Personal Wealth Management / Economics

Manufactured Worries About the Future

Data reinforcing one sector's well-known struggles don't mean trouble for the broader economy.

Uh-oh: A widely followed manufacturing gauge just dropped to a three-year low, contracting for the first time since 2012. Many blame the strong dollar and low commodity prices for wreaking havoc with US manufacturers over the past year, and with the latest weak showing, pundits are worried. Some warn the sector's troubles are the "canary in the coalmine" for the broader economy. Yet a look at the bigger picture suggests worries are a wee bit overwrought.

We'll call a spade a spade, though: The numbers weren't great.[i] The Institute for Supply Management's (ISM) November Manufacturing Purchasing Managers' Index (PMI)-a survey attempting to measure economic activity in a given sector-slipped to 48.6 from October's 50.1. The forward-looking New Orders subindex also declined, to 48.9 from the prior month's 52.9. Readings above 50 indicate more businesses grew in a given month, while under 50 says more businesses contracted. Thus, the quick-and-dirty interpretation says readings over 50 indicate expansion. But PMIs capture only the breadth of growth, not the magnitude, so that quick-and-dirty interpretation isn't always spot-on. And for what it's worth, a separate manufacturing PMI gauge published by Markit put November US Manufacturing PMI at 52.8-not contractionary, but at its weakest level in three years, tracking the ISM survey's direction. None of this is an exact science, but surprises move markets, and these figures are consistent with manufacturing's current global-ish soft patch-by now a very well-known phenomenon.

However, manufacturing's struggles don't necessarily portend to broader economic troubles. For one, consider ISM's guidance: "A PMI above 43.1 percent, over a period of time, generally indicates an expansion of the overall economy." This acknowledges a manufacturing reading below 50 alone isn't worrisome for the broader economy, which is predominantly services-based. Manufacturing readings, at least by this measure, must drop much further to approach levels associated with deteriorating economic conditions-and stay there. Under those circumstances, other sectors are likely struggling, too. History shows this as well. One of the benefits of ISM's report is its long history-it has been around since 1948, covering more than 10 full business cycles. When it dips below 50, economic trouble doesn't always follow: False reads abound. (Exhibit 1)

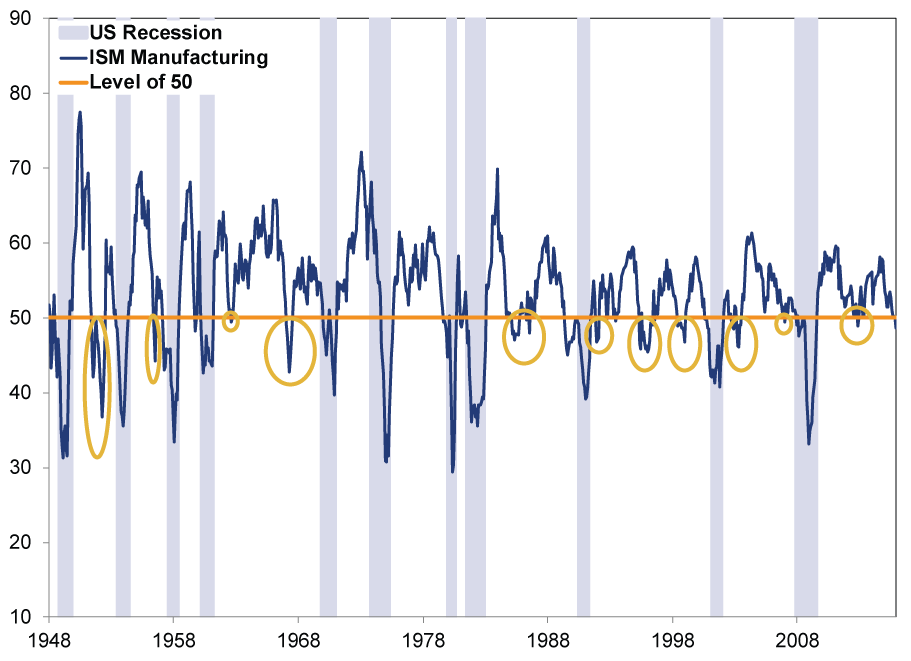

Exhibit 1: ISM Manufacturing Since 1948

Source: St. Louis Federal Reserve, as of 12/1/2015. From 1/1/1948 - 11/30/2015. Recession dates as determined by the National Bureau of Economic Research.

While the chart is a bit messy, note the circled inflection points: There are multiple instances when ISM's Manufacturing gauge fell in the contractionary zone, yet no recession followed-including that widely cited last dip below 50, in 2012. Also, consider the increasing frequency of non-recessionary manufacturing dips in recent decades-a reflection of the US economy's shift to a services- and consumption-based economy. By some researchers' estimates, manufacturing's share of value added in nominal GDP has decreased from about 25% in 1960 to about 12% in 2010-a decline of more than half. This isn't because output is down in the manufacturing sector over that span, but because other areas grew quicker.

Some of those other areas are included in the ISM's Non-Manufacturing PMI, which covers sectors amounting to more than 80% of the US economy. In recent months, as Manufacturing slowed, Non-Manufacturing ticked higher-suggesting the bulk of the US economy is growing fine. In November, ISM's Non-Manufacturing PMI slowed a bit to 55.9 from October's 59.1, but still remained well above 50. Even more broadly, the second estimate of Q3 GDP growth-2.1% seasonally adjusted annual rate, higher than the preliminary 1.5% estimate-showed consumer spending contributed nicely to headline growth. Though a bit stale, considering we're two months into Q4, it too coincided with overall weak heavy industry, which didn't prevent growth. These bits of evidence suggest this expansion's primary drivers remain intact.

Of course, no economic data coverage lately would be complete without the requisite handwringing over what it means for a potential Fed rate hike. The latest episode has some wondering if November's manufacturing contraction will give the Fed pause-especially since the Fed has constantly said its decision will be "data-dependent." Of course, that was before Fed head Janet Yellen's widely publicized Washington speech, which most observers interpreted as talking up the likelihood of a hike. As always, we caution investors from projecting central bankers' words into definitive action. We have devoted many pixels to why central bankers should not be taken at their word-their "forward guidance" hasn't been very reliable. However, we do know history shows an initial rate hike is a negligible threat to economic growth or the bull market. The sooner the Fed hikes, in our view, the better, to put this false fear to rest.

There has been a dearth of rousing economic news lately, so we understand why many latched onto one manufacturing survey's contraction. However, while it confirms the sector's tough sledding, it doesn't indicate much about the broader economy. Even during an expansion, growth won't be uniform-some spots will struggle. But the US economy and the global bull market shouldn't trip just because one sector slips.

[i] We like our numbers like we like our facts: plain. No seasoning, sugar-coating or additional flavoring needed.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 11 - May 152026-05-18

-

Behavioral Finance Investing Lessons From the Indianapolis Motor Speedway2026-05-18

-

Expert Commentary 3 Things You Need to Know This Week | Global Inflation, Fed Minutes, US Sentiment2026-05-18

-

In The News Around the World in Tax Policy Talk2026-05-15

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today