Personal Wealth Management / Market Analysis

Your Last Investing Lesson From France’s Election

French elections show stocks price in likely outcomes swiftly, often leaving hesitant investors behind.

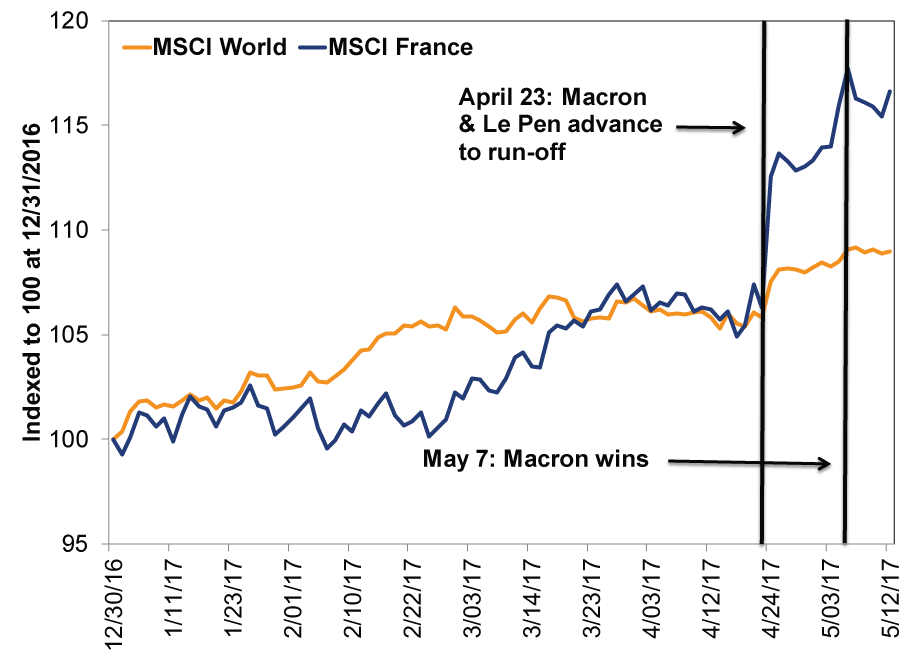

On May 7, French voters went to the polls and turned away an allegedly existential threat to global markets in anti-euro candidate Marine Le Pen, electing independent centrist Emmanuel Macron instead. With catastrophe supposedly averted, French stocks ... fell? Why the lackluster response? The answer: Markets didn't wait for French polls to close before pricing in the likely outcome, bypassing investors awaiting the certainty of a final result. Let this be a lesson: Waiting for full clarity is costly.

In the run-up to the French vote's first round, markets were skittish. Among 11 initial candidates, 4 had a shot at advancing to round two: Marine Le Pen, Jean-Luc Mélenchon, FranÇois Fillon and Emmanuel Macron. The latter two were relatively centrist and pro-euro, but the far-right Le Pen and far-left Mélenchon had no love for Brussels. Polls showed Fillon and Macron trouncing Le Pen-the polling leader-in a hypothetical round two, but folks worried they wouldn't have the chance when Mélenchon made a late polling surge. Even though he trailed Fillon and Macron, investors remembered polls being wrong before Brexit, the US election and Britain's 2015 election, and they feared an all anti-euro Le Pen vs. Mélenchon runoff.

But on April 23, as polls predicted, the race narrowed to Le Pen versus Macron, the former Economy Minister who started his own political party, En Marche. Given Macron's 20 percentage point advantage-well beyond most margins for error-the runoff outcome was never in much doubt. French markets surged, correctly anticipating Macron's victory-and by the time the results were tallied, they had moved on, actually dropping in the days following the second vote. It was a classic "buy the rumor, sell the news" scenario.

Exhibit 1: French Stocks Leap Before Macron's Election

Source: FactSet, as of 5/15/2017. MSCI World and MSCI France Indexes with net dividends, 12/31/2016 - 5/12/2017.

This highlights a crucial feature of stocks: They don't wait for uncertainty to fall, but rather rise as it falls and doubts fade. Waiting for doubts to disappear keeps investors on the sidelines, missing potentially big gains. This is especially true ahead of widely anticipated events: Efficient markets are incredibly good at pricing in probabilities beforehand, bypassing wait-and-see investors. As Fisher Investments founder Ken Fisher often quips, it's what they do for a living. Even with a surprise outcome, markets digest the news and move on long before pundits cease hyping dangers-as they did following the Brexit vote and Trump's win.

While French stocks have moved on from the election, falling uncertainty should remain a tailwind for Europe over the foreseeable future. General elections are scheduled in the UK (June), Scotland (also June), Germany (September) and Austria (October). As each comes and goes, investors should increasingly get over political jitters and refocus on Europe's underappreciated economic strength.

This strength isn't new-eurozone GDP has grown for 16 consecutive quarters, most recently outshining the US in Q1. Forward-looking indicators appear promising as well: The Conference Board's Leading Economic Index for the eurozone is high and rising. March's 0.7% m/m rise was the eighth straight, with the yield spread-the difference between long- and short-term interest rates-contributing most and nearly doubling since October. Steeper yield curves generally boost lending and money supply by making loans more profitable-and sure enough, bank lending to eurozone households has been positive since late 2014, and grew 2.4% y/y in March, while M3 (a broad money supply measure) rose 5.3%. In the US, by contrast, lending and broad money supply are slowing as the yield curve flattens-another sign Europe seems poised to continue outperforming.

Despite its relative strength, many don't see Europe's sunny reality. Most call it a fragile recovery, not realizing GDP has been charting new highs since 2015. But thinning political fog should help investors see the economy consistently beating expectations. It seems to us Europe's surprise potential is far from tapped out, and as investors start fathoming the expansion, European stocks should benefit long before the political all-clear sounds.[i]

[i] Which, frankly, it probably never will.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 9 - March 132026-03-16

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today