Personal Wealth Management / Economics

Your No-Spin Look at Q3 US GDP

Q3 GDP data confirm the US economy remains on firm footing.

Q3 US GDP rose 3.5% annualized—a slowdown from Q2’s 4.2% but still good for the third-fastest rate in four years.[i] The report had something for everybody. Optimists cheered the strongest consumer spending since Q4 2014, while pessimists groaned about the weakest business investment since 2016. Pols on both sides of the aisle found talking points: Economic growth is on track to hit the Trump administration’s 3% target, but trade policy was a headwind slamming certain industries. For investors, we suggest stripping away the narratives. Q3’s GDP report had plenty of interesting tidbits, but overall, the broader picture remains the same: The US economy remains on firm footing, bolstered by its strong private sector and domestic demand.

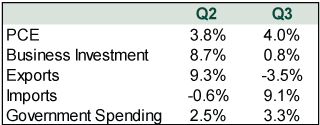

Here is a table comparing how Q3 figures squared up with Q2’s.

Exhibit 1: A Tale of the Tape

Source: BEA, as of 10/31/2018. Annualized growth rates for Q2 and Q3.

Diving a little deeper, personal consumption expenditures (PCE) hit 4.0% for the first time since Q4 2014—a positive since consumer spending comprises nearly 70% of GDP. Business investment also wasn’t uniformly weak. Investment in structures (-7.9%) was the primary detractor, largely attributable to the Oil & Gas industry, but positively, investment in intellectual property products rose 7.9%. Change in private inventories also contributed a big 2.1 percentage points after detracting -1.2 percentage points in Q2.

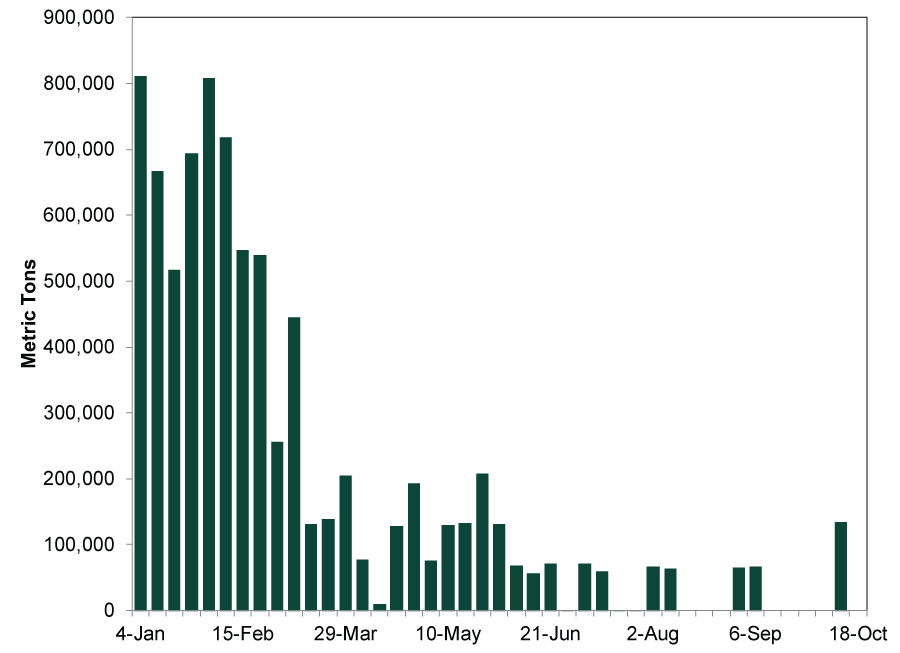

As usual, folks spun the data to support their story—especially with midterms set for next week. Depending on who you ask, Q3 GDP is evidence of a government that is either business friendly and pro-growth or shortsighted and reckless. In our view, these interpretations ascribe too much credit/blame to politicians. That doesn’t mean they have no effect on GDP growth! For example, tariffs probably pulled some activity forward, as reflected in trade data. Exports rose 9.3% in Q2 before contracting -3.5% in Q3. Many farmers front-loaded shipments to China before tariffs took effect in July, and soybean exports specifically have been plunging since then.

Exhibit 2: Direct Soybean Exports to China Have Fallen and Cannot Get Up

Source: US Department of Agriculture, weekly soybean exports to China, 1/1/2018 – 10/18/2018.

Similarly, Q3’s higher imports are likely evidence of businesses’ getting ahead of import duties going into effect in late Q3, further echoed by the big swing in inventories. Whether this is a positive or not remains to be seen. If businesses overstocked relative to future demand, it could represent wasteful spending. If they didn’t, then fine—they beat tariffs, mitigating their impact. In this way, inventory change’s treatment is one of GDP’s more nuanced quirks—a reason GDP’s ability to reflect the actual economy is more limited than many presume.

Another GDP limitation: it treats government spending as a positive. Government spending has accelerated this year, and The Wall Street Journal recently found that, “When including faster spending on nondefense items and spending at the state and local levels, increased government spending accounted for 0.34 percentage point of the 0.7 percentage point increase in the growth rate since April 2017, or nearly half.”[ii] In our view, higher government spending isn’t an automatic positive. All things equal, we believe the market-driven private sector is a better allocator of resources. However, fears about the costs of higher government upping—i.e., taking on more debt and driving an unwieldly budget deficit—seem off to us, too. US debt is far from problematic, both today and for the foreseeable future. As we wrote recently, “US interest payments also remain quite low by historical standards, compared to both federal spending and tax receipts. … National debt becomes a problem only when countries struggle to service it—and serving Treasurys is currently a breeze.”

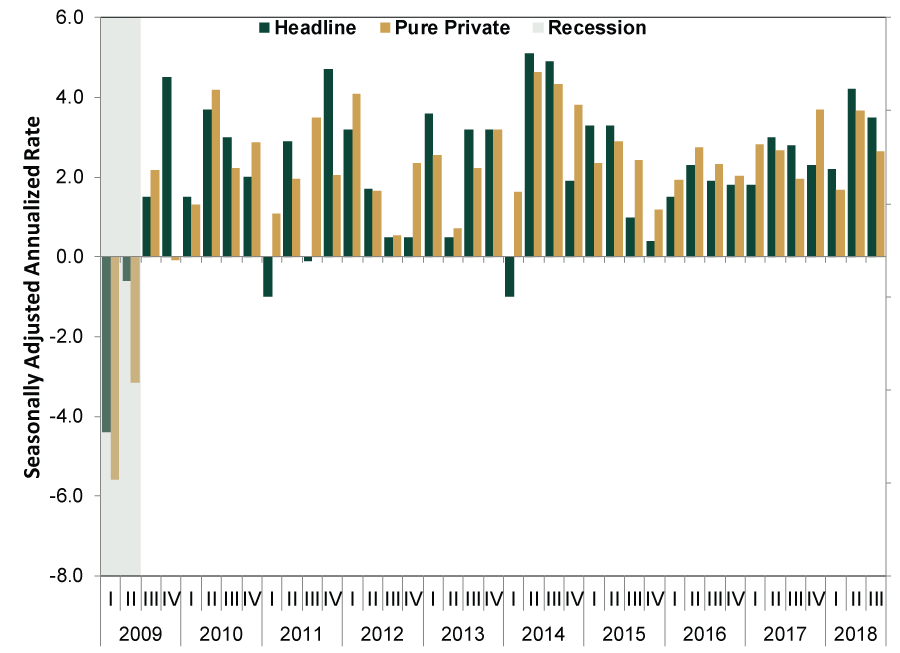

Take a broader view, and Q3 doesn’t stand out much compared to prior quarters. From both a headline and a “pure private sector” GDP—PCE, business investment and residential fixed investment—perspective, Q3 2018 is solid and in line with the past several years.

Exhibit 3: Headline and Pure Private Sector GDP Since 2009

Source: US Bureau of Economic Analysis, as of 10/26/2018. US GDP seasonally adjusted annualized rate, Q1 2009 – Q3 2018.

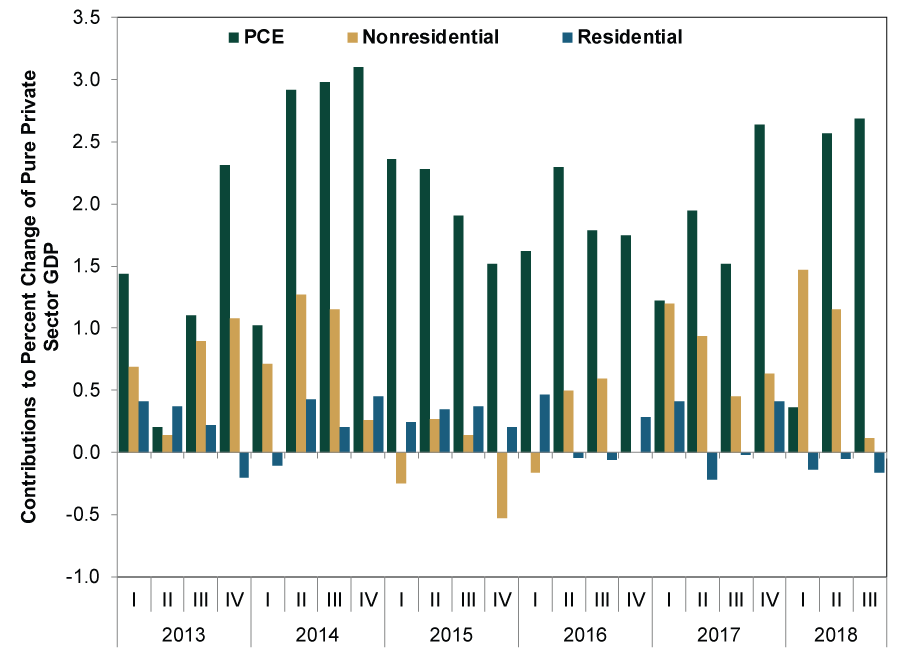

Moreover, consumer spending remains the biggest contributor to pure private sector GDP—as it has over the past several years.

Exhibit 4: Consumer Spending Remains a Top Contributor

Source: US Bureau of Economic Analysis, as of 10/26/2018. Contributions to percent change of GDP for PCE, nonresidential fixed investment and residential fixed investment, Q1 2009 – Q3 2018.

Q3 GDP is the latest evidence of US economic strength. Though the data are old news for stocks, forward-looking economic indicators suggest growth should continue. Given how recent negative market volatility and other scary stories have dominated headlines, these positive data show economic reality is better than many seem to appreciate—reason to remain bullish, in our view.[i] Source: BEA, as of 10/26/2018. Note: This citation applies to all GDP data referred to in this article unless specified otherwise.

[ii] Source: “A Big Reason U.S. Economy Is Accelerating: Government Spending,” Kate Davidson, The Wall Street Journal, 10/25/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics A May Global Economic Check-In2026-05-26

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 18 - May 222026-05-26

-

In The News How to think about the Iran war — and what it means for oil and stocks2026-05-25

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, US Q1 GDP, Graduation Season

2026-05-25

2026-05-25

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today