Personal Wealth Management / Market Analysis

On Retail Sales Trends Outside the US

How is one widely followed spending measure faring overseas?

How are consumers faring after two years of elevated inflation? The conventional wisdom would say poorly, which is understandable—and we don’t dismiss those hardships and challenges. But as we showed last week, price pressures haven’t derailed American consumer spending. How about consumers overseas? A look at the retail sales measures outside the US isn’t clean, as many distortions from prices and calculation limitations muddy the water. But the data are overall mixed—a sign consumer activity looks more resilient than those fearing recession may appreciate.

First, note that many retail sales metrics aren’t inflation-adjusted. Those that are—volume measures—take into account price changes, but for those that aren’t, it is important to keep inflation trends in those nations front of mind, as we will show.

Starting with places that report sales volumes, April’s numbers brought some encouragement. In the UK, retail sales rose 0.5% m/m, rebounding from March’s -1.2% dip.[i] April’s read beat estimates and reflected some pent-up demand from March, when historically wet weather kept shoppers home. Hence, non-food stores sales volumes rose 1.0% m/m after March’s -1.8% fall.[ii]

Looking more broadly, there has been a well-publicized divergence between UK sales volumes and values since mid-2021—tied primarily to inflation. Total UK retail sales volumes are still 0.8% below February 2020’s pre-lockdown levels, while sales are 16.5% higher in value terms.[iii] But volumes have stabilized somewhat lately, rising three of the past four months—a sign of resurgent spending despite stubbornly high inflation.[iv]

Canada also reports retail sales volumes, albeit, the latest numbers are from March. Though they fell -1.0% m/m, motor vehicle and parts dealers (-4.0% m/m) and gasoline stations (-1.3%) drove the decline.[v] Excluding auto and gasoline station sales, March sales inched up 0.3% m/m. We caution against reading much into one month, but nations reporting sales on a volume basis suggest demand for goods has persisted despite fast-rising prices over the past two years.

Elsewhere, sales values have been more growthy this year, but it can be harder to get a clean read on these figures—not just because of the lack of inflation adjustment, but because some nations don’t publish seasonally adjusted month-over-month numbers, just year-over-year. Where we do have month-over-month figures, sales hit a speedbump in April—albeit on the heels of some solid growth in recent months. For example, Japanese retail sales fell -1.2% m/m, the first such drop since November 2022, while South Korean sales (-2.3%) dipped on a monthly basis for the first time since January.[vi] In the Land Down Under, Australian retail sales were flat after rising the past three months, and the Australian Bureau of Statistics noted spending has plateaued over the past six months due to cost-of-living pressures—though we would note softer spending is still spending.[vii]

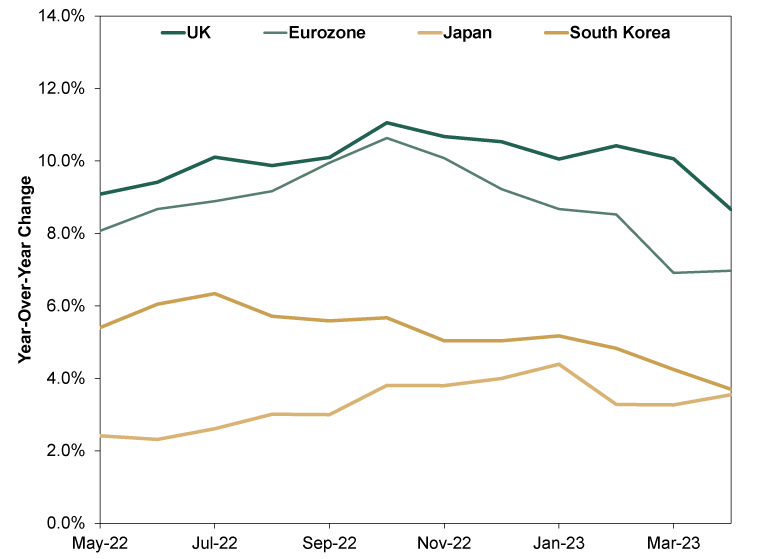

Now, we don’t have as clear a view of how demand is holding up since we can’t deflate retail sales by CPI, but it is worth noting Asia hasn’t faced the same price pressures as the West. Japan and South Korea in particular have had much lower inflation rates than those in Western Europe, so households in the East haven’t necessarily faced the same inflation-driven challenges. (Exhibit 1)

Exhibit 1: Select CPIs in Developed Asia and Western Europe

Source: FactSet, as of 6/1/2023. UK CPI, Eurozone HICP, Japan CPI and South Korea CPI, year-over-year change, May 2022 – April 2023.

China is a unique case since it reports its economic data on a year-over-year basis—common practice among many Emerging Markets. Year-over-year comparisons can introduce big skew due to the base effect, and that played a role in April’s retail sales, which rose 18.4% y/y—a reflection of April 2022’s cratering sales due to Shanghai’s COVID lockdowns.[viii] Still, even with that favorable comparison point, sales missed expectations of 22.0% y/y, and that that disappointment fueled concerns of a slowing Chinese economic recovery, especially after March sales surged 10.6% y/y from Jan-Feb’s 3.5%.

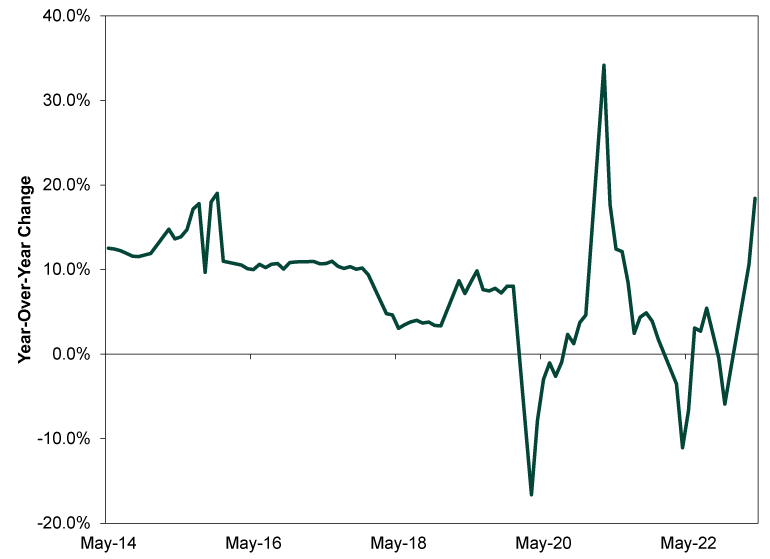

But those concerns seem overstated to us. As we pointed out this week, recent Chinese economic data appear to be following a well-known script following easing COVID restrictions: a short boom due to release of pent-up demand, followed by a return to the longer-term trend. That boom also tends to get smaller in each subsequent lockdown/reopening cycle. In our view, it is more likely retail sales growth slows than surges—consistent with China’s longer-term economic trajectory. (Exhibit 2)

Exhibit 2: Some Longer-Term Context for Chinese Retail Sales

Source: FactSet, as of 6/1/2023. Chinese retail sales, year-over-year change, May 2014 – April 2023. January and February figures are omitted due to Lunar New Year skew.

Retail sales aren’t perfect indicators. They tilt towards goods and won’t give a comprehensive look at spending since so many economies are services-heavy, especially in the developed world and late-stage Emerging Markets in Asia. Even in China, services makes up majority of GDP now. Still, retail sales indicate consumer spending in most major economies is resilient. Despite some soft patches, there are plenty of ongoing (and overlooked) growthy spots, too.

[i] Source: Office for National Statistics, as of 6/1/2023.

[ii] Ibid.

[iii] Ibid.

[iv] Ibid.

[v] Source: Statistics Canada, as of 6/1/2023.

[vi] Source: FactSet and Statistics Korea, as of 6/1/2023.

[vii] Source: Australia Bureau of Statistics, as of 6/1/2023.

[viii] Source: FactSet, as of 6/1/2023.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 8 - June 122026-06-15

-

Market Analysis A Market Perspective on Iran Truce Whisperings2026-06-15

-

Expert Commentary This Week in Review | IPOs, US Inflation, ECB Rate Hike

2026-06-12

2026-06-12 -

Market Volatility By the Numbers: 2026’s ‘Volatility’2026-06-12

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today