Personal Wealth Management / Market Analysis

Chart of the Day: When Real Estate Decided to Go Solo

How has Real Estate fared ever since it became the GICS' 11th sector?

One year ago, the smart people at MSCI and S&P who determine the Global Industry Classification Standard (GICS) declared Real Estate the 11th sector[i]-the first change to the prominent sector list since 2001. The GICS folks had pondered breaking Real Estate out of Financials since 2014, and with the growing popularity of Real Estate Investment Trusts (REITs) in recent years, it seemed like a logical decision. A month after its debut, however, Real Estate trailed both its former Financials home and the broader S&P 500 index. A year later? That lag is even more pronounced. In my view, this serves as a friendly reminder to tread cautiously when considering trendy or headline-making investment opportunities-it smacks of chasing heat, a dangerous investing approach.

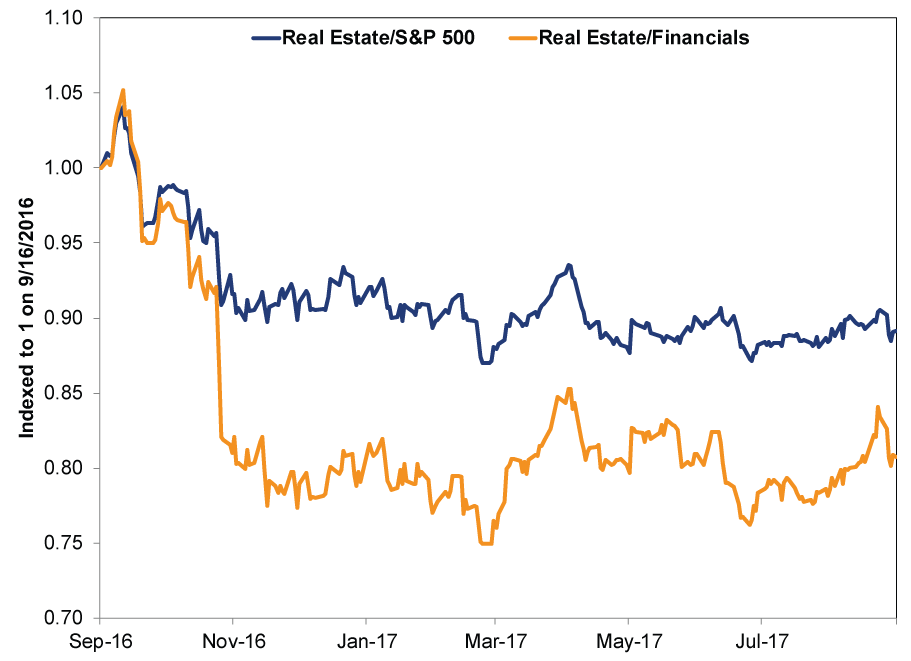

Here is a chart showing Real Estate's relative performance compared to Financials and the broader S&P 500. When the lines are rising, Real Estate is outperforming.

Exhibit 1: Real Estate's Relative Performance

Source: FactSet, as of 9/18/2017. S&P 500 Real Estate, S&P 500 Financials and S&P 500 total return indexes from 9/16/2017 - 9/15/2017. Indexed to 1 on 9/16/2016.

Granted, Real Estate hasn't been an absolute loser. Since September 16, 2016, Real Estate is up 7.8%, and year-to-date, it's up 10.0%.[ii] However, Financials is up 31.4% since last September (7.9% YTD), while the S&P 500 has risen 19.3% (and 13.3% YTD).[iii]

Buying something because it's popular isn't a sound investing thesis, in my view. Consider this just from a size perspective: Real Estate makes up about 3% of the S&P 500 market cap pie, which isn't a huge slice.[iv]Subsectors within the GICS' other 10 sectors are bigger! Banks (in Financials) have a 6.2% weighting in the S&P 500, while Software (in Information Technology) comprises about 5.1%.[v] However, Real Estate has gotten a lot of press over the past several years, particularly due to REITs, which were popular among investors seeking higher yields in a low interest rate environment. But loading up on Real Estate after its run-up smacks of heat-chasing: You can't buy past performance. Stocks are forward-looking, and investors should base investment decisions on where markets are likely headed in the next 12-18 months-not where they were 12-18 months ago.

Real Estate's relative performance also provides a timely lesson about the benefits of diversification. Investors shouldn't go hog wild over any one sector, but especially one as small as Real Estate. For the US-only S&P 500, Information Technology holds the biggest weighting at 23%.[vi] In the MSCI World Index, which spans developed markets globally, Financials leads at 17%.[vii] In both indexes, Real Estate is just about 3%, so if you're emphasizing Real Estate-related stocks, you're overweighting a tiny portion of the broader market-risky! Even if you expect Real Estate to outperform, don't forget one of investing's primary rules: No matter how sure you are, you could always be wrong.

While the history is limited, sector reclassifications tend to be reactions to recent strong returns. Before 1999, the S&P 500 had only four sectors: Industrials, Utilities, Transports and Financials. The desire to show Tech's hot returns led to the 10-sector GICS system-and it also took place right around when the Tech bubble burst in 2000. More recently, MSCI added Pakistan to its Emerging Markets index this past June, and it has lagged the broader index since then. A couple historical data points aren't all-telling, but they provide some evidence receiving recognition for great past returns doesn't automatically lead to continued outperformance.

[i]They took it to 11, as it were.

[ii] Source: FactSet, as of 9/18/2017. S&P 500 Real Estate Total Return Index, from 9/16/2016 - 9/15/2017.

[iii] Source: FactSet, as of 9/18/2017. S&P 500 Financials Total Return Index and S&P 500 Total Return Index, from 9/16/2016 - 9/15/2017.

[iv] Source: FactSet, as of 9/15/2017.

[v] Ibid.

[vi] Ibid.

[vii] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Market Volatility, Energy Markets, US Inflation

2026-03-13

2026-03-13 -

Market Analysis Due Diligence and the DOL’s DOA Fiduciary Rule2026-03-13

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today