Personal Wealth Management / Economics

Eurogrowthy

Eurozone growth defies the skeptics. Again.

Eurozone GDP grew 1.4% annualized in Q4-its seventh straight quarter of growth and beating expectations-and the way many headlines tell it, you'd think this is just terrible news. Growth "masks a broken eurozone" where wages are sputtering and living standards falling. The acceleration is powered by Germany, which is leaving France behind, "creating a worrying two-speed tension at the heart of the eurozone" and a "lopsided" recovery that "raises political stakes." Who cares about the rest when Italy is a "ticking time bomb." Looks like eurozone sentiment is still way too dour. The region isn't in wonderful shape, but with folks this negative, it doesn't need to be-choppy growth should easily surprise the skeptics.

Yes, the eurozone is the slowest-growing major region. Yes, Germany led the charge while France slowed and Italy endured its 14th straight no-growth quarter. Yes, there are political differences as countries lobby for pro-growth measures. But that's all whatever the negative equivalent of window-dressing is. Global markets generally don't care whether some nations grow faster than others-the aggregate, and how that influences earnings globally, matters more. Nor do eurozone stocks much care whether France grows 0.1% q/q (non-annualized), as it did, or 0.7% like Germany. Stocks aren't linked one-to-one with GDP. Economic growth matters, but not in a vacuum. The gap between sentiment and reality is the kicker. And in France, where services and manufacturing purchasing indexes spent most of Q4 in contraction, even slight growth was a happy surprise.

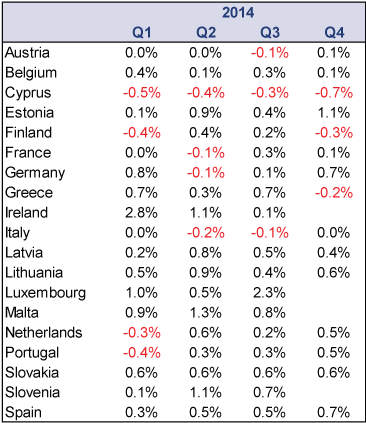

For all this talk of a broken Europe where only Germany is chugging, the country-specific breakdown looked pretty alright. As Exhibit 1 shows, of the 15 countries reporting so far, 11 grew. The three that contracted comprise about 4% of eurozone GDP. If the world could weather an 18-month eurozone contraction from Q4 2011 through Q1 2013, we daresay stocks can survive if only Greece, Cyprus and Finland shrink.

Exhibit 1: Eurozone GDP Growth by Country

Source: Eurostat, as of 2/13/2015. Quarterly GDP growth, non-annualized, 2014.

Most of the alleged drawbacks surrounding Q4 GDP are either sociological or backward-looking-not what forward-looking stocks typically care about. Some grouse over GDP remaining below its Q1 2008 peak, but this is simply trivia. It isn't unusual for an economy to take several quarters to move past recovery and into expansion. It took the US nine quarters after the 2007-2009 recession bottomed. The UK took 17. Stocks did fine in both nations, just as eurozone stocks are up during the slow recovery. As for the politicking, the region might benefit from more pro-growth measures, but the region has already proven capable of growing (and stocks rising) without fiscal stimulus. Ditto for reforms in France, Italy and elsewhere-long-term structural positives, if they happen, but cyclical positives can trump structural factors. And, yes, life is hard in nations like Spain and Greece, where unemployment is sky-high, but stocks have a long, long history of looking past issues like this. That sounds mean and callous, and we hate to sound mean and callous, but it is also a fact.

Looking ahead, we don't see much changing across the pond. Growth probably continues, based on rising Leading Economic Indexes in Spain, Germany, France and the full eurozone. It probably doesn't speed up a ton, if at all. And that's probably fine, because with everyone fearing a deflationary lost decade in a sputtering two-speed economy that can't achieve escape velocity (our paraphrasing of today's sentiment, not our opinion), uneven slow growth should beat expectations-and that's all stocks need.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today