Personal Wealth Management / Market Analysis

8.15 Bits of Bad News That Haven’t Broken Markets in 2016 (But Were Supposed to)

False fears don't scare stocks.

Don't worry, the authorities are aware of the problem. Photo by Olivia Harris/Getty Images.

Folks remain pretty glum about the current bull market, now more than seven years old and arguably history's least-loved. Headlines constantly spout warnings about the next big bad for markets, adding to the overall gloom. However, is the hype behind the fear real? Now that we are more than halfway into 2016, here are 8.15[i] stories that were supposed to derail stocks but didn't-a friendly reminder about markets' resiliency.

1. US Recession Worries

Remember when folks fretted a potential US recession earlier this year? A stock market correction welcomed investors into 2016, and some pundits argued the US' ongoing "manufacturing recession" and heavy industry's struggles signaled broader troubles. Couple all this with an "anemic" Q4 2015 GDP advance estimate, and the numbers seemed foreboding. The initially reported 0.5% Q1 growth seemingly confirmed the fears. However, data in large segments of the economy-like services and consumption-were fine. Q1 GDP was revised up to 1.1% annualized, and most indicators strengthened in Q2. Not only have service sectors kept trending higher, but industry and manufacturing have staged a comeback in recent months. More telling about the future, The Conference Board's Leading Economic Index (LEI) has continued climbing. Despite the occasional down month, no US recession has started when LEI is high and rising like it is today.

2. Misplaced Eurozone Financials Fears

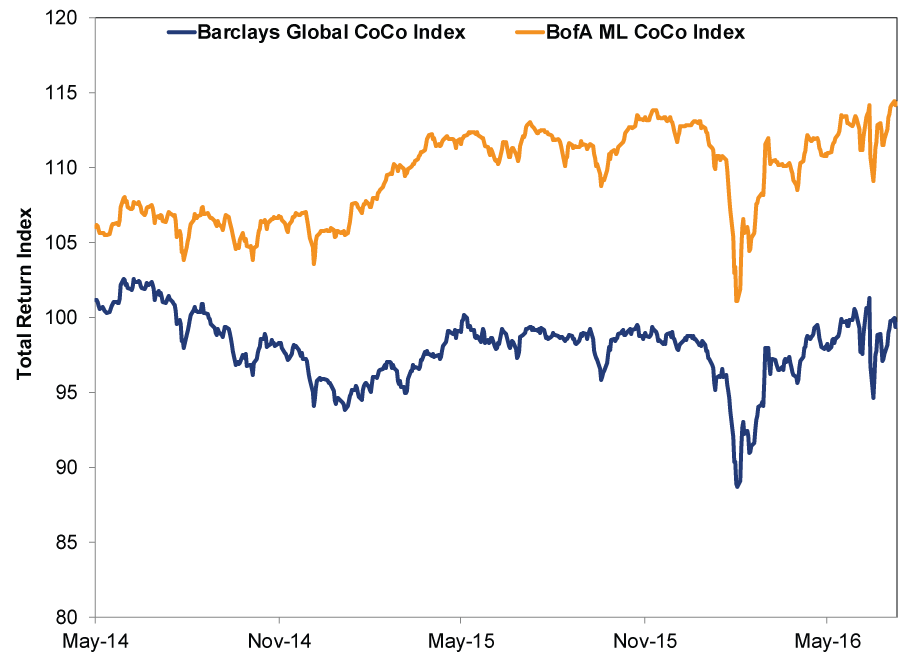

Early in the year, some worried eurozone banks were facing their own "Lehman Brothers moment." Due to a confluence of loosely related issues, from worries about bank earnings and future loan losses to the implementation of new regulatory rules surrounding bank "bail-in" proceedings, investors repriced eurozone bank bonds to account for the added risk. One notable German bank bore the brunt, and concerns about its earnings spurred comparisons to the US financial sector in 2008. However, there is a huge difference between the situation in Europe and the US eight years ago. The primary concern facing European banks: return on equity, i.e., worries about long-term profitability. In 2008, folks freaked out because financial institutions were illiquid and couldn't return creditors' money, full stop. We aren't saying European banks have an entirely clean bill of health (ciao, Italy !), but they are doing better than most appreciate-and they certainly aren't about to fall off a cliff, a la 2008. The lingering issues are longstanding and widely known-heck, even regulators are aware. Moreover, for all the handwringing about their sharp drop in February, eurozone banks' contingent-convertibles (coco bonds) have since climbed back. (Exhibit 1)

Exhibit 1: CoCos Have Not Gone Cuckoo

Source: FactSet, as of 7/21/2016.

3. Repeat of China's Hard-Landing Fears

China had a week to forget to begin 2016. Newly implemented circuit breakers-installed to curb domestic stock markets' sharp volatility-only exacerbated big downswings. Similarly, the PBoC set the yuan's reference rate lower the same week, prompting theories that China was devaluing its currency to goose growth. These concerns ultimately return to a common trope: China's long-awaited economic "hard landing." These murmurings aren't new, and more importantly, they haven't come true. Despite the oft-predicted plunges, Chinese GDP grew 6.7% y/y in Q1 and Q2 2016-right in the middle of its 6.5% - 7.0% target range for the year. No question Chinese growth has slowed over recent years, but a deceleration isn't a sudden stop. Moreover, the global economy continues benefiting from China's still-sizable contributions to growth. Oh, and not that it is a great indicator of China's economy, but those volatile domestic markets have calmed.

4. Negativity Surrounding Negative Rates

The ECB and BoJ grabbed attention with negative interest rates, fueling speculation about central banks' stimulating powers-and fears they were going too far. The theory: By charging banks to hold excess reserves, central bankers can spur lending. Realistically, though, banks don't have to lend-they can also move excess cash to another asset (e.g., US Treasurys) or pass the cost to customers. While negative rates aren't the positive central banks portray them to be, they aren't a huge problem, either. The ECB has had negative interest rates since 2014, yet the eurozone has grown, predating the ECB's negative rate policy and through it. Loan growth and demand have picked up, too-a sign incremental negatives won't reverse broader cyclical drivers. Negative yields on longer-term securities in Europe and Japan make news-and cause angst among the punditry-but they're a function of supply (limited) and demand (very high), not a reason to worry. Plus, thanks to such frequent discussion, their surprise power is waning. The world is getting more familiar with negative rates and the lack of trouble they cause.

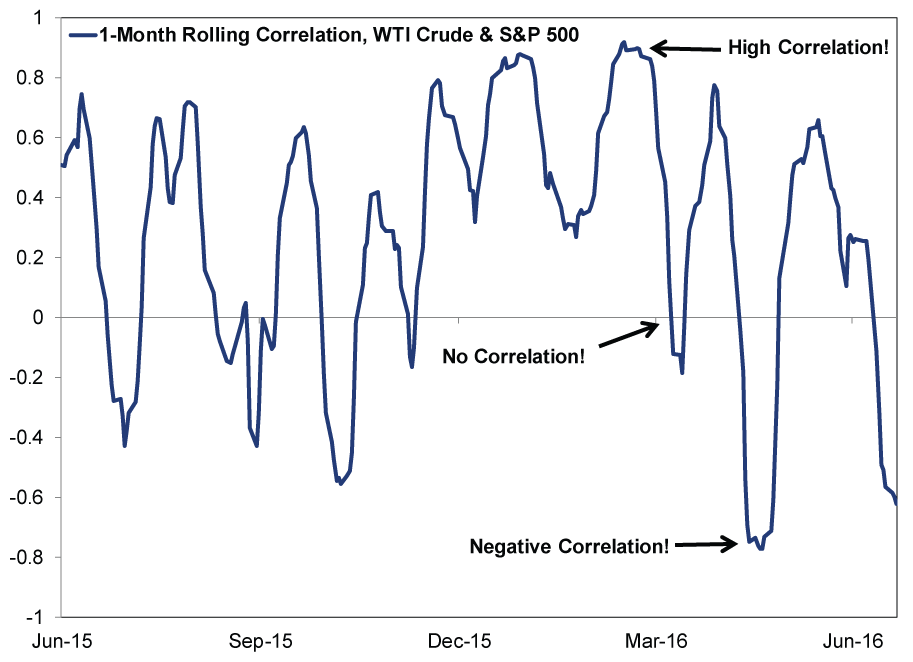

5. No Oil Slippage

Many pondered whether low oil prices would cause trouble for the global economy this year. Early in the year, the S&P 500 price movement was strongly correlated with oil, causing some to argue the two were now connected in some way. However, this was short-term happenstance, not the start of a new trend-oil markets aren't predictive for stocks. (Exhibit 2)

Exhibit 2: Oil and Stocks' Coincidental Price Movement

Source: Global Financial Data, as of 7/21/2016. Rolling 1-month correlation between S&P 500 Price Index and West Texas Intermediate Oil, from 6/30/2015 - 7/20/2016.

Certainly, oil prices' plunge over the past two years has hurt specific sectors (e.g., Energy) and commodity-dependent economies (e.g., Brazil and Russia). But for diversified nations, cheaper oil is neither hugely beneficial nor particularly harmful. It favors some, hurts others, and in services-oriented economies like the US, the winners outnumber the losers.

6. That Earnings "Recession"

S&P 500 profits have fallen for five straight quarters, prompting cries of an earnings recession and US private sector weakness. Yet the weakness is largely relegated to one sector: Energy, where plunging commodity prices (especially oil) have wrecked earnings. Excluding Energy, the picture is clearer: Corporate America is doing fine. Moreover, the final earnings numbers have consistently beaten expectations set at the quarter's start-the experts have constantly undershot reality. Analysts forecast a return to earnings growth (including Energy) later this year, and with year-over-year benchmarks soon becoming easier to meet as early 2015's higher Energy earnings fall out of the calculation, folks may finally see better-than-appreciated broad-based growth across most sectors.

7. The Premature Perils of the Presidential Primaries

As the US entered a presidential election year, the Democratic and Republican primaries were bombastic, causing folks to tremble at the thought of various candidates. With a field as large as 17, the Republicans "whittled" down the number of candidates to 11 before the Iowa Caucus. After a contentious primary season, Donald Trump emerged as the GOP's presumptive nominee. The Democrats didn't pull together a couple basketball teams' worth of candidates, but a spirited contest between Hillary Clinton and Bernie Sanders saw a fair amount of political burns[ii] too-though Clinton's lead was never in serious doubt. While headlines fretted the possibilities of a self-proclaimed socialist or a hotly contested GOP convention, neither was a serious risk for markets. With the candidates now known, markets will now start digesting the possibility of either a Trump or Clinton presidency. The closer we get to Election Day, the more uncertainty falls-a positive for markets.

8. Brexit Didn't Break Anything

After several months of similarly explosive rhetoric, the Brexit referendum resulted in a surprising win for Leave. Markets reacted negatively at first-after seemingly pricing in a "Remain" victory before the vote-and the volatility prompted concerns about Brexit's global impact. After a couple of down days, however, markets largely recovered. Now, despite the big political changes Brexit has wrought (e.g., a new prime minister), the actual economic impact is limited and should be for a while. Until exit negotiations conclude, Britain will remain in the EU. Not only does the government appear likely to wait on triggering the Lisbon Treaty's Article 50 to start negotiations, the process itself will likely last for at least two years afterwards. We don't know Brexit's economic consequences yet, but these talks will take a while to develop-sapping surprise power. More importantly, any sort of Brexit-related doom looks overwrought for the time being, and markets' move higher reflects that.

8.15. Foreign Monsters Have Invaded Our Shores

But it's OK. They're actually getting people outside and socializing. Just think twice about falling for related investment fads-buying on hype rarely ends well. We figure this latest one will Pokémon Go away soon.

[i] Our managing editor initially argued we should do 16 stories (for 2016, get it?), and while certainly doable, the writer of this article argued it wouldn't be accurate given we are only a little more than halfway into 2016 itself. To reward the writer's astute observation, the managing editor decreed 8.15 reasons be provided. And the writer said it shall be so.

[ii] Sorry.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 9 - March 132026-03-16

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today