Personal Wealth Management / Market Analysis

Will Coal Make a Comeback?

A newly proposed rule has some optimistic the coal industry is poised for a rebound, but power generation economics suggest otherwise.

While stumping for West Virginian midterm candidates last week, President Trump invoked one of his signature campaign pledges: ending the so-called “War on Coal.” At a rally, he announced the Affordable Clean Energy (ACE) rule, which would replace President Obama’s 2015 Clean Power Plan (if it took effect). Predictably, media reactions were split. Some focused on the shift’s potential environmental impact, hyperbolically claiming more coal would “kill” Americans, citing long-term forecasts of health issues tied to pollution. Others were more sanguine, theorizing it would throw beleaguered coal stocks a lifeline—something investors have long believed easing environmental regulations would do. We would take both claims with a grain of salt or two. Coal’s declining share of US energy production—the source of coal stocks’ problems—has more to do with cheap natural gas than regulation. Tweaking rules shouldn’t markedly improve their outlook.

The “War on Coal” is a term some used to describe the Obama administration’s approach toward coal-fired power plants. They pushed renewables like wind and solar while ratcheting up emissions standards, which many presumed was a shot at coal. In 2014, President Obama directed the Environmental Protection Agency (EPA) to draft new rules curbing power plants’ carbon emissions. The resulting Clean Power Plan (CPP) targeted a 32% emissions reduction from 2005 levels by 2030. This plan dictated a national standard for emissions, with little leeway at the state level. Some argue CPP accelerated coal’s demise, putting miners out of work and hurting the local economy in coal states—and bringing extra pain to coal stocks, which were already in a world of hurt. US coal stocks fell -97% from March 2011 to January 2016 (though broad-based Energy weakness likely played a larger role than regulation).[i] ACE seeks to shore up the industry by promoting so-called “clean coal,” which involves greater use of technology that aims to reduce emissions from coal plants. The plan scraps national targets and grants states more flexibility to create electricity generation plans, which is why some believe this will boost pollution and the coal industry.

Sounds like a boon for coal! But there is one teensy problem: CPP never actually took effect, making it difficult for us to see how a replacement rule changes much in practice. Twenty-seven states challenged it in court, arguing the EPA was overstepping its legal authority. In February 2016, the Supreme Court blocked implementation. In March 2017, President Trump issued an Executive Order calling for CPP’s review, which led to ACE. Further, coal’s market share has been declining since 2006, well before anyone knew Obama would become president and push tighter regulation in his second term.

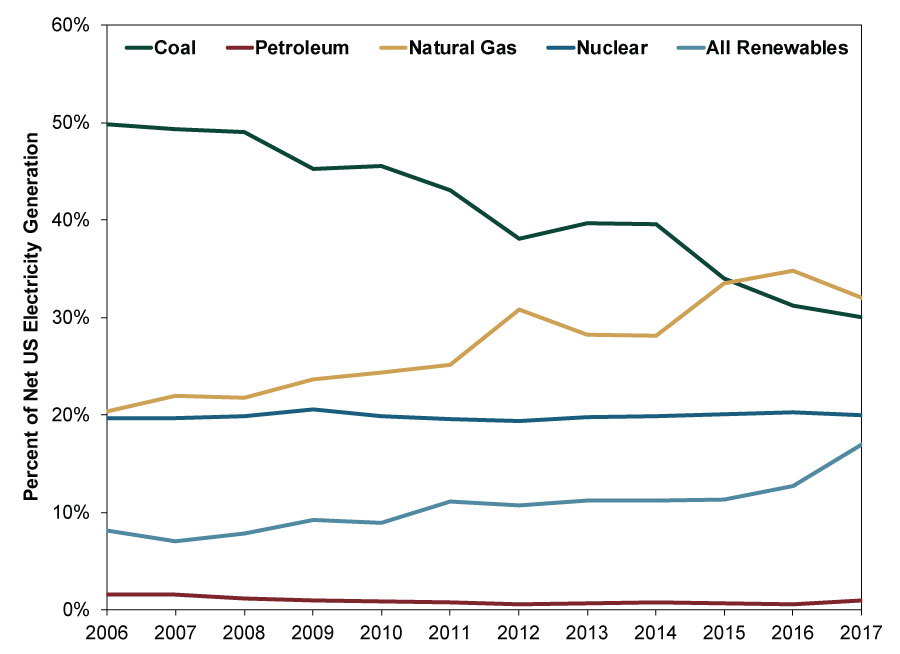

Exhibit 1: Net Electricity Generation by Fuel Source

The eagle-eyed among you may notice one source now eclipses coal’s share of production: natural gas. The shale gas revolution unlocked a treasure trove of US natural gas, driving costs down and incentivizing utilities to shift towards gas-fired plants. For years, coal had a significant cost advantage, but natural gas prices have become competitive with coal, at points nearing parity. And that is just the national average for the fuel. Regional differences, clean coal technology and more could easily tip the balance in natural gas’s favor when all costs are considered.

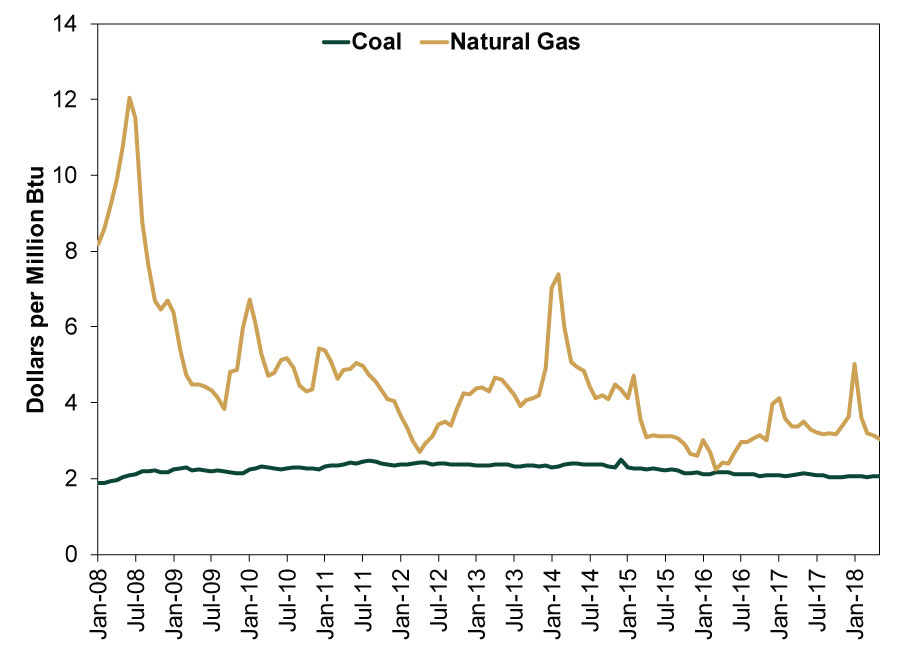

Exhibit 2: Gas Is Now a Competitive Fuel Source

Source: Energy Information Administration, as of 8/28/2018. Average Cost of Electricity Generation by Fuel Source, January 2008 – May 2018.

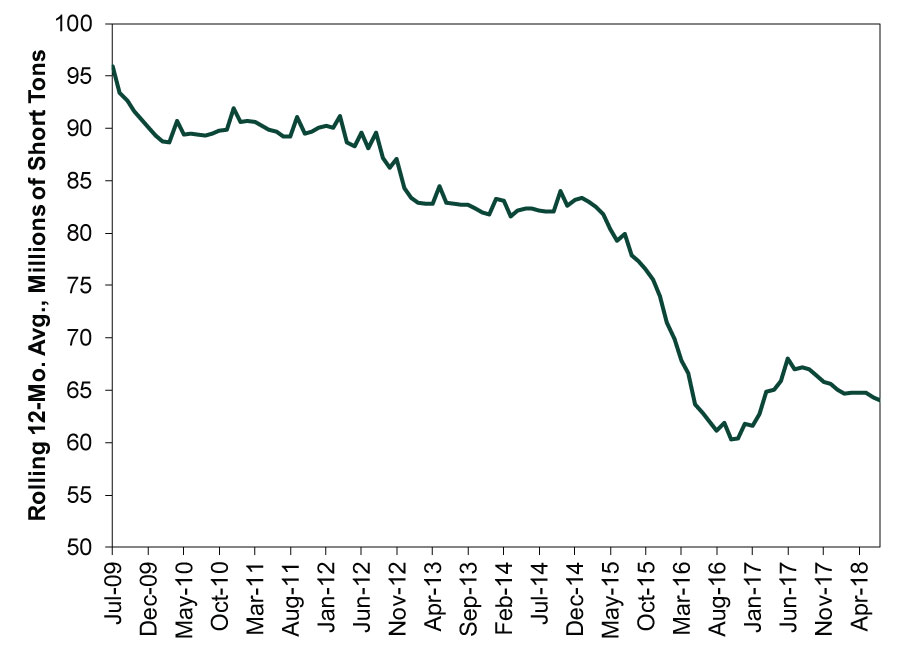

As a result, EIA data reveal over half of the generating capacity taken offline in 2017 was coal-fired. Meanwhile, the US didn’t add any new coal power generators. The EIA’s projections suggest this should continue. At the same time, utilities added more natural gas generators, suggesting it will widen its lead as the largest source of power generation capacity in the years to come.[ii] The fact it is cleaner burning is, to us, the coup de grâce. As more coal-fired plants come offline, coal demand falls further. As a result, producers are churning out less and less of it lately.

Exhibit 3: US Coal Production

Ultimately, this is an industry in long-term decline globally, overmatched by a more efficient, cleaner fuel that is nearly as cost efficient. Policy changes might score political points, but there isn’t clear evidence the new system provides incentives for states to tolerate higher levels of greenhouse gas emissions or that utilities will be inclined to use them—even if states do. Moreover, nothing at the federal level prevents states from imposing stricter environmental standards that further the push towards natural gas and renewables and away from coal. Simply allowing states to let utilities use more coal when economic reasons are driving them away is likely a nonstarter for coal stocks.

[i] Source: FactSet, as of 8/28/2018. MSCI USA Investible Markets Index (IMI) Coal and Consumable Fuels subindex total return, 3/23/2011 – 1/20/2016. IMI indexes are designed to capture the return of 99% of market cap (large and small cap) for a given region/country/sector. We used it here because coal stocks are mostly teensy.

[ii] “Electricity Generation From Fossil Fuels Declined in 2017 as Renewable Generation Rose,” Owen Comstock, US Energy Information Administration, Today in Energy, 3/20/2018. https://www.eia.gov/todayinenergy/detail.php?id=35412

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today