Personal Wealth Management / Market Analysis

Are Credit Markets Sending a Distress Signal?

Trouble at a few junk bond funds renewed long-running bond market liquidity and contagion fears, but there are some mitigating factors.

This iceberg is not a visual metaphor for the bond market. Photo by Joe Raedle/Getty Images.

High-yield bonds have had it rough lately, as a handful of fund closures sparked fears of a run on junk bonds and wider economic contagion. ETFs tracking Barclays' and Bank of America Merrill Lynch's broad high-yield bond indexes hit their lowest level since 2009, and several pundits warn more carnage is in store, with widely feared liquidity issues making things even worse. Some draw parallels with subprime mortgages in early 2007, warning junk bonds are a canary in a coal mine. But this isn't a time to flee markets. It is a time to pause and assess the facts. Yes, junk bonds have had a tough time. But the funds that closed had some unique issues, and while markets might gyrate over perceived liquidity issues in the short term, fundamentally, there is little reason for spillover. There is also no transmission mechanism to stocks or the broader economy. This is a time to take a deep breath and sit tight.

For those who haven't followed the ins and outs, our story begins on Thursday, when Third Avenue announced it would halt redemptions on its Focused Credit Fund (TFCIX), liquidate the fund slowly over the next several months, and eventually distribute the proceeds to its investors. The closure, combined with the redemption gate, drove worries that the mismatch between daily liquidity for the funds, but thinly traded underlying holdings-bond funds' "liquidity illusion"-was finally being shattered, risking a vicious cycle of fund redemptions and liquidations. Big drops and high-trading volume in junk bond ETFs seemed to underscore this, as did Stone Lion Capital Partners' decision to halt redemptions from a high-yield bond hedge fund Friday. Lucidus Capital Partners fanned the flames Monday, announcing it "liquidated its entire portfolio" and will close.

The flight from ETFs looks like a classic sentiment-driven overreaction. When emotions run high, and the fight-or-flight response takes over, it's natural for many to move first and ask questions later. If a fund's decision to halt redemptions smells faintly of market-wide liquidity issues, then the "flight" instinct will drive folks to flee bond funds now, lest they get trapped when the gates come down. It might not be a rational response based on the facts, but emotion and logic rarely intersect. This is the story of most market corrections.

But let's look at the facts. Lucidus has actually been winding down since October, when a "significant" investor sent a redemption notice. Co-founder, co-CEO and co-CIO Darryl Green co-resigned shortly thereafter. That they announced the move now is coincidental. Since Stone Lion was a hedge fund, details on its holdings aren't available. But The Wall Street Journal reports the fund faced "heavy losses on so-called distressed investments including junk bonds, post reorganization equities and other special situations." TFCIX also focused on distressed debt , which is the junkiest of junk. Nearly half its assets were in bonds rated below B, and another 40% were in non-rated firms. Broader high-yield ETFs, by comparison, have about 50% in BB-rated firms and only 9% below B. Of TFCIX's top 25 holdings, about half entered bankruptcy or restructured debt within the past two years. It isn't as though a slew of new victims of falling commodity prices brought down TFCIX. They are old victims like Energy Future Holdings, which filed Chapter 11 in April 2014. Heck, one of those holdings is a claim on Lehman Brothers' assets, which says pretty much all you need to know.

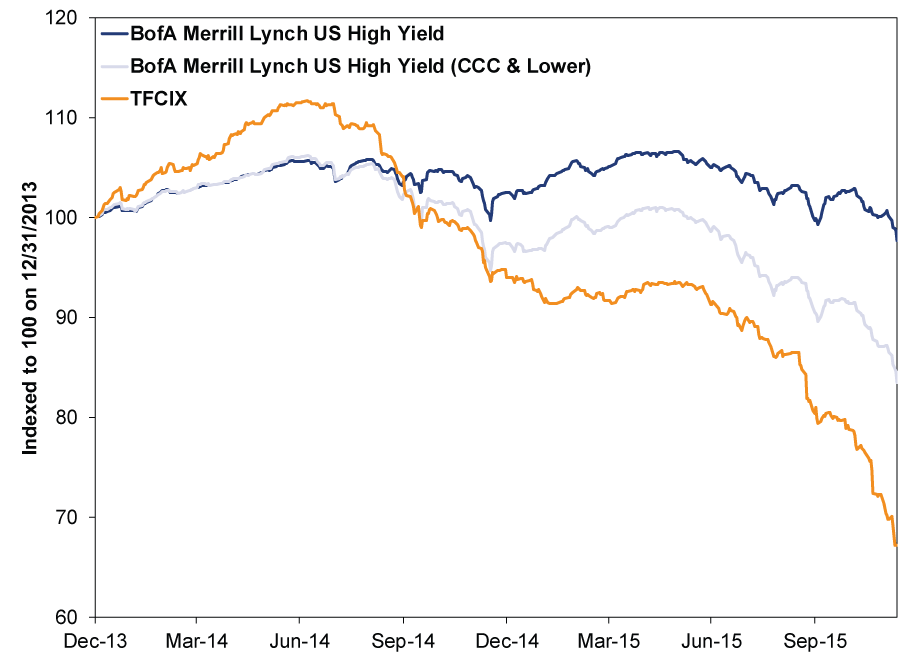

TFCIX's holdings weren't liquid, but this isn't a tale of bond market liquidity gone wrong. It is a tale of investors fleeing an extremely poorly performing fund after over a year of problems. Exhibit 1 plots its performance, along with broad and extra-junky high-yield benchmarks, since 2014 began. This year alone, TFCIX fell -28.4%, about twice as bad as the CCC-or-lower high-yield index. The broadest benchmark is down just -4.7%. Poorly performing mutual funds close shop all the time.

Exhibit 1: Ouch

Source: FactSet, as of 12/14/2015. Third Avenue Focused Credit Fund, BofA Merrill Lynch US High Yield and BofA Merrill Lynch US High Yield (CCC & Lower) total returns, 12/31/2013 - 12/11/2015. Indexed to 100 on 12/31/2013.

Still, some speculate it's worse now because Dodd-Frank prevents banks from stepping in to provide liquidity. That might sound plausible on the surface, but there is a catch: Even before 2008, dealers didn't serve as buyers of last resort en masse. Distressed bonds have always been illiquid, and before 2008, matching up buyers and sellers wasn't easy even in happy times for bonds. Junk bonds were also quite prone to sharp swings before Dodd-Frank, particularly during a crisis. At times like that, banks hunker down and shun risk. They don't pile it on altruistically to provide liquidity. Steely-nerved value investors are the ones who buy when there is blood in the streets, not banks.

As for broader economic contagion fears, we wrote last week that high-yield bonds aren't a leading indicator for stocks. That's all still true. All markets have equal access to information, and as often as both categories trade, it is impossible for one to have priced in something the other missed. Markets just don't work like that. Stocks haven't missed anything that happened in the high-yield bond world. Few of TFCIX's top 25 holdings had publicly traded shares, but of those that did, most took a severe beating this year. Some were penny stocks. Stock and bond markets alike were well aware of their innate problems. Energy and Materials stocks are also well aware of commodity-oriented firms' debt woes and have taken it on the chin this year. If high-yield bond troubles were to limit credit availability for larger, healthier firms, it would be an issue, but so far there is no evidence this is happening.

And there is another key difference between today and 2008: the absence of a transmission mechanism-a way for the losses to spiral beyond high-yield bonds and bond funds. Subprime mortgages, the punditry's favorite reference point, had a big transmission mechanism: FAS 157, the mark-to-market accounting rule, which required banks to write down all related assets whenever one of these funds sold at a firesale price. Even though banks had no intention of selling these securities, planning instead to hold till maturity and collect income along the way. That caused a couple hundred billion in actual loan losses to spiral into about $2 trillion in needlessly destroyed bank capital. High-yield bonds have no such transmission mechanism. As has been well documented, banks hold precious few of them. Funds with high concentrations will get burned, and we're seeing that play out now. But that's what you see after an asset gets hit. It isn't likely to trigger a crisis.

The wild ride could very well continue for a few more days or even weeks. Short-term swings are unpredictable, no matter the market. But to paraphrase Ben Graham: Markets are voting machines in the short term, but in the long term, they're weighing machines. The fundamental backdrop for Corporate America remains plenty healthy, with strong balance sheets, a growing economy and a steep yield curve. Over time, markets have plenty of positives to weigh.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Blunting Burnham?2026-07-21

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Expert Commentary 3 Things You Need to Know This Week | Q2 Earnings, ECB Meeting, Trump Accounts

2026-07-20

2026-07-20 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 13 - July 172026-07-20

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today