Personal Wealth Management / Behavioral Finance

What to Make of the Market’s Recent Mood Swings

Don’t let short-term sentiment swings sweep you off course.

After August’s brief bout of market negativity, many saw storm clouds gathering over stocks. Though stocks fell only 5.9%, doom and gloom headlines flooded the Internet for the following two months as pundits obsessed over Brexit, trade wars and global manufacturing’s malaise.[i] Sentiment slumped. Investors grew disproportionately dour, in my view, with many seemingly convinced recession was imminent and a bear market all but assured. Now? Not so much. Sentiment has flipped sunnier, highlighting the need for investors to stay even-keeled.

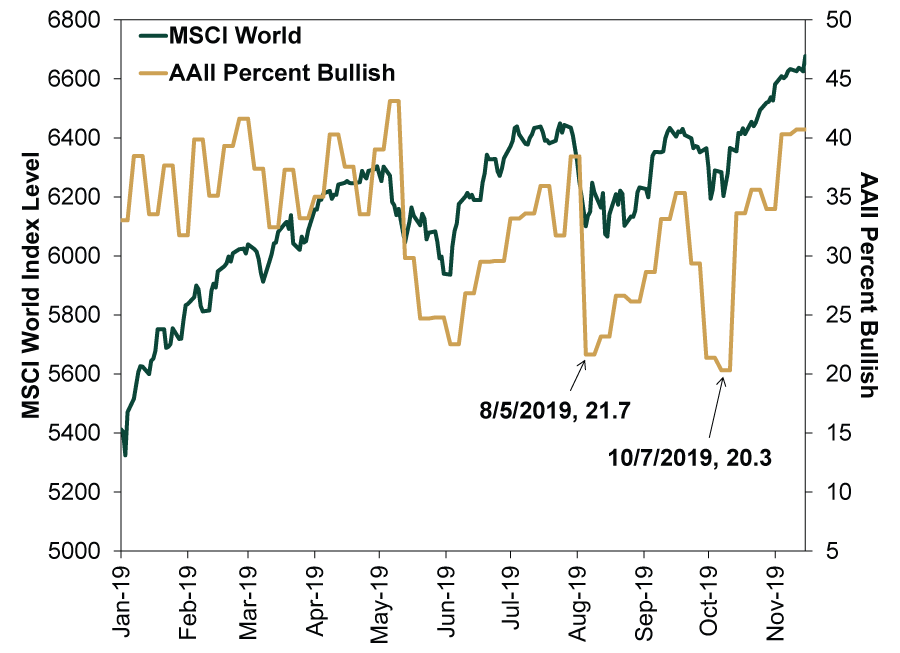

While market declines were relatively minor in late July and early August—with a wiggle again to start October—investors acted as though the dips were just the tip of a very scary iceberg. In August alone, they pulled a net $40.7 billion from mutual and exchange-traded equity funds.[ii] Only 21.7% of investors were bullish in the week ending August 9, according to an American Association of Individual Investors (AAII) survey.[iii] That figure declined further after early October’s swings. (Exhibit 1) For some perspective, only 9 readings in the last 20 years were lower than October 7’s 20.3.

Exhibit 1: Small Stock Market Swings Suppress Sentiment

Source: FactSet, as of 11/18/2019. AAII percent bullish and MSCI World Index with net dividends, 12/31/2018 – 11/15/2019.

Overseas, a gauge of German investor sentiment—ZEW’s tally of expectations for the DAX Index—sank to the lowest point in its 28-year history in August.[iv] Yes, even lower than any point during 2008 – 2009’s global financial crisis. Professional investors saw trouble ahead, too. In September, the percentage of global fund managers expecting a recession in the coming year was higher than at any point since 2009, a Bank of America poll found.[v] 10-year US Treasury yields plunged to 1.47%, with headlines shrieking about investors seeking “safe havens” wherever they could.[vi]

Those who feared negative sentiment would lead to a big market decline had it backwards, though. They made a common error, in my view: letting recent market movement impact their expectations. Recent conditions affect folks’ outlooks, often skewing them to extremes. But rather than kicking off a self-fulfilling prophecy—declines triggering weak sentiment triggering more declines—sour sentiment typically sets the stage for the positive surprises that lift stocks.

Now, one month later, a switch has flipped. Markets have rebounded, making new highs, and several gauges show equity investors—while not euphoric—are markedly more positive. One example: Bank of America’s fund manager survey for November registered the biggest jump in economic growth expectations in its 25-year history.[vii] Respondents on average decreased their net cash allocations by 20% compared to October, also shifting money out of bonds while upping equity allocations. More than 40% of AAII survey respondents, meanwhile, were bullish in each of the first two weeks of November—slightly above the 38% average since the survey’s 1987 inception.[viii] Headlines reflected growing optimism over better-than-expected economic data, US-China trade talk progress and the un-inversion of the US yield curve.

But the facts on the ground haven’t changed much. Data still show tepid economic growth. A US/China trade deal hasn’t been inked. A tiny yield curve inversion, likely too insignificant to impact lending and growth, is now a tiny yield curve “un-inversion”—no game-changer. So why has sentiment shifted so drastically?

In my view, it is because humans are a stew of emotions. People often overreact—concerns start to look like crises even though the facts don’t merit the dread. Studies show people fear losses about twice as much as they welcome gains, so many overreact to short-term trouble—behavioral finance terms this “myopic loss aversion.”[ix] That humanity now carries devices offering instant access to all the world’s negative headlines, all day long, only makes short-term overreaction more common. Worried about Brexit? A few clicks and you’ll find scores of articles lamenting Brexit’s disastrous consequences. Scared about the national debt? Click, and dozens of pundits from Los Angeles to London confirm your worst fears. What is Trump tweeting about China and tariffs now?!?

You get my drift. All this makes it easy to dump stocks when the facts don’t merit selling. A core challenge for investors is thus trying to remain even-keeled when headlines offer scads of reasons to panic. Those left behind after sentiment shifted this fall illustrate the perils of heeding the hype.

You don’t have to look back too far for more examples. Take the 2012 correction. World stocks fell -12.5% from April 2 – June 4 as investors fretted over eurozone debt and slowing Chinese growth.[x] But the EU debt fears were old news. China had been slowing for years. Those who sold into a falling market as worries spiked missed out: By early September, global stocks had topped pre-correction levels, and they kept moving higher. Similarly, in late 2018, hordes of investors ditched stocks amid fears that included stalling US-China trade talks, slowing global growth and rising interest rates. World stocks tumbled -18.1%.[xi] But none of those risks were new—and all lacked the power to wallop the economy. The global market bottomed on Christmas, and those who sold during the swoon were soon kicking themselves—global stocks have jumped 30.2% since then.[xii]

When you fear something prominently featured in headlines, negative scenarios are likely already baked into stock prices. That saps their power to sway markets’ future direction, teeing up market-boosting positive surprises. In my experience, that is a difficult lesson for many investors to learn. But it is critical. The time to get bearish is usually when few are worried and expectations are sky high, making stocks vulnerable to negative shocks. That is why Warren Buffett famously says to be greedy when others are fearful and fearful when others are greedy. This mindset requires emotional fortitude, and it can be uncomfortable. But in my view, history has proven its value.

[i] Source: FactSet, as of 11/27/2019. MSCI World Index return with net dividends, 7/24/2019 – 8/15/2019.

[ii] Source: FactSet, as of 11/18/2019. Sum total of Investment Company Institute weekly net flows into equity mutual fund and exchange-traded funds in August 2019.

[iii] FactSet, as of 11/27/2019. American Association of Individual Investors Sentiment Survey. “Bullish” indicates an investor expects stocks to rise over the coming six months. “Bearish” indicates an investor expects stocks to fall over the same period.

[iv] Source: FactSet, as of 9/24/2019. ZEW balance of investors expecting the DAX stock market index to rise minus fall. Data begin in December 1991.

[v] “Global Fund Manager Survey,” Michael Hartnett et al, Bank of America Merrill Lynch, 9/17/2019.

[vi] Source: FactSet, as of 11/27/2019. 10-year Treasury bond yield (constant maturity) on 9/4/2019.

[vii] “Global Fund Manager Survey,” Michael Hartnett and Tommy Ricketts, Bank of America Merrill Lynch, 11/12/2019.

[viii] FactSet, as of 11/27/2019. American Association of Individual Investors Sentiment Survey, average percent bullish, 7/17/1987 – 11/22/2019.

[ix] “The Effect of Myopia and Loss Aversion on Risk Taking: An Experimental Test,” Richard H. Thaler et al, Quarterly Journal of Economics, May 1997.https://pdfs.semanticscholar.org/ac8c/07714e860c42319254d762e30063e79e4713.pdf

[x] Source: FactSet, as of 11/27/2019. MSCI World Index return with net dividends, 4/2/2012 – 6/4/2012.

[xi] Source: FactSet, as of 11/27/2019. MSCI World Index return with net dividends, 9/21/2018 – 12/25/2018.

[xii] Source: FactSet, as of 11/27/2019. MSCI World Index return with net dividends, 12/25/2018 – 11/26/2019.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today