, pointing to non-food retail sales declines in the three months through July. But the vehicle tax could explain this trend, too. Singling out weak parts of a healthy sales report on the whole to score Brexit-related doom points strikes us as misperceived.

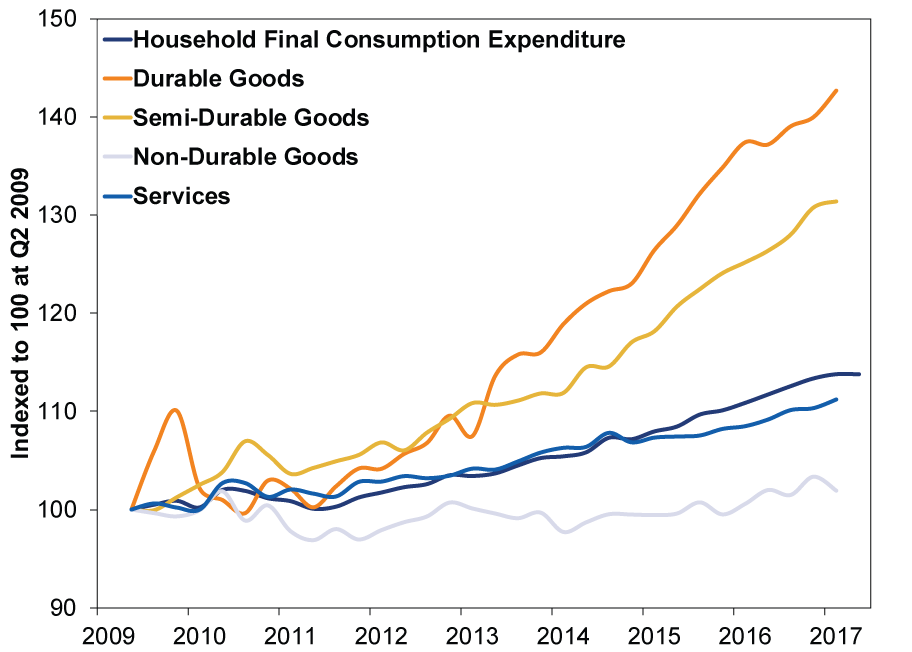

For investors attempting to construct how the entire economy is faring, it helps to break down the data in more detail. Do so, and it appears consumer demand is hardly struggling. Although Q2 expenditure details haven't been released yet, we can see general trends through Q1. (Exhibit 2) Durable goods (e.g., cars and furniture) and semi-durable goods (such as clothing) are up over 30% in volume terms from recession's end through March. Non-durable goods (like food) by volume have been trending higher since 2014 but aren't appreciably higher than 8 years ago. Spending on services-54% of consumer spending-while lagging the last few years, remains a reliable growth engine and has revved higher in recent quarters. But, Q2 ended two months ago. For fresher data, the ONS reports July retail sales rose 0.3% m/m, and the "3 month on 3 month estimate"-which better shows the trend-rose 0.6%. Q3 is off to a decent start.

Exhibit 2: UK Consumer Spending and Major Subcomponents

Source: Office for National Statistics, as of 8/29/2017.

In addition to slow consumer spending, pessimists cite weak industrial production growth and faltering contributions from trade-purported evidence the pound is not only holding back consumption, but also isn't helping manufacturing and exports the way it supposedly should. But it was always a myth that weak currencies are good for factories. Japan has been busy teaching that lesson for most of the last six years, though many pundits have yet to notice. Multinationals import many components, and weak currencies raise those costs. Moreover, this viewpoint centers on the contribution from net trade, a meaningless statistic. Look at total trade instead: Imports and exports each rose 0.7% q/q in Q2. Imports subtract from GDP, but they represent domestic demand. So rising imports is another counterpoint to the tapped-out Britain narrative.

Beyond GDP, the UK purchasing managers' indexes (PMIs) provide more forward-looking views on economic fundamentals and how they're trending-in the right direction. The July services PMI rose 0.4 to 53.8 and just-released-today August manufacturing rose 1.6 to 56.9.[iii] The July composite PMI-combining services and manufacturing-rose 0.3 to 54.1.[iv] While crawling GDP might seem to contradict speedyish PMIs, higher PMIs have never automatically translated to faster GDP growth rates. PMIs measure growth's breadth not magnitude, but all being above 50-along with their forward-looking new orders subindexes-signals ongoing UK business activity expansion. The vast majority of the UK economy is faring fine. While PMIs aren't infallible, we've found them a reliable guide to near-term economic activity, when taken in conjunction with other indicators.

Looking ahead, financial conditions are conducive to further growth. The UK yield curve is positively sloped-long-term lending rates are higher than their short-term deposit costs. That means loan growth is profitable, an incentive to lend. In response, private sector loans are ramping up. As these funds circulate, money supply is rising 6.0% year-over-year.[v] Rapid money supply growth suggests faster economic growth lies ahead. Pundits miss this. (Plus, with money supply growth so swift, it's a wonder inflation is as low as it is.)

Naysayers have come up with all sorts of reasons why the UK economy is headed off on a stretcher, but the further they delve, the less credible they look. However improbable to doomsayers, in our view, the UK economy's fundamentals remain on solid ground. For investors, when pessimism proves ill-founded, stocks usually benefit.

[i] Source: UK Office for National Statistics, as of 8/31/2017.

[ii] Ibid.

[iii] Source: IHS Markit, as of 9/1/2017.

[iv] Source: Trading Economics, as of 9/1/2017.

[v] Source: Bank of England, as of 8/28/2017. M4 excluding other intermediate other financial corporations (OFCs), 12-month percent change, June 2016 - June 2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30 -

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today