Personal Wealth Management / Market Analysis

What the Options Whale Watchers Miss

As is usual when stocks fall fast, people are grasping for technical causes and culprits.

Editors’ Note: MarketMinder doesn’t make individual security recommendations. The below simply represents a broader theme we wish to highlight.

Market volatility is as old as markets themselves. It has always sprung randomly, for any or no apparent reason, catching folks off guard and testing disciplined investors’ patience. Enduring these normal wobbles is, unfortunately, the price that comes with stocks’ long-term returns. Market history shows reacting to volatility is usually a recipe for error. We think that is true of this latest volatility as well. Tuning down the noise associated with quick drops is usually key to maintaining discipline. But that isn’t the natural response, especially among financial commentators. Instead, the search for a cause—and, very often, someone to blame—seems to hog most folks’ energy. We are seeing a lot of that now, with most coverage landing on sensational technical reasons—rather reminiscent of 2010’s Flash Crash. Usually, this search for a story is a sign of a sentiment-driven correction, not a bear market, and we don’t think this time is different.

When Tech first sold off last Thursday, the consensus explanation was old-fashioned “profit taking” or that stocks were “exhausted” after a big August climb. That is a technical term for “we can’t see any rational reasons or underlying problems, and these companies are strong, so people are probably just locking in some gains.” But this isn’t much of a story, and to many, no story isn’t satisfying. So the hunt continued. It didn’t take long for many pundits to land on a whale: SoftBank, the Japanese Tech conglomerate turned de-facto investment fund, which a Financial Times report revealed had bought several billion dollars’ worth of call options on individual Tech stocks. A Wall Street Journal analysis gave some more specific numbers, saying: “The Japanese Technology conglomerate has spent $4 billion on options tied to $50 billion of individual technology stocks. The company also disclosed last month that, as of June, it owned nearly $4 billion worth of tech stocks like Apple and Tesla. It is unclear how much of those positions SoftBank is still holding.”[i] Combine that with reports of retail investors’ indulging in a call options frenzy in recent weeks, and now we have a volatility story: A whale and a school of little fish joined together in a unidirectional bet on Tech stocks, creating a rally built on sand and euphoria and setting things up for a big drop when the cheer wore off.

For the uninitiated, when you purchase a call option, you get the right to buy the underlying stock at a pre-set price (the “strike price”) in the future. The goal is for the company’s share price to rise above the option’s strike price, so that when you exercise the option, you can quickly flip the stock for a tidy profit. Those selling call options are effectively short on that same position, so to hedge, many counterparties will buy the underlying shares. That forced buying appears to be part of the SoftBank story, according to a New York Times report.[ii] So, the popular narrative goes, markets got stuck in a weird feedback loop where SoftBank and normal people were speculating on rising prices, dealers were pushing prices higher to cover their exposure, and rising prices drove more speculation—all combining to build a house of cards.

We won’t argue there was zero froth in Tech, but hot sentiment alone doth not a bubble make. As many pointed out last week, company fundamentals today are light years from where they were 20 years ago, as the dot-com bubble was bursting. Then, the market was full of shaky new companies with no sound business plan, high cash burn rates and deep losses. Rather than judging their balance sheets fairly, investors argued “clicks are the new profits” and bought, bought, bought. Today, the companies in question have some of the healthiest balance sheets in the S&P 500, and people like them because of their strong earnings and resilience during the pandemic. To the extent people got a bit out over their skis over some actual fundamental positives, that is a recipe for a pullback to shake out the weak, not a catastrophic perma-crash. It is also the norm, as there are frequently small areas of the market or individual firms in which expectations get carried away.

But to say SoftBank is the driving force behind Tech’s climb this summer is quite overstated, in our view. Going by the Journal’s numbers, its counterparties would have bought $50 billion worth of stocks, give or take. But total market cap of the FAANG stocks (Facebook, Apple, Amazon, Netflix and Alphabet/Google) plus Tesla hit as high as $6.53 trillion on September 1, up from $5.44 trillion at July’s close.[iii] You don’t get that increase without much broader demand. So even if Softbank decides to unwind its positions—a big fear in today’s headlines—there is a buyer for every seller. (Besides, it isn’t clear the extent to which SoftBank still has exposure.) Many buyers would probably be happy to snap up these companies at a temporary discount.

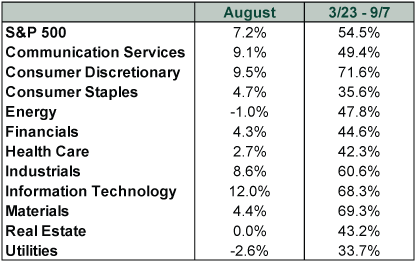

Moreover, the focus on Tech call options overlooks how broad this rally actually is. Headlines routinely portray it as Tech-only, with all others left in the dust. While Tech and the Tech-like FAANGs have led overall, it isn’t as though gains are limited to them. Exhibit 1 shows the 11 S&P 500 sectors’ returns in August and since March 23’s low. At a more granular level, the FAANGs and Tesla get all the headlines, but 72.3% of stocks in the S&P 500 rose in August.[iv] Since March 23, 98.6% of constituents are up.[v] The S&P 500 has added about $10 trillion in total market cap during that span.[vi] In our view, the much more logical explanation is that the entire market is looking ahead to the day when COVID is old news and society has learned how to live with the virus while maintaining full levels of economic activity.

Exhibit 1: S&P 500 and Sector Returns

Source: FactSet, as of 9/8/2020. S&P 500 and S&P 500 sector total returns, 7/31/2020 – 8/31/2020 and 3/23/2020 – 9/4/2020.

In a weird way, we think the search for a story and scrutiny on options traders are positive signs. This year’s COVID lockdown panic aside, bear markets usually begin gradually, and most observers ignore or explain away the gentle declines. The main story is usually reasons to ignore stocks’ slide and buy the dips, not reasons stocks were due for a fall and more pain awaits. In a correction, having a big story is one thing that helps investors get over the volatility. They see a scary thing in waiting (allegedly overvalued Tech stocks), they see the scary thing playing out (speculators’ chickens coming home to roost as their bets go south), they see the market registering it, and then its power wanes. It happened, had its effect, the world didn’t end, and investors emerge with one less thing to fear. This is one of the main ways stocks climb the proverbial wall of worry during bull markets.

In the end, we imagine the SoftBank story will go down in history with the Flash Crash as a market curiosity that came and went. Perhaps it will lead to more chatter over non-financial companies’ investments and new disclosure requirements, much as 2012’s London Whale incident at JPMorgan Chase did. But these things tend to play out slowly and inside baseball generally isn’t a market driver.

[i] “SoftBank’s $4 Billion Tech Option Gambit Feels Like Déjà Vu,” Jacky Wong, The Wall Street Journal, 9/8/2020.

[ii] “We Have Some Questions About SoftBank,” Andrew Ross Sorkin, Lauren Hirsch, Michael J. de la Merced and Jason Karaian, The New York Times, 9/8/2020.

[iii] Source: FactSet, as of 9/8/2020.

[iv] Source: FactSet, as of 9/8/2020. Percentage of S&P 500 constituents positive in August 2020.

[v] Ibid. Percentage of S&P 500 constituents positive for the period 3/23/2020 – 9/4/2020.

[vi] Ibid. S&P 500 total market cap change, 3/23/2020 – 9/4/2020.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 9 - March 132026-03-16

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today