Personal Wealth Management / Market Analysis

China Hits the Target

Chinese GDP growth matched the official target in Q2, but some fear struggling mainland stocks will soon take an economic toll.

Chinese GDP officially grew 7.0% y/y in Q2, matching Q1's pace and the government's target and beating expectations for 6.9%. But the good news hasn't quieted those long-running "hard landing" fears. They just morphed again, this time into jitters over how mainland stocks' crash will impact China's economy from here on. Wild Chinese markets or no, we wouldn't be surprised if China's economy continued its modest slowdown for the foreseeable future, but a hard landing still appears highly unlikely-we think investors can still expect China to contribute meaningfully to global growth.

China skeptics claim the trouble in A-shares (which we discussed here) could hurt economic activity on two fronts: financial services and consumer spending. The consumer spending fears center on the supposed "wealth effect"-the belief rising stock markets make folks feel wealthier, driving spending higher, while falling markets make folks feel less rich and thus inspire them to tighten the purse strings. The financial services angle is a little more straightforward: Trading volumes jumped during the mania, boosting financial firms' growth, and falling back to more normal trading volumes could drive a setback in the industry, hurting China's service sector-the sector officials are counting on to offset the continued slowdown in heavy industry. There is probably a kernel of truth here, though the impact likely isn't as great as feared. The consumer spending angle, however, doesn't wash.

Industry-level data for China's Q2 GDP aren't yet available, but analysts crunched the numbers for Q1 and found financial services contributed 1.3 percentage points to China's 7.0% headline growth rate, way up from its 0.7 percentage-point contribution in all of 2014 (when China grew 7.4%). Considering service sector growth accelerated sharply from 7.9% y/y in Q1 to 8.4% in Q2-and millions of investors reportedly opened brokerage accounts in the quarter-many suspect financial services drove the acceleration. Fair enough, and probably fair to assume things ease off a bit when the frenzy dies down (as we write, many companies' shares remain halted, so activity is slowing). But the broader impact seems limited. As of 2014's end, the financial industry comprised just 5.3% of Chinese GDP-about even with real estate, and smaller than retail/wholesale trade and (by a mile) heavy industry. Property sales have picked up lately, and a continued rebound there could help offset any potential iffiness in finance.

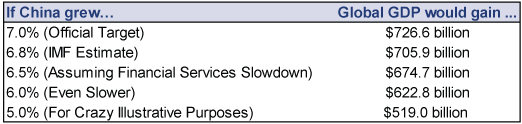

UBS economists estimate a financial services slowdown would shave just half a percentage point off China's second-half growth, knocking it from the first half's 7.0% to 6.5%. Take that with a grain of salt as you would all economic forecasts, but for illustrative purposes, that sort of slowdown wouldn't mean a heck of a lot for the global economy-even at that slower growth rate, China would add a lot of dollars to world GDP:

Exhibit 1: Hypothetical Chinese Growth in Dollars

Source: IMF, as of 7/15/2015. Calculations based on IMF's estimation of China's 2014 GDP at $10.38 trillion.

And even that table understates matters, as it applies real (after inflation) growth rates to nominal dollars. The IMF's estimate for nominal Chinese GDP growth in 2015 would add about $831.5 billion to world output. That's huge. Shave some off for financial services, and it would still be huge. Heck, even that $519 billion is big-it's like two and a half Greeces. Or, if you prefer, it's the equivalent of the US growing about 3%. Would anyone sneeze at 3% US GDP growth?

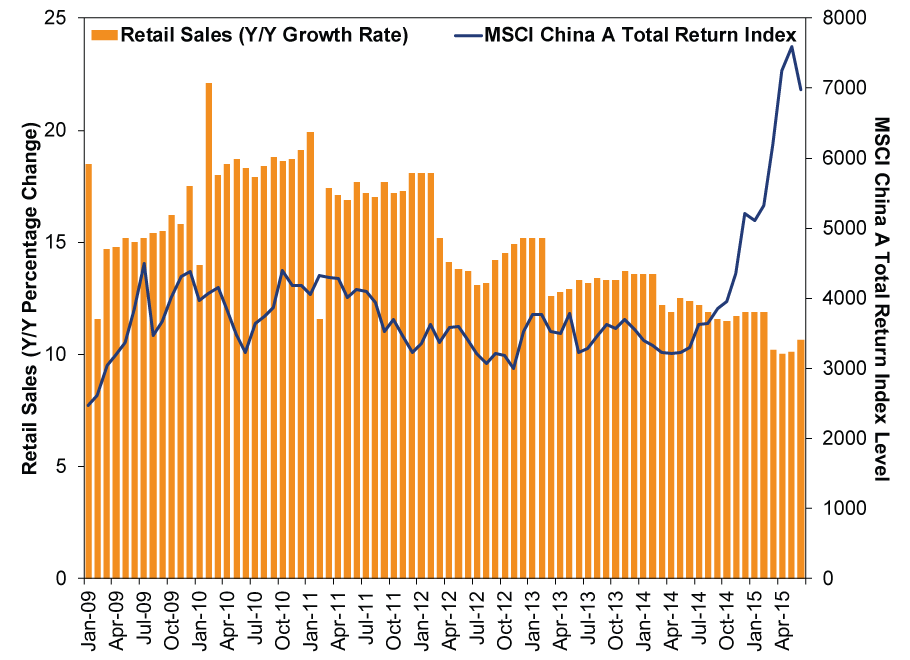

As for the consumer spending angle, stock markets don't drive consumption. Not in the US, not in China, not anywhere. Chinese retail sales maintained double-digit growth rates when local stocks tumbled in 2009, 2010 and 2011. Those growth rates slowed-natural, as growth compounded off an increasingly larger base-but they did not plummet. Nor did sales suddenly surge when mainland stocks began booming last year.

Exhibit 2: Chinese Retail Sales and Mainland Stocks

Source: FactSet, as of 7/15/2015. Y/Y Retail Sales growth and MSCI China A Index with net dividends, January 2009 - June 2015.

This is logical when you consider that only about 6% of Chinese citizens have brokerage accounts. Plus, rumors of investors using their brokerage accounts as ATMs-in the developed world or China-are greatly exaggerated. Yes, some retirees living off their portfolios do cut back when markets are down, to the extent they have discretionary expenses they can reduce temporarily. And yes, what some economists call "animal spirits" or "confidence" may impact spending on the margin (though measurements and theories around what drives those spirits aren't ironclad). But for the most part, disposable income growth drives consumer spending growth-if you earn more after taxes, you can spend more. Simple as that. China's government is uncannily good at ensuring their economy grows fast enough to keep disposable incomes rising at a decent clip. Year-to-date, national per-capita disposable income is up 9.0% y/y (7.6% y/y when adjusted for inflation), and urban residents' per-capita disposable income is up 8.1% y/y (6.7% y/y after inflation). That last figure about matches urban residents' full-year real per-capita disposable income growth of 6.8% in 2014. Steady income growth, not soaring stocks, is behind retail sales' continued 10%+ growth.

GDP calculation is never a perfect science, and some private-sector economists suspect growth was lower-and has been for some time. But whether growth is closer to 7% or the 5-ish % estimated by private-sector economists, China should continue growing fast enough to help propel the global economy forward.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today