Personal Wealth Management / Market Analysis

11 Reasons to Be Grateful This Thanksgiving

For investors, scoop a healthy portion of these positive tidbits to go along with your turkey this Thanksgiving.

With Turkey Day looming, your friendly MarketMinder editorial staff is in a thankful mood. As eventful-and at times, difficult-as 2016 has been, there are lots of positives, too. Here are 11[i] things investors can be thankful for.

The Election Is Over

Whatever your feelings about President-elect Donald Trump, we are thankful election coverage is finally over. Besides the contentious presidential election, state and local elections-and their accompanying talk and hyperbole-are done, which is itself worthy of thanks.[ii] Even for politics aficionados, the sheer amount of noise has likely been a bit much. However, don't expect the media to quiet down. Though election advertising and campaign-trail mudslinging is over, the media has already started attacking the president-elect, and the critiques will probably only intensify. It is likely we will see a much more aggressively anti-administration media than in the last eight years, so those hoping for quiet will have to look elsewhere.

That said, the uncertainty surrounding who will be 45th president is gone. Already, President-elect Trump has started forming his cabinet and telegraphing his priorities for his first 100 days in office. It doesn't mean he'll do everything he says-politicians, experienced or not, tend to have ... ummm ... fuzzy memories when it comes to campaign pledges. Plus, we don't expect Trump and a GOP-led Congress to necessarily get along swimmingly-many Republican lawmakers oppose Trump's policies[iii] and aren't likely to let the president-elect do as he wishes. This intraparty gridlock means the passage of big, sweeping legislation isn't likely-an underappreciated, bullish positive.

Improving Corporate Earnings

With Q3 2016 earnings season nearly complete, it seems the much-ballyhooed "earnings recession" is over. With 481 companies reporting as of 11/18/2016, earnings growth is 3.0% y/y-far better than estimates of -2.0% at the quarter's onset.[iv] Though Q3 should end a streak of five consecutive quarterly S&P 500 earnings declines, we always thought that "earnings recession" moniker mischaracterized reality. Ever since oil prices plunged more than two years ago, Energy sector earnings have been the key drag. Excluding it, earnings only fell in one quarter during that negative streak, and this quarter, earnings grew 6.6% excluding Energy, easily exceeding initial expectations of 1.3%.[v] However, with oil prices' stabilization and the dramatic declines now falling out of the year-over-year comparisons, Energy is no longer weighing down the headline number as much. Its drag should vanish in coming quarters, contributing to an expected earnings growth pop in Q4 and beyond.

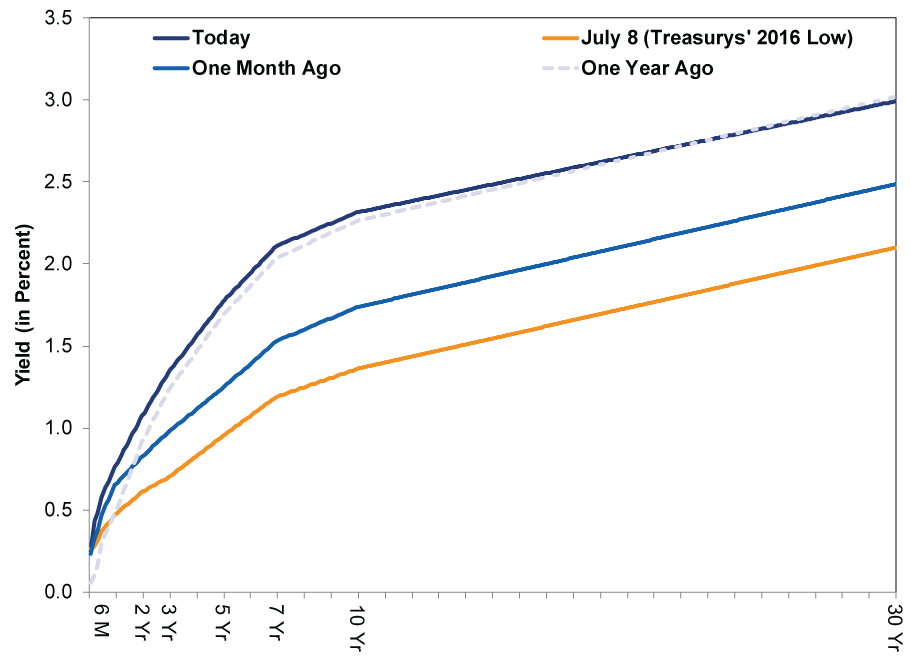

Steepening Yield Curve

In other positive economic news-this one meaningful for future growth-the yield curve continues steepening. The yield curve refers to the distribution of bond yields across all maturities from one borrower. The spread is the difference between long-term rates and short-term rates, and it acts as a proxy for banks' loan profitability. Because banks' core business is to borrow short term and lend long, a positive spread means banks get more bang for their buck-and thus, would be more willing to lend. If businesses and individuals have easier access to capital, they can use that money in whatever productive ways they see fit-goosing growth. For this reason, the yield curve's shape is widely considered a very reliable indicator of future economic conditions. After some concerns earlier this year about a flatter yield curve, the spread has widened again in recent months-a positive few are cheering. (Exhibit 1)

Exhibit 1: US Treasury Yield Curve Have Steepened

Source: FactSet, as of 11/22/2016.

Global Growth Beyond US

Outside the US, data show global growth continues. Across the Atlantic, eurozone GDP grew 0.3% q/q (1.4% annualized), its 14th consecutive quarter of growth.[vi] Though not all 19 members have reported yet, growth is broad-based, from economic behemoth Germany (0.2% q/q) to smaller Portugal (0.8% q/q). Even beleaguered Greece[vii] grew!

In Asia, Hong Kong grew 1.9% y/y, accelerating from 1.7% in Q2, while Malaysia (4.3%), the Philippines (7.1%) and Thailand (3.2%) also expanded on a year-over-year basis in Q3. And in Latin America, Mexico picked up from Q2's 0.2% q/q in a big way, growing 1.0%, while Chile grew 1.6% y/y in the same quarter. So while think tanks fret and politicians push policy plans to pump up growth, economies keep grinding higher.

Five Big False Fears That Haven't Come to Pass

The second-longest bull market continues climbing the proverbial Wall of Worry, overcoming many false fear bricks-sometimes the same brick several times over. After Brits voted to leave the EU in June, many projected big bad Brexit fallout. Yet it is nearly entirely absent-not surprising to us, considering nothing has changed economically (and won't change until negotiations, which haven't even started yet, are complete). That oft-feared Chinese economic "hard landing" has yet to materialize, as the world's second-largest economy continues expanding at a slower-though still robust-rate. A deflationary spiral of doom didn't knock economic growth, and actually, inflation has been picking up as energy prices have stabilized and are no longer dragging down headline CPI. Folks are now worried about accelerating inflation, which says a lot about sentiment, as higher inflation needn't hurt future growth prospects, either. While experts warned the next US recession would hit soon, these forecasts aren't new-and they haven't been right yet. More importantly, forward-looking economic data (e.g., The Conference Board's Leading Economic Index) don't suggest the US economy will meaningfully weaken for the foreseeable future. And finally, remember all those worries about the negative market fallout if Donald Trump surprisingly won the election? Well, besides some ultra-brief volatility in futures markets election night, broader markets have largely risen since Trump's win. This doesn't mean stocks "prefer" Trump. Rather, it's likely reduced political uncertainty allows investors to see the brighter-than-appreciated world around them.

Innovation in All Things

While folks focus on false fears, wonderful technological innovations keep surprising us in positive ways. US oil producers have found ways to make hydraulic fracturing even more efficient. Drone technology continues making headway, with drones delivering pizza in New Zealand. And for all the concerns Moore's Law-the theory semiconductors' computing powers will double every two years-was reaching its limits, some innovative researchers are testing new ways to boost computing power. We don't know how technology and innovation will develop long term-but as long as they are incented by profit and free markets, we believe folks in capitalist societies will continue wowing us with fascinating discoveries that improve the world. Stocks offer you a slice in that process and a share in the financial rewards.

Positive Side Dishes

Thanksgiving dinners are cheaper now compared to 20 years ago. Be nice to the therapy dogs you see at the airport. Some retailers can't wait to get the shopping started. Super Mario is coming to your phone. The Gilmore Girls revival.[viii]27 rules for your family Thanksgiving touch football game. Montana is looking for the best Brussels sprouts recipe for Thanksgiving. Bacon Turkey! And like Black Friday discounts, we believe calories are half off on Thursday.[ix]

[i] Partly because it's November and partly because we believe we need to take this commentary to 11.

[ii] Particularly those of us who live in Oregon and were subjected to an onslaught of Measure 97 coverage.

[iii] To the extent they exist.

[iv] Source: FactSet Earnings Insight Report for weeks ending 11/18/2016 and 9/9/2016, as of 11/22/2016.

[v] Ibid.

[vi] Source for all these GDP numbers: FactSet, as of 11/22/2016.

[vii] Greece! Yes, that Greece !

[viii] One of our editors made us do it.

[ix] We aren't health experts, and this isn't medical advice.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics The Tenth Question Facing Alberta2026-08-06

-

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today