Personal Wealth Management / Market Analysis

When Sentiment Prices in Reality: Japan and UK Edition

Sentiment seems to be sensibly seeing through the noise in Japan and the UK, illustrating how markets work.

Pop quiz: When is bad news not really bad news for stocks? Generally speaking, when it is long-running, well-known bad news that investors and the world at large seem to have a rational grasp of. We think Japan and the UK provide real-time examples presently.

To understand how these nations’ economic data interact with markets, we think there are two bedrock investing principles to consider. First: Stocks look forward, pricing in all widely known information about factors affecting companies’ earnings outlooks, be they economic or political. In our view, stocks look around 3 to 30 months out, focusing mostly on the next 12 to 18. As the market digests probable outcomes, it sets baseline expectations within this horizon—but they aren’t infallible. Legendary investor Benjamin Graham once noted that stocks are like a “voting machine” in the short term, which can be driven by sentiment, but in the long run they act more as “weighing machines,” assessing fundamentals.

Second: Stocks move most on the gap between reality and expectations. Positive economic data alone aren’t enough to be bullish, and vice versa. If expectations priced into stocks match reality on a forward-looking basis, unsurprising results are unlikely to sway markets materially. What matters for investors isn’t the reality—good or bad—per se, but whether broad sentiment appreciates it properly, overestimating (bearish) or underestimating (bullish) its prospects. In other words, the surprise (or lack thereof) factor. This is why stocks can climb the proverbial “wall of worry” and tend to “die on euphoria.”

Rational Skepticism in Japan

The financial press is treating recent positive Japanese economic data with appropriate skepticism, in our view. April’s core machinery orders, released last week, not only rose for the third straight month, but accelerated in each. Often, in our experience, headlines would be all over a few months’ upticks, claiming Japan is getting over its soft patch. (Or, if there is a weak reading, extrapolating economic doom.) Since core machinery orders supposedly represent future investment, some might say its recent strength signals Japan’s improving prospects. But in this case, the negative take appeared to match reality: “Surprise Gain in Machinery Orders Masks Cooling Outlook,” which made the argument export-reliant Japan probably isn’t doing so great, with external orders (not included in the “core” figure) falling -24.7% m/m in April. This is just one recent example, but we think it matches the tenor of Japanese economic coverage in recent months.

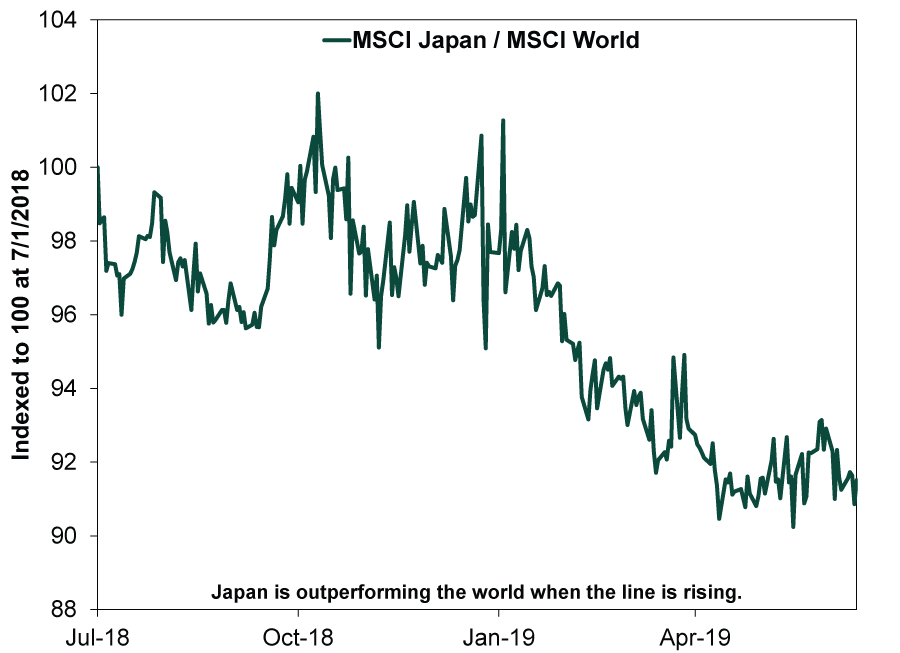

Sentiment in Japan seems to be seeing reality—and the outlook—for what it is. We think this could be one reason Japanese stocks have performed more or less in line with the world since April after underperforming earlier this year amid uncertainty over the pending sales tax hike, a potential snap election and mixed economic data. (Exhibit 1) When negative news is expected, weak data don’t carry much market-moving surprise power.

Exhibit 1: Japanese Stocks’ Relative Returns

Source: FactSet, as of 6/17/2019. MSCI Japan Index divided by the MSCI World Index. All returns in USD with net dividends, 7/1/2018 – 6/14/2019.

The UK’s Sensible Sentiment

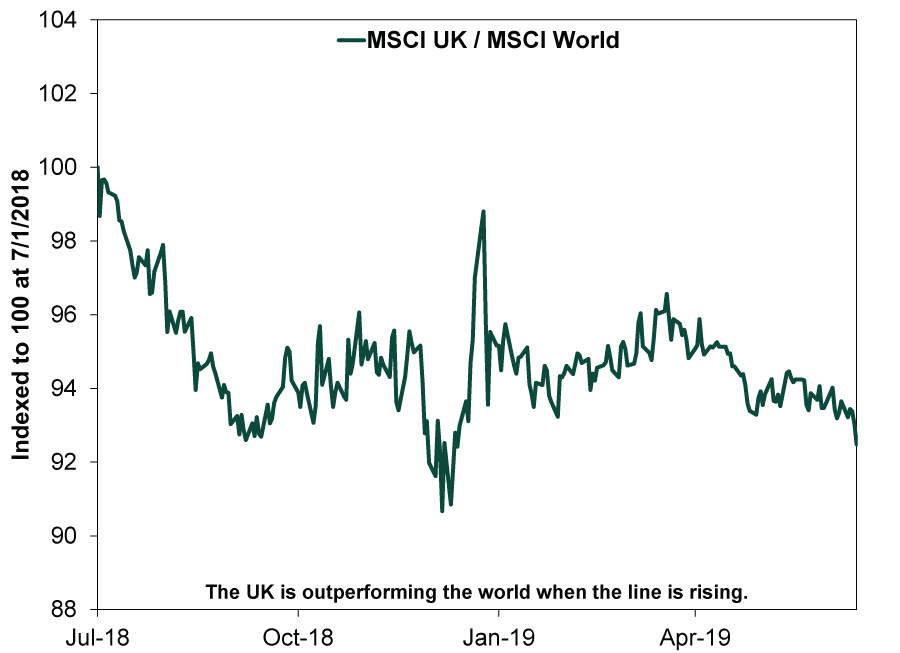

In Britain, we think a similar sentiment-matching-reality dynamic prevails. Noisy news continues surrounding Brexit, from Prime Minister Theresa May’s resignation and the scrum vying to succeed her to economic disruptions from the Brexit delay. To say nothing of Brexit’s ultimate form and timing remaining a question mark! Yet despite this and wobbling economic data, UK stocks are basically in line with world returns since September 2018. (Exhibit 2) This follows a patch of underperformance from Q2 and Q3 2018—even as GDP accelerated—showing how markets apparently pre-priced Brexit uncertainty dampening 2019 growth. The actual slump wasn’t a surprise.

Unlike Japan, we find Britain’s underlying economic growth drivers fundamentally fine. Despite the headline gloom, it looks like the UK market is sensibly keeping its head. In the UK, weaker economic data this year are a foregone conclusion to most, as the inventory overhang following Q1’s now-unnecessary pre-Brexit stockpiling is widely known.

Exhibit 2: UK Stocks’ Relative Returns

Source: FactSet, as of 6/17/2019. MSCI UK Index divided by the MSCI World Index. All returns in USD with net dividends, 7/1/2018 – 6/14/2019.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today