Personal Wealth Management / Market Analysis

How to Lie With Statistics: Election-Year Stock Returns

In which we debunk three flawed "analyses" of election-year returns.

How will 2016's election impact stocks?

We've seen a wealth of speculation in recent weeks, much of it purportedly based on market history-and much of it wrong. Here are three of the biggest fallacies:

- Election-Year May Returns Are Usually Negative

- Election-year returns are bad in year four of a two-term president's second term

- In election-year May - Novembers, stocks do well when the incumbent party wins but badly when the opposition wins.

All exemplify what Darrel Huff called "lying with statistics" in his seminal 1954 book, whose title we borrowed for this article. Some use limited datasets with averages skewed by extreme outliers. Others cherry-pick broken indexes like the Dow or ignore dividends. It all amounts to misinformation, and none of it is actionable for investors.

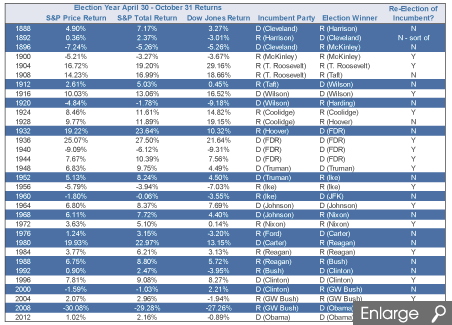

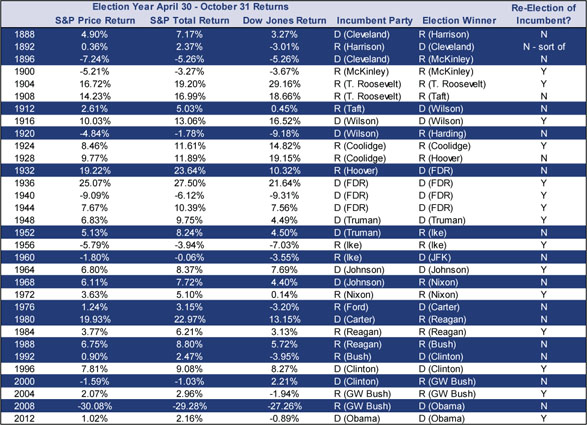

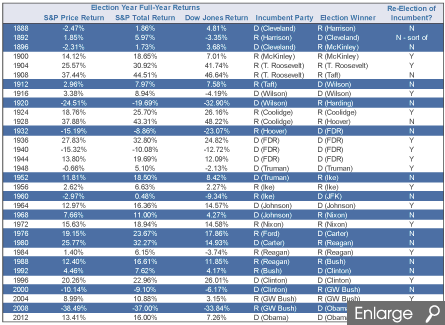

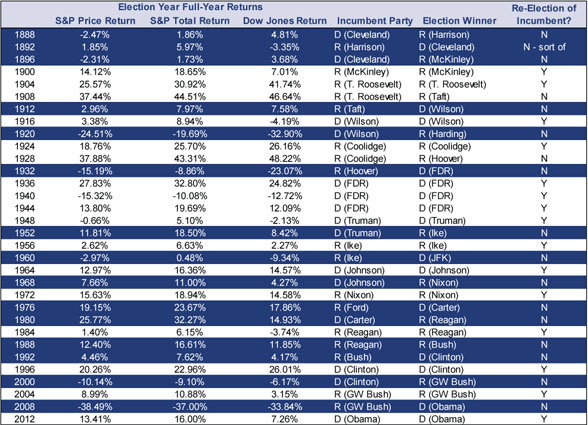

Before we debunk these myths, here are two tables of election-year returns since 1885-the year the Dow Jones Industrial Average was born. Of course, back then, it was only a handful of stocks, not even the slightly bigger handful of 30 it is today, but it was there, and there is history. S&P 500 returns have been reconstructed that far back, but anything before 1926 is widely considered less reliable, as the Cowles Commission didn't verify it. Consider it there for illustrative purposes. Anyway, the first table shows returns from 4/30 - 10/31-the "sell in May" window getting so much coverage this year, along with the incumbent, winner and whether the incumbent was re-elected. The highlighted rows indicate party changes. The second shows full-year returns alongside the same incumbent/winner data.

Exhibit 1: "Sell in May" Returns in Election Years

Source: Global Financial Data, Inc., as of 5/11/2016.

Exhibit 2: Full-Year Returns in Election Years

Source: Global Financial Data, Inc., as of 5/11/2016.

We could easily point out that S&P 500 returns are positive far more often than not, regardless of the incumbent and winner-while the Dow numbers are significantly more variable across the board-and call it a day. These numbers speak for themselves. But the myths mentioned above are worth picking apart.

1. Election-Year May Returns Are Usually Negative

We didn't bother putting May returns in the chart, because one month is too short and we aren't myopic. But the evidence for this statement-plucked by pundits from the Stock Trader's Almanac-is the Dow's average -0.8% return in election-year Mays since 1952.

As we've written many times before, the Dow is a broken index-only 30 stocks out of more than 5,000 in America (and several thousand more globally), it's price-weighted, and it excludes dividends. The broader, cap-weighted S&P 500 Price Index's average election-year May since 1952 is better, -0.2%. But it still excludes dividends. The S&P 500 Total Return Index, which includes dividends, flips positive at 0.07%. Returns were negative just 5 of 15 times. There is nothing awful about a month with a 67% frequency of positivity and positive average return-which actually exceeds the average frequency of positivity for all months.[i]

But May is one month, and 1952 is an arbitrary cutoff. Go longer, to the full "Sell in May" window as defined by the Stock Trader's Almanac (April 30 - October 31) in election years since 1926, and the S&P 500's total return is positive 80.9% of the time, averaging 5.9%.[ii] There is nothing to avoid.

2. Election Year Returns Are Bad in a Two-Term President's Second Term

This claim is based on another arbitrary observation: Since 1944, the S&P 500 averaged -3.3% (price returns) in year four of a president's second term, with a 50% frequency of positivity.

Right off the bat, you can tell this is flawed. Before Barack Obama, we had five two-term presidents since 1944: Truman, Eisenhower, Reagan, Clinton and G.W. Bush. You can't have a 50% frequency of positivity in an odd-numbered dataset. That raises questions: Should Ford or Johnson be included? For that matter, should Truman? If we go back to the 19th century, would Grover Cleveland belong? And is it too conveniently arbitrary to start the analysis after FDR?

Our number crunching revealed the mystery two-termer the analysis includes is Lyndon Baines Johnson, which is inconsistent with history, given LBJ elected not to run in 1968 when he was eligible to. His time in office (five years and two months) doesn't even round to two terms. That alone is cause for skepticism, but let's set that aside for now.

If you average the six years in question-1952, 1960, 1968, 1988, 2000 and 2008, then you get -3.3% in price terms. But if you add dividends, the negativity turns to a +0.8% gain-not great, but it isn't down.[iii]

However, the real issue here is we're talking about six data points-five, using our two-term president count. Five or six data points aren't enough to prove anything. Particularly when this five- or six-point dataset is skewed by one gigantic outlier, 2008, which featured a global financial crisis that had next to nothing to do with the election. (See here and here.) Far be it from us to debunk a tiny data set by removing an outlier and shrinking the sample even more, but for kicks and grins: Toss 2008, and the S&P 500 Total Return Index averages 7.5%.[iv] Toss 2008 and Johnson as a non-two-termer and the average is 6.6%.[v] Lesson: Beware one big number skewing a very small, arbitrary sample.

3. In Election-Year May-Novembers, Stocks Do Poorly When the Incumbent Party Loses

This final fallacy comes from this factoid: Since the Dow's creation, it averages -1.1% in election years when the incumbent party loses. (When we ran the data, we got -1.2%, which we'll chalk up to different data providers or rounding.[vi]) When the incumbent party wins, it averages 7.4%. (We got 7.5%)

This one has all the attendant Dow problems. In these same years-the ones highlighted in blue in Exhibit 1-the S&P 500's "Sell in May" price return averages 1.1%.[vii] Total returns average 3.2%.[viii] Exclude one year-2008-and S&P 500 average price returns improve to 3.2%-5.3% when you include dividends.[ix]

But the real flaw here is the philosophy. Cherry-picking returns when the incumbent party wins ignores re-election. When incumbents win second terms, there is less uncertainty. All else equal, that bodes well for stocks, which despise uncertainty and are generally fine with extending the status quo. So for this logic to hold up-and to imply a Democratic candidate winning this November is inherently bullish-the analysis would have to look at newly elected presidents from the same party as the prior administration. Since reliable S&P 500 history begins, we have a whopping two: Herbert Hoover (1928) and George H.W. Bush (1988). That's it. (Even if we expand it to the Dow's inception, there are only three-Taft, 1912.) Returns were fine both times, but two data points prove nothing.

[i] Source: Global Financial Data, Inc., as of 5/10/2016. The frequency of positivity from 12/31/1951 - 4/30/2016 was 62.7%. Since 1926, it is 61.9%, so no matter how you slice it, May in election year is more frequently positive than the average month.

[ii] Ibid. S&P 500 Total Return Index April 30 - October 31 average return and frequency of positivity in election years from 1928 - 2012.

[iii] Ibid. S&P 500 average total return for the years 1952, 1960, 1968, 1988, 2000 and 2008.

[iv] Ibid. S&P 500 average total return for the years 1952, 1960, 1968, 1988 and 2000

[v] Ibid, of S&P 500 average total return for the years 1952, 1960, 1988 and 2000.

[vi] Ibid. Dow Jones Industrial Average April 30 - October 31 return in election years from 1888 - 2012.

[vii] Ibid.

[viii] Ibid.

[ix] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Pumping Up the Yen?2026-07-17

-

Expert Commentary This Week in Review | US-Iran Conflict, US Inflation, New UK Prime Minister

2026-07-17

2026-07-17 -

Market Analysis Business Friendly Bureaucracy or No, Britain is Growing2026-07-16

-

Economics Don’t Doubt the Old World2026-07-16

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today