Personal Wealth Management / Politics

Your Global Investing Lesson From Malaysia's 'Populist' Victory

A US-listed Malaysian ETF’s sharp reaction to last week’s election teaches the importance of being patient.

On May 9, Malaysia held an election in which a ragtag populist coalition took on the establishment party that had governed since the country’s 1957 independence. Defying polls and expectations, the populists won, drawing comparisons with Brexit and President Trump’s election. Echoing both of those events—and scared of anything associated with the P-word—headlines warned of market mayhem in the aftermath. Incoming Prime Minister Mahathir Mohamad called a three-day market holiday, leaving investors on the edge of their seats. But some folks didn’t wait for markets to reopen, instead trading the US-listed iShares MSCI Malaysia ETF (EWM)—just as they traded a Greek ETF when Greek markets were closed after the infamous 2015 referendum on the bailout. Needless to say, it plunged. But then it bounced. By market close on Monday, it was back at pre-election levels. Meanwhile, when Malaysian markets re-opened Monday, they rose a wee bit. Let this be a lesson: Markets don’t have preset reactions to geopolitical events and often do what few expect.

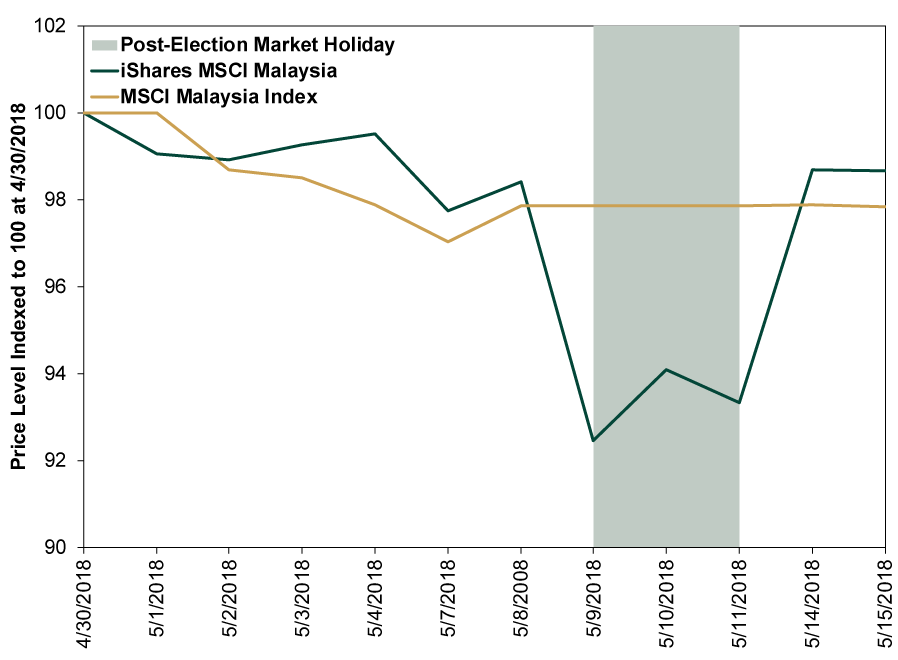

Exhibit 1, which plots EWM and its underlying index before and after the election, underscores the benefits of staying patient and not overreacting to loud media narratives.

Exhibit 1: The Importance of Being Earnest

Source: FactSet, as of 5/15/2018. EWM and MSCI Malaysia price level in USD, 4/30/2018 – 5/15/2018.

Whenever you are confronted with a popular market narrative, the wisest course of action is to think critically. Try to pick it apart. Explore whether there are fundamental reasons it should hold true. Just as there was no reason for the Brexit vote or Trump election to be automatically bearish for stocks, nor was there any fundamental reason for Malaysia’s opposition’s victory to bring market doom. While labeled in broad brushstrokes as populism, it was actually a case of voters picking the rule of law, transparency and accountability over a corruption-riddled status quo. Google “1MDB,” a scandal involving Malaysia’s government, the state-run investment fund and, um, Leonardo DiCaprio, and you will see what we mean.[i]

Oh, and about those “populists”? Beware of labels. We are politically agnostic, as always, but we think it is important to note that the opposition leader, Mahathir, is a 92 year-old former prime minister who broke with his party last year, taking a stand against corruption, and rallying other like-minded politicians who were tired of graft. His signature pledge? Freeing political prisoners, including the longtime opposition leader, Anwar Ibrahim—jailed on what The Wall Street Journal describes as “trumped-up charges”—and pledging to cede the position of prime minister to him within two years (provided he wins a parliamentary by-election). On Wednesday, Mahathir followed through, securing a pardon for Ibrahim, who is now a free man. Might we also mention that this is the country’s first real transition of power in its history? You might say that until last week, Malaysia’s democracy remained untested. Well, it just passed.

Those warning of a negative market reaction largely conceded these long-term positives, pointing instead to some of Mahathir’s economic-related campaign pledges, including restoring fuel subsidies, which they worried would jeopardize the country’s credit rating and standing in international capital markets. Yet it seems to us like this fear is a ghost from Malaysia’s past—specifically, the Asian financial crisis, which it narrowly escaped without IMF assistance. A wider fiscal deficit isn’t inherently bearish, particularly in a fast-growing, modernizing country like Malaysia. Projecting what credit ratings agencies will do is speculating on largely feckless factors. Other proposals, including rolling back a goods and services tax scrapping toll fees and raising the minimum wage might create winners and losers, but this doesn’t amount to a radical economic policy shift. On the contrary, Mahathir has pledged to lead a business-friendly administration and appointed a former central banker and finance minister to his team.

Maybe it turns out eventually that he doesn’t follow through with the good stuff and only implements bad stuff, but you can’t know that now. Certainly couldn’t last Wednesday either. Watch what politicians do, not what they say. Or, more accurately in this case, what media says of them.

So the next time you read about some political development being automatically bad for markets, don’t rush to conclusions. Instead, remember markets price in all widely known information, including popular opinions, and look for ways those popular opinions might be wrong.[i] Leo wasn’t implicated in any wrongdoing. He just had the misfortune, along with other Hollywood A-listers, of receiving gifts from a financier/Hollywood hanger-on who bought the items in question with money embezzled from the fund.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics Q2 US GDP’s Stealthy Strength2026-07-31

-

Expert Commentary This Week in Review | Fed Meeting, US GDP, Eurozone GDP

2026-07-31

2026-07-31 -

Market Analysis Don’t Fret the EU’s Low Summertime Gas Storage Levels2026-07-31

-

Economics On Fires and GDP2026-07-30

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today