Personal Wealth Management / Market Analysis

On Japan’s January Hiccup

While the effects of China’s slowdown are probably short-lived, their fading won’t resolve Japan’s underlying problems.

After Japanese Q4 GDP rebounded from Q3’s one-off, natural disaster-driven contraction, January data suggest the economy got off to a subpar start in 2019. The primary culprit? Softer Chinese demand. While this headwind should pass, in our view, other economic woes—especially weak domestic demand—likely linger, hindering Japanese growth and hampering domestically focused Japanese firms.

Up first: some not-so-pretty numbers. Japanese firms’ machinery orders—which many consider a harbinger of broader business investment—fell -7.9% m/m in January.[i] Core orders—which exclude the volatile categories of ships and electric utility orders—also contracted (-5.4% m/m).[ii] January was the third straight contractionary month for both. Elsewhere, in a sign of tepid external demand, core machinery orders from overseas fell -18.1% m/m—the same pace as December.[iii] Exports also struggled, falling -8.4% y/y in January after December’s -3.9% drop.[iv] Exports to China fell more, plunging -17.1%.[v] While February exports held up better (as we will discuss), they still fell and missed estimates.

In sum—a poor showing! The usual suspect is Lunar New Year’s shifting timing, which typically distorts first-quarter economic data across Asia. But the common perception goes beyond this, arguing a US/China trade war is sapping Chinese demand and crimping global growth. As its key export destinations flag, the logic goes, Japan suffers. While we think trade war fears are overblown, this explanation has some merit. Tariffs probably partially explain recent weakness, especially if fear of getting caught in the crossfire is leading Japanese businesses to delay spending.

But we see another, more important cause few discuss: China’s crackdown on shadow banking—lending outside the official financial system. Since that is where China’s vast private sector formerly turned for credit, the move choked financing to large swaths of the economy. The resulting decline in Chinese demand appears to have crimped growth as far away as Europe. However, we believe the pain is likely short-lived. In an effort to ease private companies’ transition to traditional banks, Chinese policymakers have been implementing substantial fiscal and monetary stimulus. The monetary measures—including bank reserve requirement cuts and incentives to lend to small and mid-sized private firms—probably make a larger impact, but not immediately. Monetary policy typically takes effect at a lag, as more available financing gradually feeds into borrowing, business investment, hiring and the like. As it does, we expect rebounding Chinese demand to buoy exports from major trading partners like Japan.

It may already be: Although Japanese exports dipped again in February (-1.2% y/y), shipments to China rose 5.5%, thanks largely to a 16.3% surge in machinery orders.[vi] We likely need more data to confirm a bounce, though, as the Lunar New Year could skew the data. Fading trade war fears could also help, particularly if ongoing US/China trade talks reach a resolution. But even if these headwinds dissipate as we expect, Japan’s deeper problems probably remain.

Chief among them is a reliance on external demand to fuel growth. In 2017, exports were 17.4% of Japanese GDP.[vii] While not huge compared to its developed-world brethren—exports were 48.5% of 2017 eurozone GDP, for example—a years-long malaise in domestic demand has left exports as Japan’s primary growth engine.[viii] When they pull back, the economy typically suffers.

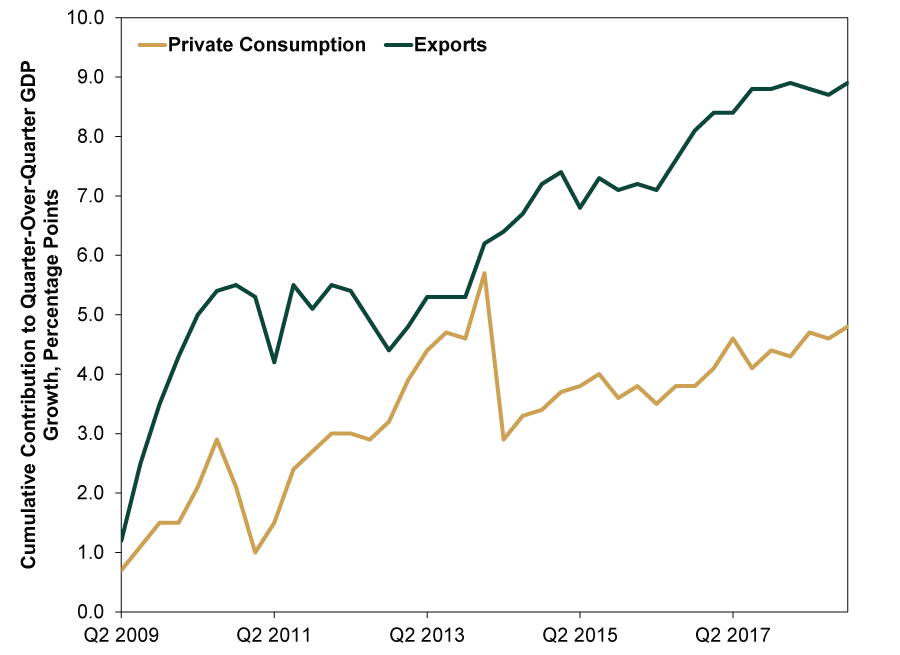

Exhibit 1 shows this: Export growth’s contributions to GDP have far exceeded private consumption’s during this global expansion.

Exhibit 1: Japanese Exports Versus Private Consumption

Source: FactSet, as of 3/14/2019. Cumulative contribution to Japanese quarter-over-quarter GDP growth of private consumption and exports, Q2 2009 – Q4 2018.

The divergence is particularly stark since Q2 2014’s consumption tax hike from 5% to 8%. Another hike—this time to 10%—is scheduled for October.[ix] While it likely will pull some buying forward—as it seemed to last time—a broad increase in prices probably isn’t great for private spending. Domestic demand didn’t get off to a roaring start in 2019, either. Though no single month’s numbers reveal a ton, retail sales and industrial production contracted in January (-1.8% and -3.4% m/m, respectively).[x]

Beyond monthly data, Japan’s economic backdrop is mixed. An inflexible labor market and the BoJ’s counterproductive quantitative easing (QE) policies are notable headwinds. As we have written, while QE aims to boost bank lending, it does the opposite by cutting into banks’ profits on future loans. Hence QE’s sterling record of depressing lending and growth. The BoJ’s QE program is the world’s largest relative to GDP and the only one still in effect. Given the bank’s (misguided, in our view) focus on using QE to weaken the yen, it probably isn’t going away anytime soon. On the positive side, a mammoth Japan/EU trade deal went into effect last month, following close on the heels of a resurrected (and sans-US) Trans-Pacific Partnership. The US and Japan are also about to open up trade talks. Fewer trade barriers probably improve Japan’s outlook. But the benefits tend to be incremental and longer term, with little immediate effect on the economy and markets.

In our view, Japan’s private consumption travails are a negative but not a death-knell. Strengthening demand for Japanese goods (from China and elsewhere) probably sustains Japanese growth as stimulus slowly kicks in. Hence, we don’t think global investors should ignore Japan. Caution and selectivity, though, are key. In our view, big Japanese exporters, not domestically focused firms, seem best poised to profit from recovering external demand.

[i] Source: Japan Cabinet Office, as of 3/13/2019.

[ii] Ibid.

[iii] Ibid.

[iv] Source: FactSet, as of 3/13/2019.

[v] Ibid.

[vi] Source: Japan Customs, as of 3/18/2019.

[vii] Source: FactSet, as of 3/18/2019.

[viii] Ibid.

[ix] Unless, that is, the government opts to delay it for the third time.

[x] Source: The Ministry of Economy, Trade and Industry, as of 3/18/2019.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis CPI Sheds Light on Britain’s Price ‘Cap’ Conundrum2026-05-20

-

Market Analysis The Investment Implications of Record-Low Consumer Sentiment2026-05-19

-

Market Analysis More Positive Surprise in Japan’s Q1 GDP2026-05-19

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 11 - May 152026-05-18

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today