Personal Wealth Management / Market Analysis

Will Oil’s Bounce Boom or Bust?

What to make of oil's recent rally.

Oil's drop below $40-a two-week low-made headlines Tuesday, prompting the usual speculation about where the commodity is headed next. Did black gold just hiccup in a broader rally, or is it about to resume its longer-running decline? As ever, we caution investors against focusing on oil's day-to-day movements. Look instead to its economic drivers, which show supply still exceeds demand. Though this means prices likely won't soar any time soon, markets have dealt with this reality for a while, and dirt-cheap oil isn't a negative.

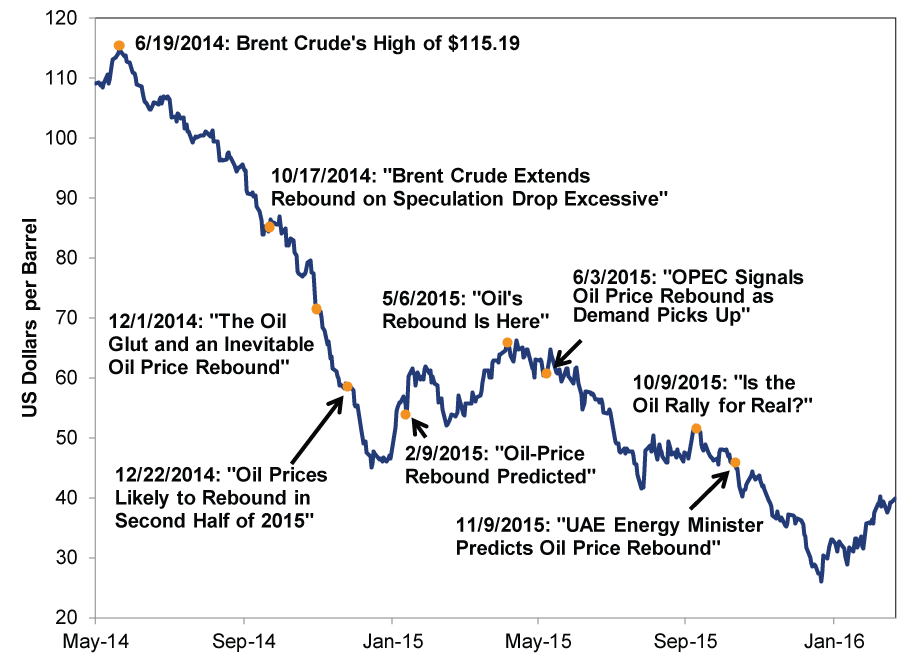

Oil's volatility has been popular headline fodder, and over the past two months, many grew convinced its price had finally bottomed out. After a bounce near January's end, other news-like an industry report forecasting a quickening decline in US oil output this year-seemingly stabilized prices. From January 20 - March 21, a barrel of Brent crude rose more than 50%, from $26.01 to $39.91.[i] And hey, perhaps January 20 will indeed mark oil's low. We will only know in hindsight. However, there have been plenty of false alarms over the past 21 months. (Exhibit 1) We won't venture a guess about oil's low. Trying to time any asset's next short-term move is an exercise in futility.

Exhibit 1: When Exactly Did Oil Rebound?

Source: St. Louis Federal Reserve, as of 3/29/2016. Crude oil prices: Brent crude, from 5/30/2014 - 3/21/2016. See headlines, in chronological order, here, here, here, here, here, here, here and here.

Oil prices probably will stabilize at some point, if they haven't already, though supply and demand drivers suggest they're unlikely to soar any time soon. The world has been awash with oil, with producers globally pumping record numbers. Powered by the shale oil revolution, US production has skyrocketed. In 2015, the US produced 3.4 billion barrels of crude-a level exceeded only in the early 1970s. Inventories are robust, with crude stockpiles exceeding 80-year highs. But stabilizing forces are appearing. Rig count tumbled last year as producers cut investment, and exploration has fallen off a cliff. Output has been slow to adjust, but it looks like that's about to change as experts have lowered their estimates for 2016. Some expect shale oil production to fall by 600,000 barrels a day this year and another 200,000 barrels a day next year, while global demand growth is expected to slow a bit, too. Though these two forces may help stabilize prices, there is a counterbalance. A substantial amount of shale oil remains in "fracklog"-untapped wells that can be turned on in a jiff when markets provide a worthwhile price point for producers.

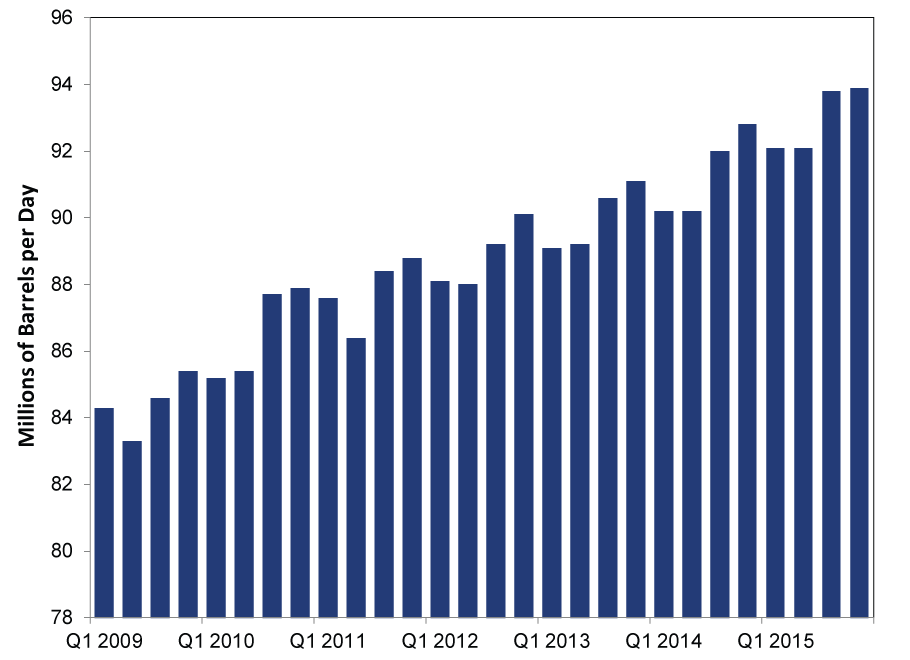

Foreign production, particularly in the Organization of the Petroleum Exporting Countries (OPEC), is more of a wildcard. Determined to maintain its market share, OPEC has kept up production despite dissension from some members who want to cap output to prevent prices from falling further. The cartel produced an average of 33.2 million barrels of oil per day in 2015-the second-highest on record. The most recent data suggest output is rising, not falling, and this doesn't look likely to abate any time soon. With sanctions lifted, Iranian supply is rising, offsetting outages in smaller producers. Kuwait and Saudi Arabia are set to resume production at a joint project, an oil field that generated about 300,000 barrels of oil per day before closing in 2014. And even though non-OPEC member Russia announced it might coordinate a freeze with other producers, its output is still at record levels-it isn't reducing supply, merely keeping it steady. Global demand is still growing, too, but not as fast. (Exhibit 2)

Exhibit 2: Total Oil Consumption by Quarter Since 2009

Source: FactSet, as of 3/29/2016. Oil consumption, total world, in millions of barrels per day, from Q1 2009 - Q4 2015.

While falling oil prices generate lots of chatter, they aren't an absolute good or bad for the broader economy. They have generated both fear and enthusiasm in various corners, but it's mostly overstated. Fear of faltering global growth abounds since cheap oil has hit Energy-heavy economies, particularly Brazil and Russia. On the home front, some worry oil-related job losses could whack consumer spending, triggering a vicious circle. Fears about "toxic" energy debt-and the potential fallout on bank balance sheets-are persistent. On the more positive front, lots of folks think cheap oil is a boon for consumers, who will have more money to spend elsewhere-and are disappointed this hasn't materialized yet.

But these perceptions are exaggerated or wide of the mark. While we don't diminish the human impact of job losses, this isn't a macroeconomic negative. The US economy overall is strong and diverse enough to offset those losses through jobs in other fields-see Texas as Exhibit A-and employment doesn't lead consumer spending. The same is largely true globally, as growth in most of the world offsets the economic troubles in oil-heavy nations. Brazil and Russia are struggling but remain too small to cause recession globally. Energy debt comprises just 3% of total loans in the US, and banks have built buffers against potential loan losses. As for the allegedly missing spending boost from cheaper gasoline, the impact here is a bit misunderstood. Gasoline spending is part of total consumer spending . Folks don't suddenly have more money to spend-rather, they keep more of their current income to spend elsewhere (or save or repay debt). Thus, the impact is at best zero sum. Spending might shift to more discretionary goods and services, creating winners there, but hopes for a jump in spending overall are largely unfounded.

All that said, much of oil's negative impact on the economy has probably passed. Producers have already taken their lumps and cut costs dramatically-survivors are leaner. More cuts could follow, but the base is already quite low. Meanwhile, on the revenue side, with much of oil's slide likely behind us, the Energy sector's poor year-over-year sales benchmarks will probably start looking better, weighing less on earnings and revenues moving forward. As we have long pointed out, Energy companies have obscured Corporate America's overall strength. With 99% of S&P 500 companies reporting as of March 24, Q4 earnings fell -3.6% y/y.[ii] But excluding Energy, earnings grew 2.7% y/y.

Once Energy earnings stabilize at low levels and stop dragging down the headline number, strength elsewhere will become much more apparent. As investors get wise to the fact things are better than they feared, their relief should be positive for stocks.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Golden Paradox2026-03-24

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today