Personal Wealth Management / Market Analysis

Growth, Value and Valuations

Fears swirl over rising price-to-earnings ratios-but these are typical of a maturing bull market in which growth stocks lead.

Everyone likes a deal-and no one likes to waste money on too-pricey products or services. So it isn't surprising above-average US valuations and recent headlines about "overvalued" and "expensive" stocks have many wondering if today's buyers are getting snookered into a bad deal. In our view, this fear is rooted in a value approach to investing-one that says "cheap stocks" are inherently superior to pricier, "growth" stocks. But this overlooks the fact neither style leads forever-both have periods of outperformance. Higher valuations today are largely a function of growth stocks' benign emergence-and it wouldn't surprise us if they keep outperforming as the bull market continues.

Distinguishing between value and growth stocks can be tricky, and there are no hard-and-fast rules. That said, value stocks tend to sport lower valuations and pay dividends, with broad economic growth heavily influencing their profits and revenues. Folks using a value approach aim to identify companies investors are wrongly punishing, as reflected by low price-to-earnings ratios. They might believe markets are blowing company-specific problems out of proportion. Or they may be incorrectly downplaying the prospects for economic growth ahead. Growth stocks, conversely, tend to have higher valuations; are less likely to pay dividends; rely more on innovation; and are growing much faster than the overall economy. Growth-targeting investors care less about P/Es and more about expected earnings growth.

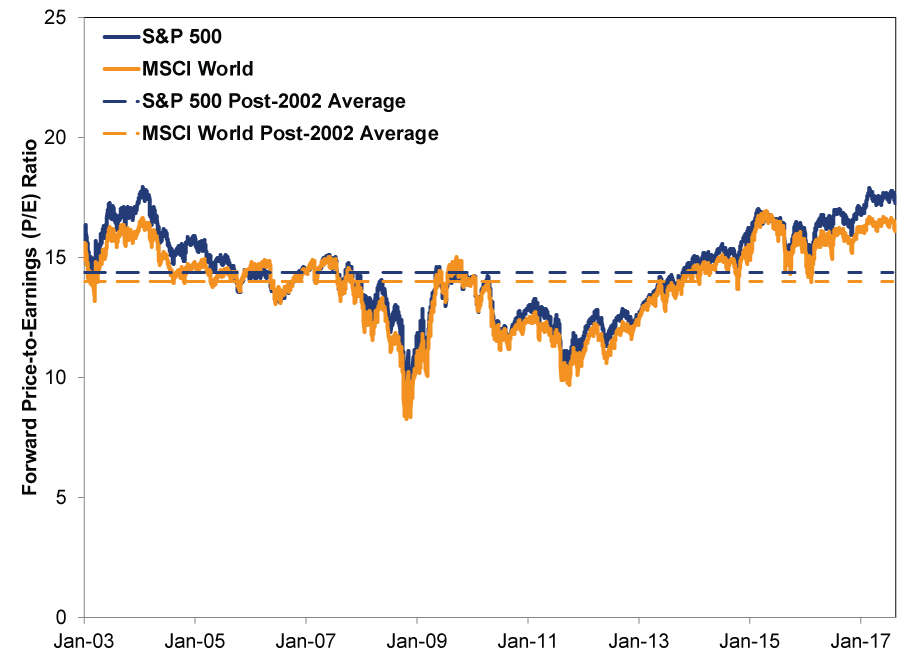

Growth and value cycle in and out of favor-like big and small, US and foreign and virtually every other category theme we can think of. Nonetheless, low-valuation fans are everywhere, and many don't like what they see today. Both US and global price-to-earnings ratios (presently 17.4 and 16.2, respectively)[i] are above-average and rising.

Exhibit 1: US and Global Stock Valuations

Source: FactSet, as of 8/28/2017. S&P 500 and MSCI World 12-month Forward P/E ratios, 1/1/2003 - 8/25/2017.

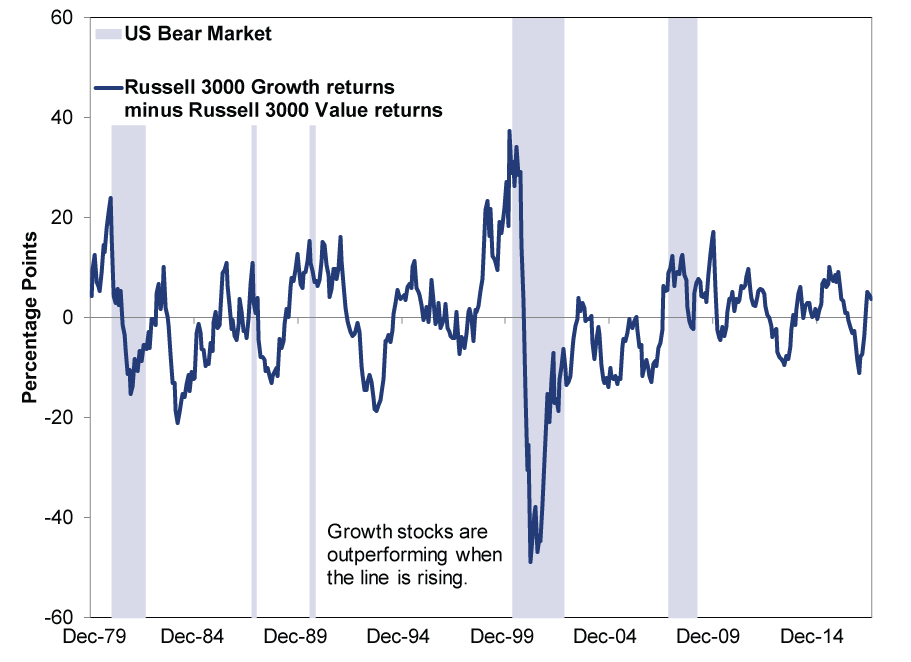

Growth stocks' outperformance doesn't explain current valuation levels entirely. Energy, for example, has the highest P/E ratio of any sector, largely due to low oil prices' wreaking havoc on profits. Nonetheless, most sectors other than Telecom have above-average P/Es today. This is typical of a growth-led period: When growth stocks-with their typically higher valuations-outperform, market valuations overall rise. Growth stocks' leading doesn't necessarily signal danger, either: As Exhibit 2 shows, growth can pace bull markets for years before they end.

Exhibit 2: USGrowth vs Value Historical Performance

Source: FactSet, as of 8/23/2017. Russell 3000 Growth Index rolling 12-month returns minus Russell 3000 Value Index rolling 12-month returns, December 1978 - July 2017. Bear market dates are based on S&P 500 price returns.

In this bull, growth started outperforming in mid-2013-not coincidentally, about when high P/E fears started kicking into gear. After slipping between July 2015 and December of last year, growth roared back, reinvigorating high-P/E fears.

While such worries are regular in bull markets, they are perhaps heightened this time because investors haven't seen persistent growth leadership since the 1990s! Glance again at Exhibit 2, and you'll see value led through most of the 2003 - 2007 bull market. Likewise, Exhibit 1 shows P/E ratios mostly fell. Why? Primarily because the bull ended in a wallop, long before P/E-boosting optimism-and growth stocks-got a chance to shine. Hence, for many of today's investors, stocks' persistent rise while valuations are above-average may seem unusual-weird and risky! But in reality, it is neither of those things. There are both fundamental and sentiment-based reasons for growth stocks to lead-and valuations to rise-in a bull's later stages.

For starters, business cycles affect value and growth companies differently. Value stocks' economic sensitivity means they tend to benefit disproportionately when the economy rebounds from recession and surprises pessimistic investors. Growth, meanwhile, tends to lead later in a bull, as increasingly optimistic investors favor high-quality companies with strong earnings potential. These stocks typically sport higher valuations, so P/Es rise: More confident investors are willing to pay up for the fast earnings growth they expect.

Eventually, sentiment will likely reach a point where investors believe they have a clear view of profit growth extending far into the future. This is characteristic of a bubble. As the Tech bubble inflated, for example, valuations surged as investors bid up dot-com stocks with allegedly sky-high earnings potential.

We aren't at the point in this bull market where folks project profits as far as the eye can see and disdain valuations. But sentiment is warming, and it seems to be lifting valuations and growth stocks with it. And sure enough-high-P/E companies with innovation-driven revenue streams have led the way recently. If this sounds like Tech, that's because many (though by no means all) Tech companies are growth stocks[ii]-an example of style/sector overlap. (Of course, growth isn't limited to Tech, but it is a fair example.)

Ultimately, we don't think investors should sweat growth's day in the sun. Its primacy today is typical of a maturing bull featuring sustained earnings growth and slowly warming sentiment-and in a world of broad-based growth and stellar earnings in both the US and Europe, it's rational for investors to pay more for future earnings-and bid up stocks.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10 -

Market Analysis Trim Your Angst on Economic Measurement Tweaks2026-07-09

-

Politics Long-Term Forecasts and Court Verdicts: The Latest in British and French Politics2026-07-09

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-07-08

2026-07-08

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today