Personal Wealth Management / Market Analysis

Volatility, Continued

Stocks seesawed wildly Tuesday, finishing the day solidly in the black.

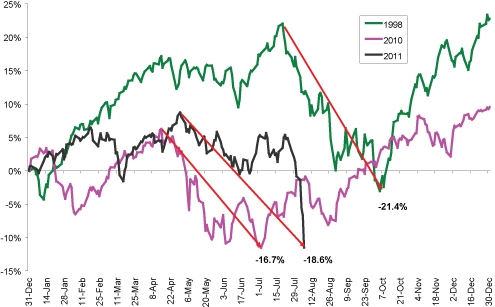

Stocks have been volatile of late. And yes, Tuesday, though up big, was a heck of a volatile day. Investors tend to think of downside volatility as “volatility” and upside volatility as “good.” But it’s all volatility—and it’s quite normal. Not all market negativity presages a recession and/or bear market. Quite often, it’s a standard market correction, and we believe that’s what we’ve got—a short, sharp shock driven by a huge story or stories that dominate headlines. For example, 1998 and 2010 both had similar big corrections, but fine or even fantastic overall returns.

Corrections of 1998, 2010 and 2011 (through 8/8/11)—MSCI World Index-Price Return:

Source: Thomson Reuters.

Now, a sharp correction doesn’t necessarily imply big positive returns in calendar year 2011. But a big correction followed by a strong finish isn’t unprecedented. And 2010 and 1998 had sentiment features similar to today.

Most of what’s driving current volatility seems to be a preoccupation with fears of several flavors, most of which aren’t new or fundamentally big enough to overwhelm extant positives and drag stocks down over the next 12 months. At times like this, as tough as it can be, we advise taking a more measured look at economic conditions. We start with a survey of today’s major headlines.

Downgrade fallout

Single Mother From St. Louis Flying Banner Over Lower Manhattan: ‘Thanks for the Downgrade. You Should All Be Fired.’

As we’ve said here and here, we think ratings agencies aren’t much use, and S&P’s downgrade doesn’t say anything new about the state of the US economy. But the joke isn’t the $2 trillion miscalculation—it’s that they felt the need to try to estimate future US deficits at all. They’d long hinted the downgrade was coming and entirely for political reasons. That they tried to rationalize it quantitatively tells us even they knew their rationale was thin. If the US shouldn’t have top-notch credit because its legislators can’t agree on anything, no democratic country should.

More important than S&P’s opinion are stories like these:

US 2-Year Notes Yield Falls to Record on Fed Move

The US’s first debt auction as an AA+ country was a resounding success: Yields fell (signifying lower perceived risk), and demand was strong.

Asia to Keep Buying US Debt Despite Downgrade

Why? Because the depth and liquidity of US Treasury markets are unmatched—by a wide margin—and despite the downgrade, US Treasurys remain one of the lowest risk vehicles around.

Certain uncertainty

The Uncertainty Shock From the Debt Disaster Will Cause a Double-Dip Recession

We find a few things to quibble about in this news story, including the assumption the VIX is predictive. But what really caught our eye was the talk of “massive economic uncertainty.” We won’t argue at all that things aren’t certain today...but when is the economy ever certain? Every expansion has headwinds and tailwinds, and in our view, this one’s no different. More important than how folks feel, in our view, is how they act—for example, consumer confidence fell in June and July, even as retail salesincreased. Watch what people do, not what they say or feel.

Debt is scary. No, cutting spending. No, a downgrade...

If there’s a theme to the past few weeks, it’s fear. Consider recent headlines: First, the US was well on its way to spending itself into oblivion—debt is scary. Then, politicians and the media warned if we cut too much spending, we’d imperil the recovery and send the country (possibly the world) into a (widely feared but rare in actuality) double-dip recession—cutting spending is scary. Then, even if we avoided demise from fears one and two, we might still be downgraded—so a downgrade is scary.

But those fears are basically mutually exclusive, meaning you can’t fear them all simultaneously. What’s seemingly gripped markets and investors is a fear of fear—worrying you’ll miss the next big, scary news story and be hurt as a result.

As it’s turned out, markets have been quite volatile—not terribly surprising when the media finds bad news in every story, positive or otherwise—but nothing so economically dire as any of the widely touted outcomes has actually come to pass. Regardless, markets and investors will likely continue to fret for now—fodder for stories like these:

3 Questions: Parsing Turbulent Market in Wake of S&P Downgrade

In the run-up to the debt ceiling deal, headlines warned a downgrade would mean higher interest rates. But since S&P’s downgrade, interest rates have fallen, and these news stories tell us too-low rates are equally bad (if not worse) because they indicate low growth expectations. But if rates remain low, businesses and sovereignties can continue borrowing and financing growth easily in various ways—in our view, that’s an incremental positive for the economy and markets.

A plethora of perceived problems

Recently, volatile markets and some economic data have many pundits and politicians opining the US and world have big economic problems. But do they really, or is this a selective view of economic conditions? Some data to consider:

US consumers (who many say won’t or can’t spend) boosted online retail spending14% y/y in Q2, accounting for roughly 10% of US discretionary spending. This, on top of US July same-store sales that rose 5% y/y. Then consider US Q2 2011 GDP growth, which so many sources bemoaned as slowing, actually accelerated from Q1 2011 (to +1.3% from +0.4%). Housing has even shown signs of life lately.

Of 436 S&P 500 companies reporting Q2 earnings as of August 5, 72% beat estimates, 9% met and 19% missed. And excluding a well-publicized bank with one-time litigation issues, the earnings growth rate was 17.7%. Moreover, this wasn’t all generated through cost cutting. Nine of ten sectors are on pace to report growing revenues in Q2—increasing revenues are a key sign of global health—with expected revenue growth of 12% y/y for the quarter.[i] The lone exception: Financials. It’s awfully difficult to square double-digit sales gains with what many assume are economic dire straits. All recent data, all showing growth.

Corrections by their very nature are unpredictable. We can’t say when this one will end. We can say that more volatility is likely in the fore and it will be trying. But in our view, this continues to be a classic correction. Patience and steely nerves are likely rewarded.

[i]Source: Thomson Reuters, “This Week in Earnings,” August 5, 2011.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today