Personal Wealth Management / Economics

A Web of Misperceptions

A look at some misperceptions we came across in our regular internet perusal Tuesday.

A look around the web at some common misperceptions—and some alternative perspective to consider.

So went January...

January’s officially in the books, and the MSCI World returned 5.05%i—one of the strongest Januarys in recent memory.

Following the January Effect’s logic, we can all count on a gangbusters 2012, right?

Well, not necessarily. It’s true very strong January’s like the one just finished are frequently followed by strength in the rest of the year, but that’s not a causal relationship, just an interesting observation. A strong or weak single month—January or any other—doesn’t guarantee the months following will follow suit. So using one month’s returns to predict an entire year, either in the same or opposite direction, isn’t sufficient—regardless of whether said month is up, down or flat. What moves markets in January doesn’t necessarily move them over the next 11 months. Many other factors—some perhaps completely unfathomable to folks today—will come into play, and markets will discount these without a second thought to January.

So what should investors look to as 2012 continues? Fundamentals! As we’ve written, though volatility could very well continue and risks exist (as always), we’ve noticed several underappreciated fundamentals that seem likely to provide strong tailwinds for stocks this year. These include a robust US private sector, healthy global demand and a growing global economy, to name just a few.

Sinophobia

Sunday, the New York Giants face the New England Patriots in Super Bowl XLVI. For certain: One will win; the other won’t.

Some believe similar logic applies to our economic relationship with China—one winner, one loser. And many believe China’s currency policy is unfair, rigging the game and creating many economic problems. To fix this, some suggest politicians somehow level the playing field.

While China’s currency may be undervalued, claiming yuan policy is responsible for a host of economic ills is going too far. It’s true the US has consistently run a trade deficit with China since 1985—where most discussion seemingly starts. But as we’ve written, imports are not an economic scourge, stealing jobs and plaguing America—even those from undervalued-currency China, as economist Dr. Mark J. Perry eloquently explains.

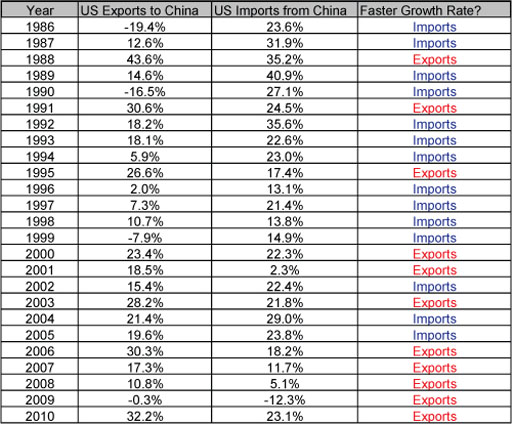

And focusing on the trade gap obscures other, much more significant developments. Exhibit 1 helps illustrate one such change in our relationship with China.

Exhibit 1: Annual Growth Rates of US/China Trade

Source: US Census Bureau.

While import growth outpaced export growth most years from 1986 through 1999, since 2000 the opposite is true: US exports to China grew quicker in 8 of 11 years. And 2011 data through November show it’ll likely be 9 of 12.

China’s fast economic rise has brought a developing middle class—one demanding more imported goods. In fact, US exports to China have grown from about $16 billion in 2000 to over $94 billion in 2011 through November. No, the Chinese don’t consume our imports in the same volume we do theirs. But what else would you expect? China’s per capita GDP was 117th globally in 2011; the US is 11th.[i]

Our economic relationship with China is actually win-win even if the yuan’s undervalued. However, history shows one easy way to make it lose-lose is a government attempt to make trade “fair.”

Questioning consumers’ confidence

January’s US Consumer Confidence index dipped to 61.1 from December’s 64.8. But as we’ve covered before, confidence and sentiment indexes tell us little-to-nothing about the direction of markets or the economy.

One flaw (among a few) in confidence or sentiment indexes is they’re almost always based on a survey of how folks felt at a single, now-past point in time. But people’s feelings change all the time. That’s why what people felt (a couple weeks or a month ago) and what they do (today) are frequently two very different things. Case in point: Confidence surveys aside, US retail sales have consistently shown strong growth (in December, retail sales were up 5.5% year over year) and remain near recent highs.

Speaking of wonky indicators ...

As unemployment numbers have remained (predictably, as we’ve said) elevated in the recession’s wake, some have sought scapegoats. Seemingly popular is some version of “it’s technology’s fault,” which goes something like: Because of improved technology in [fill-in-the-blank] field, fewer workers are necessary to produce the same output, thereby displacing workers and actually contributing to an unemployment dilemma.” The other common strain is to blame cheap, foreign labor that can perform similar tasks to US laborers for significantly lower wages.

Both views, though, express a similar basic fear of societal progress and ignore the widespread benefits such progress redounds on all Americans regardless of income or profession. After all, consider just a few short years ago, only the very wealthy could afford computers at all, let alone tablets, smart phones, etc. with Internet connections. Now, they’re ubiquitous. Over time, productivity is a powerful force pushing prices down.

In our view, there’s little to fear from American manufacturing (and other industries) becoming increasingly productive over time. Making technology more broadly available at cheaper prices benefits not only Americans but the world. Hardly seems something to bemoan—rather, something to cheer amid continuing efforts to fight the scourge of global poverty.

iSource: Thomson Reuters.

ii Source: CIA World Factbook.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today