Personal Wealth Management / Market Analysis

Why the Rising Dollar Doesn’t Doom Emerging Markets

Recent isolated currency wobbles aren’t a sign of spreading contagion.

To hear headlines tell it, the dollar and Emerging Markets (EMs) are adversaries locked in a perpetual battle—one the dollar is presently winning. The standard narrative goes like this: After yield-hungry investors piled into EMs, rising US interest rates are contributing to dollar strength, knocking their currencies and threatening their companies’ finances. The Argentine peso and Turkish lira have been especially hard-hit, prompting steep rate hikes to stanch the bleeding. The Indonesian central bank followed suit today, “pre-emptively” lifting rates in an unscheduled meeting. As now-frightened investors flee, media warn the risk of a 1998-style currency contagion looms, possibly threatening growth in EMs and beyond. In our view, this narrative is lacking. Both history and fundamentals show EM economies can fare just fine with a rising dollar.

Strong dollar fears aren’t new—they first flared during this bull market in 2013’s “taper tantrum,” when folks believed winding down quantitative easing (QE) would send the dollar skyward and cause foreign investors to pull out of EM in droves yanking the rug out from under companies who borrowed heavily in dollars in prior years. This turned out to be a false alarm: The dollar didn’t budge much, and the Fed tapered—and eventually ended—QE without incident. But the fear returned in early 2015. This time the dollar did strengthen—by the year’s end, it had reached its highest level against the Fed’s broad trade-weighted currency basket since 2003. Yet EMs didn’t endure a wave of defaults on dollar-denominated debt. The MSCI EM Index did struggle in 2015, falling -14.9% that year in USD, but it began recovering well before the dollar peaked.[i] Overall, since 12/31/2014, the index is up 28.2%.[ii]

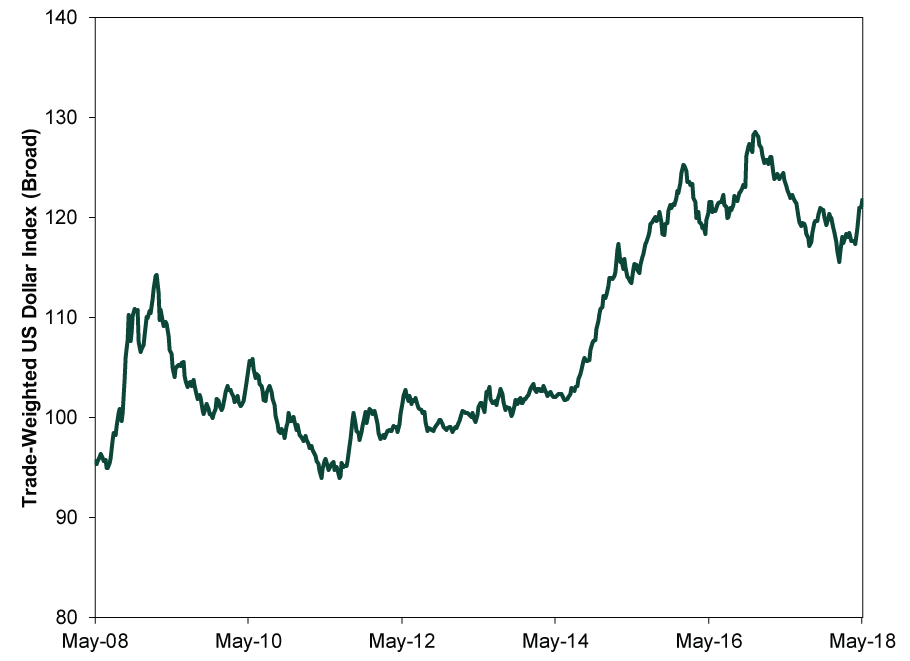

Scaling the dollar’s recent rise also undercuts current worries. Since 2018’s start, it has appreciated just 2.5% and remains comfortably below its prior high in 2016. (Exhibit 1) If Emerging Markets firms didn’t collapse under the weight of dollar-denominated debt payments then, why should there be a crisis now?

Exhibit 1: The Dollar’s Mini-Rally in Context

Source: Federal Reserve Bank of St. Louis, as of 5/30/2018. Trade-Weighted US Dollar Index, 1/4/2008 – 5/30/2018.

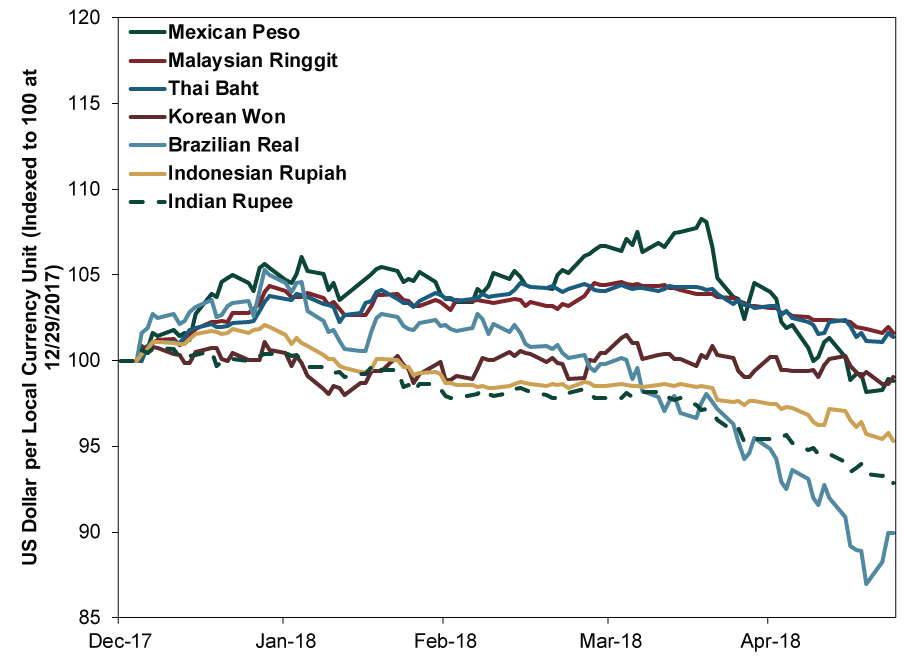

EM currencies don’t appear to be taking it on the chin, either. Most currency weakness is concentrated in Argentina and Turkey, which are special cases—see our Research Analysts’ latest commentary for more. Otherwise, as Exhibit 2 shows, with the possible exception of the Brazilian real, most major, market-set EM currency exchange rates haven’t much budged against the dollar.

Exhibit 2: Select Emerging Market Currencies Not Doing a Whole Lot

Source: FactSet, as of 5/24/2018. USD per local currency unit, 12/29/2017 – 5/23/2018. Currency values indexed to 100 at 12/29/2017. When the lines are falling, the currencies are weakening.

Also worth noting: Since the Argentine peso plummeted, it is part of the “EMs are in distress” conversation. But per MSCI, it is a Frontier Market. Now, other organizations like the OECD classify them differently. But the disagreement—and the fact Argentina is rated as even less developed—speaks to the fact it has structural issues that differentiate it from the other EMs.

When EM fears surface, comparisons to the late 90s’ Asian currency crisis frequently follow, with some speculating spooked investors will abandon EMs en masse. But this misunderstands that crisis’s true causes. Wary of slowing growth, high levels of dollar-denominated debt and unsustainable currency pegs, investors turned on Korea, Malaysia, Thailand and Indonesia in 1997 – 1998, sparking a regional recession. But investors didn’t act arbitrarily or indiscriminately. Money fled these countries because they had similar—and substantial—financial problems, leading investors to conclude they would be unable to service dollar-denominated debt once they broke their currency pegs, which are inherently unstable. Not merely because issues in one sparked a panicked flight from all. Today, only Qatar, Pakistan and the United Arab Emirates have official dollar pegs, while China has a de-facto peg. The other 20 EMs float freely, albeit with some official intervention now and then. Absent pegs, drastic overnight devaluations are highly unlikely.

Another difference: EM governments now have plenty of firepower to intervene if they deem it necessary. They held $6.3 trillion in foreign exchange reserves in 2017 compared to just $430 billion in 1996—a nearly fifteen-fold increase that leaves them far better equipped to stabilize their currencies if needed.[iii] Hence, forecasting an investor stampede seems premature today, especially given the bulk of EMs’ finances are a world away from Turkey’s and Argentina’s.

To be sure, if EM firms loaded up on dollar-denominated debt and the dollar’s value shot up, problems could sprout. Argentina’s present troubles, for example, stem in part from a recent dollar-denominated debt surge. But overall and on average, EM firms haven’t gone hog-wild for dollar-denominated debt. In 2017, this comprised a smaller percentage of most EM countries’ GDP than it did during the late-90s crisis.[iv]

We aren’t predicting the dollar’s moves from here—or any other currency’s. But currencies are only one driver of EMs’ attractiveness to foreign investors. Major EMs today are growing nicely, with more modern and freer capital markets than they had two decades ago. Currency swings still garner headlines, but they aren’t a major economic driver, good or bad. In our view, there is plenty of reason for foreign capital to stay in EMs regardless of currency wobbles.

[i] Source: FactSet, as of 5/29/2018. MSCI Emerging Markets Index return with net dividends, 12/31/2014 – 12/31/2015.

[ii] Ibid. MSCI Emerging Markets Index return with net dividends, 12/31/2014 – 5/28/2018.

[iii] Source: IMF, as of 5/29/2018.

[iv] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today