Personal Wealth Management / Market Analysis

US Economic Update

A smattering of August and September data demonstrates fears of a US recession immediately ahead are likely overdone.

(Note: A video version of this updateis also available on Fisher Investments' YouTube channel.)

A smattering of US economic data for August and September suggests the economy remains stronger than many believe, and in our view, the current expansion seems likely to continue.

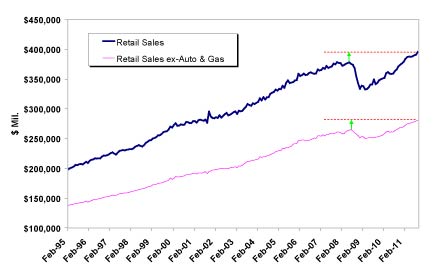

Once again, consumers proved they’re healthier than many perceive as retail sales rose 1.1% month-over-month (7.7% year-over-year)—beating expectations, accelerating from August’s upwardly revised 0.3% growth and logging a new record.

Exhibit 1 shows headline and core (ex-auto and gas) retail sales since 1995. Interestingly, there has been less retail volatility overall in this expansion than in the prior cycle.

Exhibit 1: US Retail Sales Volume (Nominal)

Sources: US Census Bureau, Thomson Reuters

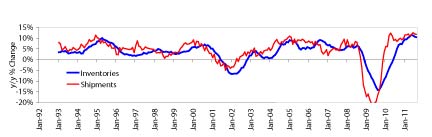

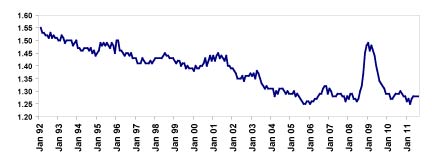

Business shipments (sales) rose 0.3% month over month (11.8% year over year) in August, while business inventories rose 0.5% (10.5% year over year) in August—higher than expected. (July’s inventories were also revised higher from 0.4% to 0.5%.) Though inventories grew slightly faster than sales (partly reflecting July’s large push of sales from manufacturers to wholesalers), both remain above the peak annual rates seen in the prior expansion. And the inventories-to-sales ratio remains near all-time lows, suggesting an unappreciated underlying strength: The low ratio also implies an incremental end-demand increase would likely spur additional production quickly. Exhibits 2 and 3 show business inventories’ and shipments’ annual growth rates and the business inventories-to-sales ratio since January 1992.

Exhibit 2: Business Inventories and Shipments (year-over-year change)

Sources: US Census Bureau, Thomson Reuters

Exhibit 3: Business Inventories-to-Sales Ratio

Sources: US Census Bureau, Thomson Reuters

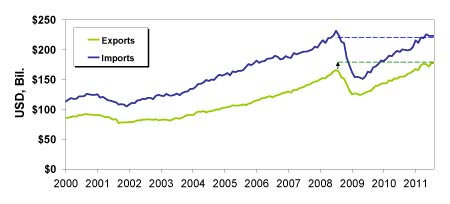

US trade was essentially flat in August, with total trade posting a very modest month-over-month dip. Exports remain near the record high set in July, and imports’ and exports’ annual growth rates remained strong at 11.4% and 14.7% in August, respectively (both categories’ monthly rates were virtually unchanged).

Exhibit 4 shows US imports and exports since 2000. Total trade has grown robustly during the current expansion.

Exhibit 4: US International Trade (Nominal)

Sources: US Bureau of Economic Analysis, Thomson Reuters

Though recession is always possible, these data taken in concert with other recent data from the US and world suggest it’s unlikely in the near term, in our view. Headline economic growth may remain volatile, as it’s been year to date, but a fluctuating growth rate a couple years into an expansion is fairly typical through history.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today