Personal Wealth Management / Market Analysis

Industry Isn’t Producing a Recession

Industrial production's recent contractions don't mean recession is nigh.

As the global expansion nears its seventh birthday, many folks see worrisome signs that the "r" word-recession-looms. As evidence of weakness, they point to contracting industrial production, now down in 10 of the past 12 months-presuming industrial production is a forward-looking economic indicator. Spoiler alert: It isn't. And that isn't the only shortcoming to this theory. A closer look at the data reveals some other big caveats. In our view, recession doesn't look likely.

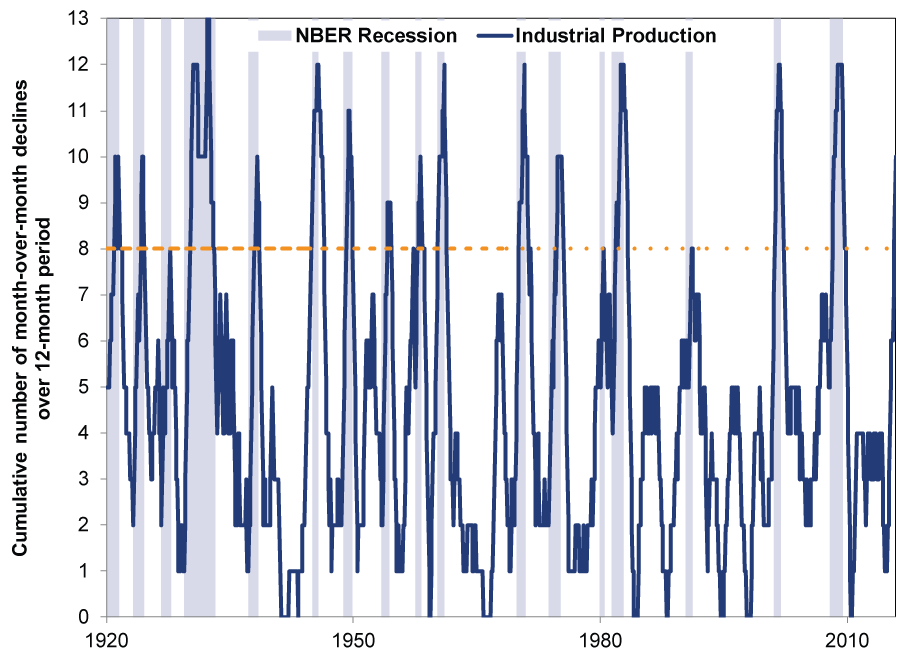

First, the stats behind the fear. According to one pundit, when industrial production falls at least 8 months in a 12-month period, it's a surefire sign a recession will occur. Here is the messy chart allegedly supporting this thesis (Exhibit 1).

Exhibit 1: Does Industrial Production Foresee Recession?

Source: St. Louis Federal Reserve, as of 1/26/2016. Recession dating from NBER.

Essentially, the theory goes, when the dark blue line passes or touches[i] the orange line (marking 8 months of falling industrial production over the prior 12 months), that spells recession. And because industrial production has fallen in 10 of the past 12 months, this methodology suggests an economic downturn is virtually assured. Yet reality is a bit more nuanced.

Using past performance-i.e., waiting for industrial production to hit the magic number of eight drops-to make a forward-looking economic forecast is always a fallacy. There are multiple instances when industrial production had its eighth drop well after recession began. Though difficult to see on the chart, drop number eight didn't occur until a year into the 1923-1924 recession. The 1925-1926 recession? 13 months. It took 9 months to flash in the 1953-1954 recession and 10 months for the 1973-1975 recession. More recently, nine months passed before industrial production supposedly announced the 1990-1991 recession. Maybe this is just us, but if your fancy "recession indicator" doesn't actually confirm it until you're almost a year into one, perhaps it needs some retooling. Or perhaps this is largely a matter of confusing coincidence with causality. That is, if the economy is suffering a downturn, industrial production goes down as well-not necessarily first. The noisy chart shows effect, not cause.

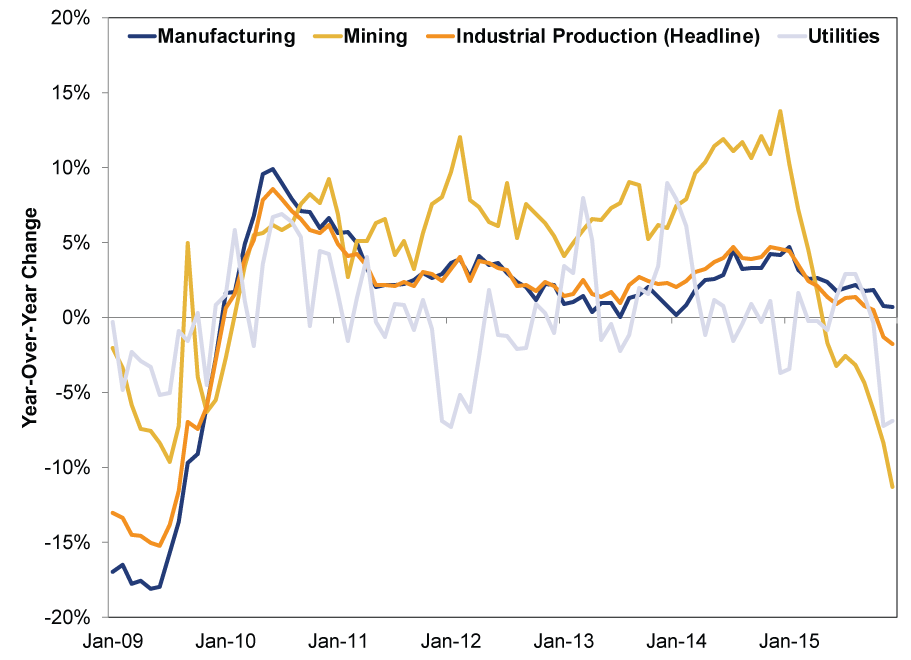

A deeper look at industrial production's components suggests the drop isn't recessionary. Though December industrial production dropped -0.4% m/m (-1.8% y/y), most of this negativity comes from Mining (-0.8% m/m, -11.2% y/y) and Utilities (-2.0% m/m, -6.9% y/y). Mining has unsurprisingly been slammed by falling energy prices while Utilities are down due to mild weather,[ii] reducing demand for home heating. (Maybe Winter Storm Jonas is actually economic stimulus?) However, Utilities and Mining comprise a little more than 25% of total industrial production. The largest swath belongs to Manufacturing, which makes up more than 70% of industrial production-and is a better gauge of actual US heavy industry. Manufacturing wasn't hit as hard, down a smidge at -0.1% m/m (0.7% y/y).

That's just one month, but the story broadly applies to Industrial Production's 2015 wobble. Here is a chart showing headline industrial production and its components on a year-over-year basis during the current expansion (Exhibit 2).

Exhibit 2: Industrial Production and Its Components, Year-Over-Year Change, Since 2009

Source: St. Louis Federal Reserve, as of 1/27/2016. From 1/1/2009 - 12/31/2015.

Headline Industrial Production and Manufacturing usually track each other pretty closely, but Mining and Utilities have pulled the headline index below Manufacturing for a year. Despite Mining and Utilities' drag, Industrial Production's current downturn is still small compared to other comparable contractionary 12-month stretches. Over the past 12 months, industrial production has fallen cumulatively by -1.8%.[iii] Compare that to May 2008-May 2009-the throes of the last recession-when industrial production plummeted -15.0%.[iv] Even during milder recessions, the drops were much steeper. From November 2000-November 2001, the gauge fell -5.5%[v] while from December 1973 - December 1974, it slid -8.5%.[vi] This current contractionary stretch is tame by historical standards, even including Mining and Utilities' isolated impact.

From a higher level, consider industrial production's slice of the total economy. Manufacturing makes up approximately 12% of GDP.[vii] Mining and Utilities combined are a little more than 4%.[viii] Compare that to services-related industries, which comprise nearly 70% of GDP.[ix] For those worrying the headwinds slamming Mining and Utilities will knock industrial employment-which will then cause a decline in consumption and affect the services sector-this goes a teensy bit too far. Utilities output is highly weather-related, and we doubt many firms lay folks off because of a warm December, particularly given January has delivered the Northeast a slight change. Mining, including oil production, makes up about 0.5% of total nonfarm payrolls.[x] Though layoffs likely will mount as producers respond to the global commodity supply glut, this isn't a macro-level negative that packs the power to derail the economy. (Besides, unemployment tends to lag growth, not lead it, but we digress.)

Other data suggest recession doesn't look likely, as the US economy is much more than just industrial production. Though the ISM's December Manufacturing PMI remained below 50 at 48.2-signaling more companies contracted than expanded-this isn't a big negative surprise, given manufacturing's recent soft patches, not just in the US but globally. Non-Manufacturing PMI (which, interestingly enough, includes both Mining and Utilities) finished December at 55.3, a bit slower than November but still well in "expansionary" territory. Total consumer spending has been chugging along. And though The Conference Board's Leading Economic Index (LEI) fell -0.2% m/m in December, month-to-month figures can be volatile and this is only the fourth drop in the past year. More important is its longer-term trend, which is high and rising. Moreover, the negativity comes from LEI's noisier components. The interest rate spread and Leading Credit Index-the two most consistent and prescient components-were the biggest positive contributors.

In our view, investors should beware proclamations about the forecasting power of any single economic gauge-especially one as limited as Industrial Production.

[i] That's convenient.

[ii] Nationally speaking, we presume. Because it was pretty darn cold (relatively speaking) in the Bay Area.

[iii] Source: St. Louis Federal Reserve, as of 1/28/2016. Industrial Production cumulative change, from December 2014 - December 2015.

[iv] Ibid. From May 2008 - May 2009.

[v] Ibid. From November 2000 - November 2001.

[vi] Ibid. From December 1973 - December 1974.

[vii] Source: Bureau of Economic Analysis, as of 1/27/2016. Value Added by Industry as a Percentage of Gross Domestic Product, 2014.

[viii] Ibid.

[ix] Ibid.

[x] Source: Bureau of Labor Statistics, as of 1/27/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 11 - May 152026-05-18

-

Behavioral Finance Investing Lessons From the Indianapolis Motor Speedway2026-05-18

-

Expert Commentary 3 Things You Need to Know This Week | Global Inflation, Fed Minutes, US Sentiment2026-05-18

-

In The News Around the World in Tax Policy Talk2026-05-15

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today