Personal Wealth Management / Economics

US GDP: Statisticians Will Replace Fuzzy Math With Different Fuzzy Math

Whether or not US GDP's Q1 contraction is eventually revised away, nothing here bodes ill for the economy.

The sun rises over the Port of Oakland. Photo by Silentfoto and Getty Images.

So US GDP "officially" contracted in Q1, as the Commerce Department revised their estimate from 0.2% growth to a -0.7% contraction (all figures at seasonally adjusted annual rates). While some say this "raises questions" over America's underlying strength and bemoan the "economy's continuing inability to generate much momentum," others were far more calm. Count us among the optimists: In addition to the widely discussed temporary skew from weather and the West Coast Ports labor dispute, most of the components here just weren't all that bad.

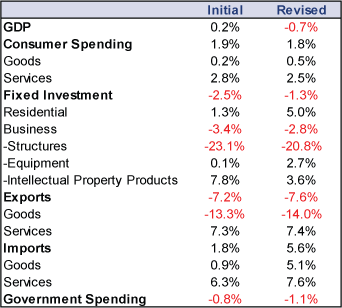

Exhibit 1 shows the breakdown. Consumer spending was revised down a tad, but spending on goods bumped up. Fixed investment was revised higher-including business investment. Imports went way up, from an initial estimate of 1.8% to 5.6%. Imports subtract from GDP, but don't let that fool you: Rising imports mean domestic demand is strong.

Exhibit 1: Q1 GDP Growth, Initial and Revised Estimates

Source: Bureau of Economic Analysis, as of 5/29/2015. All figures are in 2009 USD at seasonally adjusted annual rates.

Trade is also where the longshoremen's labor dispute becomes evident. Trade in services, which are not packed in containers and transported across oceans on ginormous boats, flourished. Trade in goods, which are packed in containers, transported across oceans on ginormous boats and then manually unloaded by human beings with really cool cranes, tumbled. We, and pretty much every economist and logistics industry insider, reckon a labor dispute between ports operators up and down the Pacific coast and those strong, crane-operating people is why that tumble happened. Yes, imported goods rose, but we're inclined to chalk that up as a timing quirk. By the time the dispute ended, a few dozen ships-loaded to the gills with goods from Asia-were idling outside harbors from San Diego to Seattle. In the short window between the dispute's settlement and Q1's end, longshoremen unloaded more ships than they had time to reload. It'll all even out in the end. Just give it time.

Our views on the business investment breakdown aren't much changed from the first estimate, discussed here. Oil companies cut back heavily, driving most of that eye-popping decline in investment in structures. Turns out they cut back a little less than initially surmised, while investment in equipment was a bit better. As for the slowdown in intellectual property products, a lot of that is tied to a drop in arts & entertainment royalties. Hollywood bigwigs, you have our sympathies (we guess).

The other story here, of course, is the Northeast's horrible weather, which anecdotal evidence and regional surveys tell us whacked shopping and output in that region. The BEA's seasonal adjustments are supposed to scrub most of this, but as several economists have noted in recent weeks, Q1 growth rates have been strangely weaker than the rest of the year for the last 30-odd years-and glaringly so since 2010. Last week, the BEA conceded the point, announcing a "multi-pronged action plan"[i] to address this "residual seasonality." This includes adjusting for the fact Federal defense spending is habitually lower in Q1 and Q4, seasonally adjusting some inventory data for the first time ever, and changing the way they scrub certain services surveys. And, for good measure, they'll manually review every last series that goes into GDP for evidence of lingering seasonal skew, and massage it away if necessary.

Now, make of all that what you will. We aren't going to stand up when these new seasonal adjustments hit on July 30 and shout, "Huzzah! 'Tis accurate now!"[ii] Rejiggering seasonal adjustments amounts to exchanging one form of arbitrary data torturing for another, which speaks to how fuzzy GDP is-and why we encourage investors not to rely on it (or any one stat) as their sole barometer of the economy. This is also a big reason we wouldn't get too hung up on fluctuating growth rates, good or bad-just the broad trends, how they square with expectations, and how they stack up with other indicators. If one month or quarter diverges from the trend as Q1 GDP does, just dig deeper to see if it's likelier to be a blip or the start of a new trend.

Whether or not we find out on July 30 that the US grew in Q1 after all, any dip or stall is likely a blip. Consumers are still spending. Outside oil, businesses are still investing. Rising imports tell us domestic demand is strong. Rising service exports say the same about demand abroad. The Conference Board's Leading Economic Index-that uncannily accurate indicator that hasn't missed one single recession since 1959-is high and rising, up in 14 of the last 15 months with April's 0.7% rise.

Stocks are forward-looking. They won't fuss over what happened between two and five months ago, good or bad. They're considering what is likely over the foreseeable future-and that, friends, is more growth.

[i] We like this phrase a little too much. It's jargon with a side of boardroom cheese. Yes, please!

[ii] Ok, we might, but only in jest, and no one will see it outside of our quirky corner of Fisher Investments' office.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today