Personal Wealth Management / Behavioral Finance

Counterproductive Cash Cushions

When you get down to it, keeping a cash cushion so you can buy on the dips is a rather bizarre tactic.

Cash beat stocks and bonds in Q1, which has some saying it deserves greater emphasis in your portfolio: Keep some cash, they argue, to both cushion the blow when markets tumble and give you firepower to buy on the dips. Sensible as this might seem on the surface, we think it raises some tricky questions, like: If you buy on the dip, when and how do you raise a new cash cushion for the next pullback? Is this just market-timing by another name? Pick it apart, and we think it becomes clear the biggest beneficiaries are the brokers collecting commissions from all this cushion-stuffing and dip-buying.

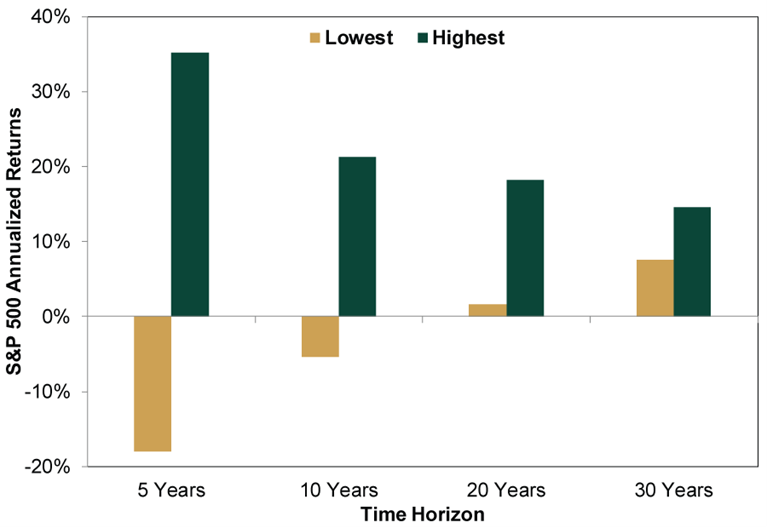

The “volatility cushion” argument overrates the impact of short-term wobbles on an investor’s long-term returns. While sitting through turbulence isn’t fun and wanting to avoid (or lessen) its impact is natural, corrections and pullbacks don’t prevent disciplined long-term, growth-oriented investors from reaching their goals. US stocks’ roughly 10% long-term annualized returns since 1926 include not only 13 bear markets, but also scores of lesser zigzags along the way.[i] As Exhibit 1 shows, stocks have never had a negative return over any 30-year rolling period during this window (based on month-end values). Rather, the lowest return was 7.5% annualized, from August 1929 to August 1959.

Exhibit 1: Stock Returns Diverge Less With Time

Source: Global Financial Data, Inc. and FactSet, as of 4/2/2018. Highest and lowest annualized 5-, 10-, 20- and 30-year monthly rolling S&P 500 total returns, 12/31/1925 – 3/31/2018.

Bull market returns far outweigh bear market drops. But earning them requires owning stocks during bull markets. We aren’t preaching buy-and-hold here. We believe bear markets—long-lasting, fundamentally driven drops exceeding -20%—are possible to identify early enough that trying to avoid them can be helpful. (Helpful—not necessary.) But that doesn’t apply to corrections[ii] and smaller pullbacks, which occur frequently and without warning throughout bulls. Overreacting to these introduces risks. If you sell after a drop, you lock in losses. If markets just as suddenly recover, and you mistime re-entry, you may end up paying a higher price. Or worse, not get back in at all, forgoing any future gains.

For investors, what matters aren’t the day-to-day or even month-to-month wiggles, but the total return over their entire time horizon. For those entering retirement now, that could easily be 30 or more years as life expectancies extend. Keeping cash on hand during a bull market detracts from those returns. Although the lure of cash as presumed “safety” may seem strong when volatility strikes, heeding its siren call can cause you to miss out on the bull’s gains.

“Buy the dips” sounds good, but we don’t think it is realistic. Dips are when most folks least want to buy. Corrections often end before the big fear associated with them fades away—because nothing fundamental is driving stocks down, just the fear (itself). But lingering headline risks extend fear, making it emotionally difficult for many folks to invest. Case in point: The S&P 500 tested its low point April 2, but since then it is up 3.2%,[iii] albeit choppily. Current headlines are blaring about trade wars, exploding deficits, Fed machinations, White House turnover, Tech’s travails and technical breakdowns, to name a few. Have we seen the bottom, and is it now time to put that cash cushion to work? Or is there another leg down? Headlines might make you believe much more pain awaits. But what if you raise more cash just as the market unexpectedly rebounds? If you miss it, you may feel dejected—like you might during a dip—but with the additional downside of feeling left behind.

Most folks aren’t robots with nerves of steel. Trading against the market—consistently and successfully—is exceedingly difficult! It is even more so when your emotions run high and life savings are at stake. “Time in the market is more important than timing the market” may be a catchphrase, but we think investors who take it to heart are more likely to see higher lifetime returns. Otherwise, you are committing to market timing for the entirety of your time horizon, with all the execution risks and potential mistakes that entails. Plus, consider the transaction costs: Given the relatively high frequency of corrections and pullbacks in bull markets, even if perfectly timed, will the money saved through all this trading outweigh its brokerage commissions and potential capital gains taxes? Or will your brokerage firm and the IRS be the biggest winners?

Overall, the lesson is pretty simple: If you need stock market-like returns for some or all of your assets, you should be in stocks much more often than out. In practice, it isn’t always easy or obvious, but it is better than the alternative—increased trading, fees, complexity and myopia—likely leading to lower returns. Raising cash randomly jeopardizes the returns you need! Instead, keep a longer perspective, and remember timing volatility is a good way to shoot yourself in the foot.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today