Personal Wealth Management / Economics

Wednesday Wrap-Up: Services Data, Earnings and Biden’s ‘Big’ Decision

A midweek financial news potpourri.

What do corporate earnings, services PMIs and Fed head Jerome Powell have in common? Nothing! Except that all hit headlines on Wednesday, inspiring us to bring you a roundup of financial news you can use. Off we go!

Services PMIs Are News, Not New

If you like economic data, then the third business day of the month is always your friend, because it brings us services purchasing managers’ indexes, or PMIs. These monthly surveys show the percentage of businesses reporting increased activity across a range of categories and whether getting goods to market is easier or harder. Readings over 50 indicate more firms reported growth than contraction, and the biggest PMIs all topped 50 by a mile in July—like their manufacturing counterparts, they clustered around 60. The US ISM Services PMI (formerly known as the Non-Manufacturing Index) rose to an all-time high of 64.1.[i] New orders were robust, and overall, services industries seem to be firing on all cylinders. But demand remains far above supply, creating shortages and bottlenecks for retailers, echoing Monday’s manufacturing report.

Interesting as July’s PMIs might be, they don’t tell investors anything new. We already knew services were in the catbird seat as the reopening process continued, especially in Europe. Personal services and restaurants were among the last businesses to reopen, and establishments that depend on foot traffic from local office workers are finally getting a lift from white collar workers’ return. All this was telegraphed far in advance and is well-known to stocks. Momentum shifting from the “stuff” economy to the “people” economy also got a big preview in the US’s June consumer spending report on Friday, which showed spending on services leapfrogging spending on goods. That, by the way, echoed the May report, where goods spending dropped while services rose. Oh, and those supply hang-ups? Well known for months. We say that not to dismiss them, but to remind you how markets work: They look forward, pricing in expected events over the next 3 – 30 months. Data—even timely data like PMIs—look backward, confirming what markets already priced in. The new orders component has some forward-looking powers, as today’s orders are tomorrow’s production, but that is a leading economic indicator, not a market forecasting tool.

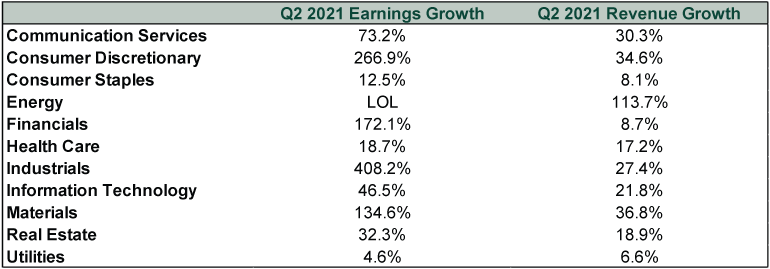

Q2 Earnings: Fun With Math and Big Numbers

With over 75% of S&P 500 companies having reported Q2 earnings as we write, it is safe to say earnings growth is off the charts. Figuratively, in total earnings’ case, as they are up 87.0% y/y, which is possible to chart. Literally, in Energy earnings’ case, as the year-over-year comparison is a negative number, owing to Energy firms’ collective $10.6 billion loss in Q2 2020.[ii] The $15.7 billion in net income reported so far for Q2 2021 is obviously far higher, but a percentage growth rate is incalculable. Witness: 100 × [(15.7 ÷ -10.6) – 1] = -148.1. But earnings did not drop another -148.1%. So FactSet rightly reports Q2 earnings growth as “ – ,” which we converted to LOL in Exhibit 1 because it is more fun. But if you still crave some kind of a number, the Energy Equipment & Services industry grew 1,381.1% y/y, which may actually be more mind-boggling than the dash or our LOL.[iii]

Numbers in other sectors were more rational[iv] but still far from normal, as Exhibit 1 shows. We overall find the revenue side of the table more useful this time around, as it has fewer distortions.

Exhibit 1: Q2 2021 Was Better Than Q2 2020

Source: FactSet, as of 8/4/2021. Blended S&P 500 earnings and revenue growth, year-over-year, Q2 2021.

To state the obvious, publicly traded companies are overall a heck of a lot better off now than a year ago. That makes sense, considering lockdowns reigned in Q2 2020 and they do not reign now. Economies are open, albeit unevenly, with fits and starts. Some coverage has noted stocks’ overall lack of enthusiasm over these results, arguing it implies the bull market is petering out. But we think that misunderstands how markets work. These earnings are a product of today’s reopenings and last year’s dreadful base effect. Stocks began pre-pricing the reopenings that would generate these profits in late March 2020—before governments even lifted the lockdowns. They were looking 3 – 30 months out then and are now doing the same. These earnings, though sparkling, are backward-looking. Stocks aren’t tired, just efficient.

Don’t Overrate Powell’s Power or Fear Brainard’s Brain

To read financial news coverage, President Joe Biden confronts a monumental decision in the near future: whether to reappoint Jerome Powell as Fed head. His term expires in February 2022, and we are reaching the time of year when presidents usually decide what to do about Fed head nominations. Barack Obama tapped Janet Yellen in October 2013, and Donald Trump nominated Powell in November 2017, so as autumn nears, the questions are mounting.

In recent history, presidents have mostly opted to keep their predecessor’s Fed head in place so long as he or she wasn’t retiring. Ronald Reagan initially kept Paul Volcker, a Jimmy Carter appointment, before charting a new course with Alan Greenspan in 1987. George Bush, Bill Clinton and George W. Bush reappointed him until he retired in 2006, when the latter Bush picked Ben Bernanke to replace him. Obama kept him around until he decided to step down. Trump’s decision to make Yellen a one-termer is the outlier, hence, pundits’ baseline expectation is for Powell to stay, which they say must be markets’ presumption, too.

In recent days, however, a new thread has emerged: Several pundits have warned Biden could dismiss Powell, a Republican, and anoint Lael Brainard, a Fed Governor first appointed by Obama and who served in the Obama and Clinton administrations. She is widely seen as more in line with Biden’s sociological viewpoints, leading some pundits to argue that if she indeed takes the reins, the Fed will shift from fighting inflation to attempting to engineer economic equality, sacrificing price stability as collateral damage. Thus, they argue, her appointment would be negative for markets.

We think that is quite hasty. For one, it presumes to know exactly how Brainard would think and act once in the top job. History roundly shows otherwise, with pretty much all Fed heads in history defying expectations and their own earlier viewpoints. It also presumes she will automatically let politics bleed into monetary policy, which strikes us as unfair and ignores Yellen’s entire record. (Not to mention Powell’s, Bernanke’s, Greenspan’s, and and and.) Most importantly, the Fed is a committee, and decisions require consensus. Oh, and markets don’t pay attention to Fed personalities any more than they care about political personalities. We have a long, long, long history of markets not caring about who is running the Fed and, instead, judging decisions as they are made. We therefore humbly suggest investors do the same.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Kevin Warsh and the Magical Delete Button2026-06-17

-

Market Analysis The Politics and Practicalities of the Social Security Trust Fund2026-06-16

-

Market Analysis Gold Fails the Safe Haven Test Again2026-06-16

-

Expert Commentary Ken Fisher on Crypto, Inflation, AI Bubble and Annuities

2026-06-16

2026-06-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today