Personal Wealth Management / Market Analysis

Investing in a Maturing Bull Market

As the bull grows older, owning stocks makes sense for most-but your long-term financial goals still rule.

Is owning-or buying-stocks now a sucker's move? Headlines, predictably, differ. Some argue Q1's rally rested on a shaky foundation of overexcited retail investors, while the "smart money" wisely shied away from too-high valuations-a sign of stocks breathing their last. Others recommend piling into stocks now to capture lofty returns as euphoria takes hold. Who's right? We're bullish and think stocks will have a great year, but the right way to view this debate isn't to pick a side. Rather, it's to let your long-term financial goals determine how you invest, not a near-term forecast of the bull's lifespan. If you need long-term growth, stocks should feature heavily in your portfolio by default, and you should veer only if you are darned sure a bear market has begun.

We don't think that time is now. Many cite rising price-to-earnings (P/E) ratios to argue a bear is approaching. One recent report listed 20 different S&P 500 valuation metrics, most well above historical averages. While we quibble with how many are constructed, the basic point they loosely illustrate is accurate-sentiment is warming. That is normal during maturing bull markets and nothing to fear.

But we have nothing nice to say about gauges of retail investor enthusiasm, which supposedly show Low-Information Joes and Janes are the sole buyers-a traditional contrarian indicator of peaking markets. Nonsense! The one cited here merely shows inflows into SPY-an S&P 500 ETF-which just happens to be the most heavily traded security in the world, popular with individuals and professionals and institutions . Another popular supposed indicator-stocks' rising share of total household assets, as reported by the Fed-is a function of market movement, not investor behavior. If you start with 70% stocks/30% bonds, and stocks outperform bonds, they will gain a larger share of your portfolio even if you don't make a single trade. Besides, "dumb" and "smart" money are fictions. No one has cornered the market on poor investment decisions-not institutional investors, corporate insiders or retail investors.

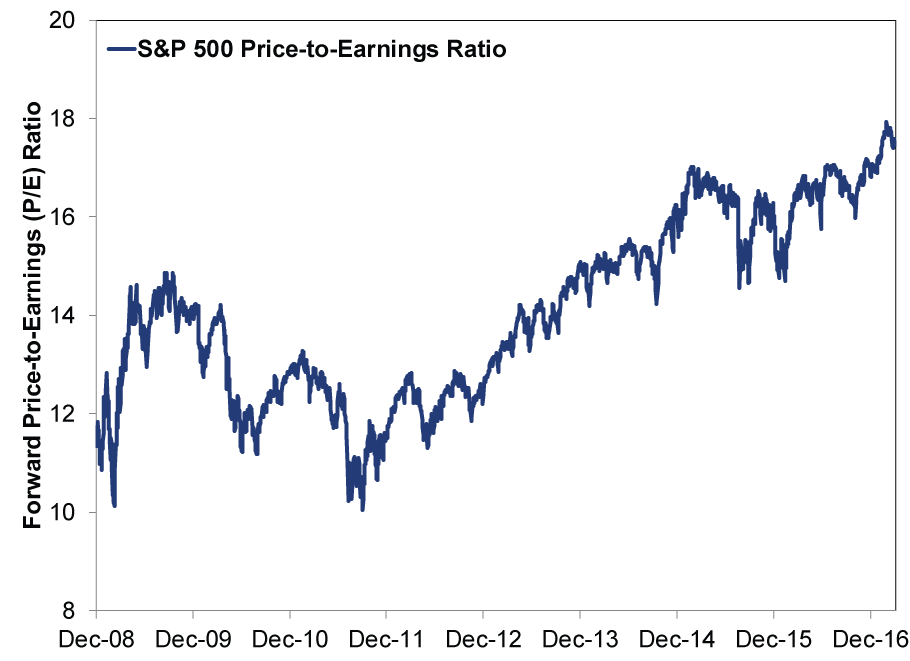

To us, all the handwringing over burgeoning euphoria proves one thing-it isn't here yet. Optimism is spreading, but only gradually, in fits and starts, which is consistent with valuations' slow, choppy rise. A sudden surge in valuations could signify euphoria, a la 2000, but today's rise bears no resemblance.

Exhibit 1: Valuations Aren't Surging

Source: FactSet, as of 4/6/2017.

Rising P/Es aren't bearish. There is no ceiling-a "high" P/E can get higher, and often does in a bull's last third or so, when stocks frequently accelerate. Some of the 1990s bull's best years came after then-Fed head Alan Greenspan warned of irrational exuberance in 1996. Fading skepticism hints we may be entering this final stage, setting up big gains.

But while this is our view, it isn't why we think long-term growth investors should own stocks now-we'd say the same even if we expected only mild returns this year. The goal in equity investing shouldn't be to target only big positive returns. The stock market is not a get-rich-quick machine. Buying only when you anticipate a big, near-turn payoff misses the importance of asset allocation. If stocks' returns are right for some or all of your portfolio, you are unlikely to achieve your goals by sitting in cash and jumping in when you expect heat. It doesn't take a boatload of academic research to show this is a risky approach, but researchers have looked into it anyway-and sure enough, most investors turn out to be poor market timers, as emotions like fear and greed drive decisions and slash returns.

If your goals require equity-like growth and you don't have a super-solid reason to expect a bear, you should own stocks regardless of how high or how much longer you think they might rise. It's easy to cite some reason to stay on the sidelines-new market highs, recent dips, scary stories of huge threats markets are overlooking, the belief things will calm down soon, so why not wait?-you name it! Don't let this be your default. Rather than fixate on the risks of owning stocks, consider the opportunity costs of staying out-they're often substantial.

Asking yourself basic questions about why you're investing in the first place can add useful perspective. So start there. Ask yourself: What are your financial goals? Do they require growth? How much, and over what timespan? What sort of cash flow do you think you'll need to live comfortably in your golden years? The answers should guide how much you put in stocks and bonds. Only after you know what this mix is-your default asset allocation-should you weigh market direction.

For those whose goals necessitate owning equities, switching to bonds or cash makes sense in rare cases-namely, during bear markets (prolonged, fundamentally driven market downturns of at least -20%). Don't jump the gun, though. Historically, bull markets rise powerfully before rolling over into a bear. Bear markets typically don't begin with huge drops, either. Hence the saying that bull markets die with a whimper, not a bang. Stocks usually decline gradually at first, and steep drops arrive later in the bear. This leaves plenty of time to determine that a bear market is underway and adjust your allocation accordingly. Acting before a bear market risks missing gains. Plus, while avoiding a bear market or two is nice, reaching your financial goals needn't (and shouldn't) depend on it.

So while it's tempting to draw sweeping conclusions from talk of retail investor excitement and above-average valuations, we don't think it justifies big moves into or out of stocks right now unless your long-term goals require stocks and you don't presently own them. The bull market is going strong, so own stocks if they fit your goals. But don't let short-term market forecasts cloud your vision or rouse your emotions.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights.

Sign up for our weekly e-mail newsletter.

See Our Investment Guides

The world of investing can seem like a giant maze. Fisher Investments has developed several informational and educational guides tackling a variety of investing topics.

SHARE THIS MEDIA

Related Resources

Learn More

Learn why 150,000 clients* trust us to manage their money and how we may be able to help you achieve your financial goals.

*As of 3/31/2024

New to Fisher? Call Us.

Contact Us Today