Personal Wealth Management / Market Analysis

Cutting Through the BoJ's Monetary Confusion

Monetary policy observers are still trying to figure out whether the Bank of Japan just tightened.

Central bank watchers have been stuck in quite the conundrum since the Bank of Japan’s (BoJ) July 31 meeting—no one can seem to tell if the bank is “easing” or “tightening.” At first, easing seemed to be winning, since the bank kept all its asset purchasing (aka quantitative easing, or QE) targets unchanged. But as time passed, more observers seemed to realize the decision to let 10-year government bond (JGB) yields rise as high as 0.2% would probably mean fewer JGB purchases, which to most sounds like tightening. But when yields hit an 18-month high at 0.145% on August 2, the bank intervened with a “special buying operation,” driving yields back to 0.115% as one policymaker said they wouldn’t hesitate to stem a rapid rise. Which … sort of seems like easing? Meanwhile, JGB yields have kept on swinging. Overall, we think the saga is emblematic of why trying to divine central bankers’ next move is fruitless—sometimes they say one thing and do another. But we would also suggest investors not read too much into one or two days’ worth of special operations and instead take a longer view. The last time the BoJ widened the JGB trading band, it amounted to a “stealth tapering” of QE. Once all the fuss dies down, this latest tweak could very well do the same. If it did, we suspect it would be an incremental positive for Japan’s markets and economy.

To see why, it is important to understand how we got here. Japan’s QE program is the world’s largest relative to GDP. The BoJ targets purchasing ¥80 trillion (roughly $720 billion) in JGBs annually—nearly 15% of 2017 GDP![i] At its peak, US QE was only 6.1% of GDP.[ii] The BoJ has been so active, it owns nearly 40% of total outstanding JGBs.[iii] But despite this Godzilla-sized “stimulus,” Japan’s economic growth has been tepid. The BoJ began the current QE program near the end of 2010, yet average annual GDP growth from 2009 through 2017 was only 0.7%.[iv] Meanwhile, average annual US GDP growth was 1.7% over that period, without its much smaller “stimulus/QE” for the last three years.[v] This doesn’t shock us. While most believe QE supported the economy and markets—and fear its end—we have long argued QE is a drag. When the BoJ bought long-term bonds, it reduced long-term rates and flattened the yield curve. Banks borrow short-term to fund long-term loans, so a flattish yield curve—with just a teensy gap between short- and long-term interest rates—crimps banks' loan profits. This discourages banks from lending to all but the most creditworthy borrowers, starving most firms of capital and the economy of fuel. It also stifles broad money supply growth, working against the BoJ’s mandate to get inflation back up to 2%. This is why we have long believed Japan would benefit from ending QE as soon as possible.

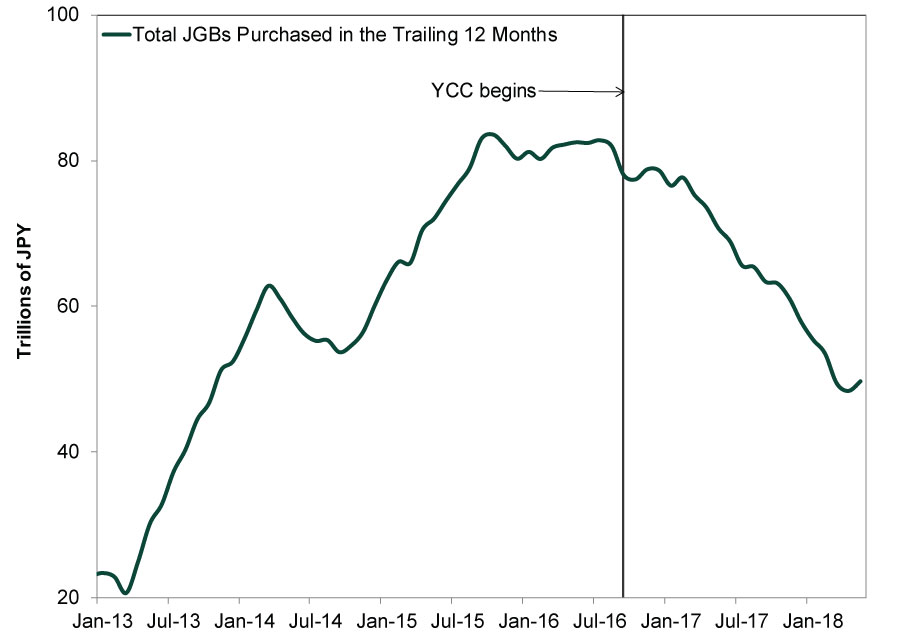

Japanese banks have long seemed frustrated with BoJ policy as well. Not only because they can scarcely make any money from lending, but because negative short-term interest rates further whacked their profits. The BoJ seemed to get the message in September 2016, when they introduced a program called Yield Curve Control (YCC), which targeted a 0% 10-year JGB yield but allowed fluctuation within a tight bandwidth, widely assumed to be +/-0.1%. At the time, long rates were negative, so targeting a 0% yield actually meant steepening the yield curve. It also meant the BoJ was buying fewer 10-year JGBs, allowing long rates to inch up. BoJ asset purchases fell to ¥50 trillion in the 12 months through May 2018, far below that ¥80 trillion full-year “target.”[vi] Tapering! But that sure isn’t what they called it, so they are tapering on the down-low.

Exhibit 1: Japan Started Tapering Nearly Two Years Ago

Source: BoJ, as of 8/7/2017. Total JGBs Purchased in the Trailing 12 Months, 1/31/2013 – 5/31/2018.

Notwithstanding the recent intervention, widening the 10-year JGB yield’s trading band to +/-0.2% could theoretically allow long rates to inch up a wee bit more, steepening the yield curve. Even before the BoJ’s announcement, yields were already creeping above 0.1%, inciting policymakers to intervene with unlimited purchase offers to drive them back down. This strikes us as a strong indication the market would like to take yields a bit higher. But whether they will be able to depends on how much the BoJ intervenes from here, which remains to be seen. We may see more operations like August 2’s JGB-buying frenzy, or they may allow a more gradual rise toward 0.2%. This, plus the BoJ’s decision to apply negative interest rates to a smaller swath of assets, might give banks a smidge more relief and enable them to lend a tad more. Only a baby-step, but a step nonetheless.

We half wonder if August 2’s intervention was more marketing spin than anything else. The BoJ has seemingly been trying to have it both ways for a while, giving the perception of maintaining QE while quietly tapering and creating an interest rate environment more likely to benefit the economy. Any hint of central banks tapering QE has spooked markets for years now (e.g., 2013’s taper tantrum), and that includes the prospect of tapering in Japan. The BoJ also appears to be wary of doing anything that would make the yen rise, as evidenced by policymakers’ quick clarification of BoJ Governer Haruhiko Kuroda’s comments to Japanese lawmakers that it might be reasonable for policymakers to start pondering QE’s end next year if inflation hit 2% then. A subsequent press release sought to ensure investors they weren’t actually planning to end QE then. Marrying the latest policy tweak with temporary intervention and dovish public comments could be another step toward keeping up appearances while gradually stepping away from QE.

Whatever happens, our views haven’t changed. We still think tapering and eventually ending QE would be a net benefit for Japan’s economy and markets, and if the latest policy tweak is a step toward that, it would be a positive. But only a small one, with Japan’s monetary policy only slightly less abysmal than it was before this announcement—and only slightly less of a headwind against an economy plagued by weak domestic demand and in need of reform. But any progress would be worth noting, if for no other reason than it further disproves the notion QE and central banks drove this bull market.[i] Source: Ministry of Finance, as of 8/3/2018. 2017 nominal GDP. Also, we included the word “targets” here very intentionally as it no longer actually buys that amount, which is sort of why we’re writing this article.

[ii] Source: Federal Reserve and US Bureau of Economic Analysis, as of 8/8/2018.

[iii] Source: BoJ and Japanese Ministry of Finance, as of 8/2/2018. Percentage of outstanding JGBs owned by the BoJ, 3/31/2018.

[iv] Source: Japanese Ministry of Finance, as of 8/13/2018. Average annual real GDP growth, 2009 – 2017.

[v] Source: Bureau of Economic Analysis, as of 8/13/2018. Average annual real GDP growth, 2009 – 2017.

[vi] Source: BoJ, as of 7/31/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis On the June Inflation Cooldown2026-07-14

-

Expert Commentary 3 Things You Need to Know This Week | US Inflation, China GDP, US Retail Sales

2026-07-13

2026-07-13 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—July 6 - July 102026-07-13

-

Expert Commentary This Week in Review | Global PMIs, SpaceX, RMD Planning

2026-07-10

2026-07-10

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today