Personal Wealth Management / Market Analysis

New Highs, Old Fears

Stock market records raise more unfounded concerns of a "too far, too fast" rally.

Last Wednesday, the S&P 500 hit its 200th new high of this expansion-a nice, big round number! And, before you put your party hats away, this Thursday the global bull market turns eight. On March 9, 2009 the global financial crisis-driven bear market ended, and the march upward since is now the second-longest in history. The two (somewhat arbitrary) markers recall two longstanding false fears: That market records signal stocks are too high and aged bull markets must die soon. Neither is correct, and skeptical headlines today suggest there is more wall of worry for this bull market to climb.

Open a newspaper,[i] and you'll see frequent coverage of new market highs alongside projections that they can't last. If this sounds familiar, it's because such stories have tracked markets' rise for years, as folks repeatedly declare the latest record high is near a market peak.

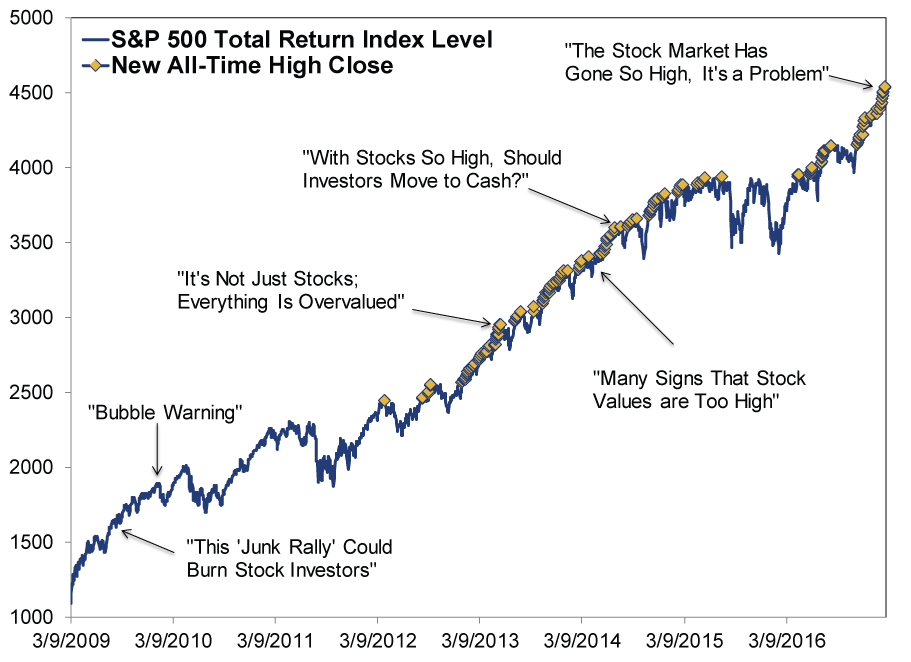

Exhibit 1: 200 S&P 500 Record Highs

FactSet, S&P 500 Total Return, 3/9/2009 - 3/1/2017. Source, source, source, source, source, source.

Heeding those warnings would have cost you dearly. This bull market's first record came on April 2, 2012. From then to June 4, 2014's 100th new high, the S&P 500 rose 42.5%.[ii] From number 100 to last week's 200th record, stocks rose another 31.7%. Cumulatively, in the nearly five years from the first new record high to last week's, stocks were up 87.7%-big! Despite all the acrophobia, stocks reaching new heights over and over again is a bull market regularity, which means obsessing over round (or any) number milestones merely wastes time and energy. Stocks look ahead, rendering milestones meaningless, no matter the index.

Still others fear eight years means the end must be nigh-and it's true that this bull market is longer than the historical average of about five years. But averages don't govern stocks-they result from longer and shorter periods blended together. There is no mean reversion in markets, which can be above average in length, magnitude or valuation for very, very long periods. Markets aren't people or animals, and they don't get "tired" or "long in the tooth." Bulls end for concrete reasons. Most often, investors get punch drunk on big past returns, ignore risks and raise expectations to levels reality can't meet. Alternatively, a widely unnoticed negative worth trillions of dollars can sneak up and wallop stocks, killing a bull.

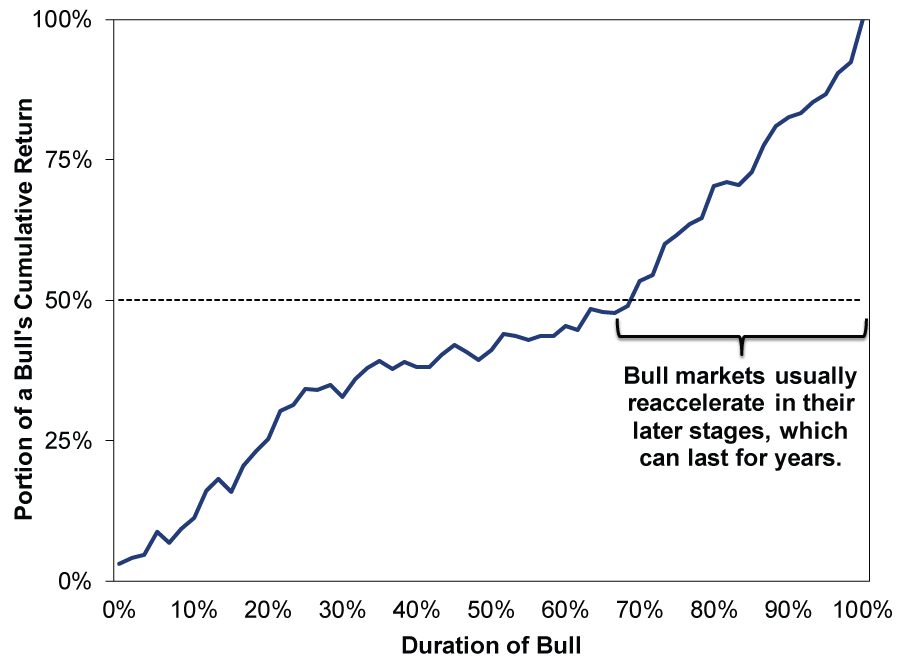

We are keenly aware that this bull market will eventually end, but that end doesn't seem nearby today. We don't presently see any negatives with wallop potential looming-pockets of weakness are either minor, widely known or both. And, though sentiment in America has warmed some recently, optimism typically lasts for long periods before markets peak. After all, while returns in the last year look nice, this follows a deep correction and an overall ho-hum period-far from the bigly returns that usually feed euphoria. Typically, bull markets accelerate to their peak, with large portions of total return coming in the last third or so.

Exhibit 2: Finishing Strong

Source: Global Financial Data, Inc., as of 11/9/2016. Depicts bull markets from 6/1/1932 - 10/9/2007. Bull markets before 1990 rounded to nearest month to match GFD's S&P 500 Total Return extended data.

That acceleration may be underway now. But even if it's started, there could be a long way to go still. Take the 1990s, for example. Many recall former Fed head Alan Greenspan warning of "irrational exuberance" in December 1996 based, in part, on valuations. Stocks rose another 116% over the ensuing three-plus years before the bull peaked.[iii]

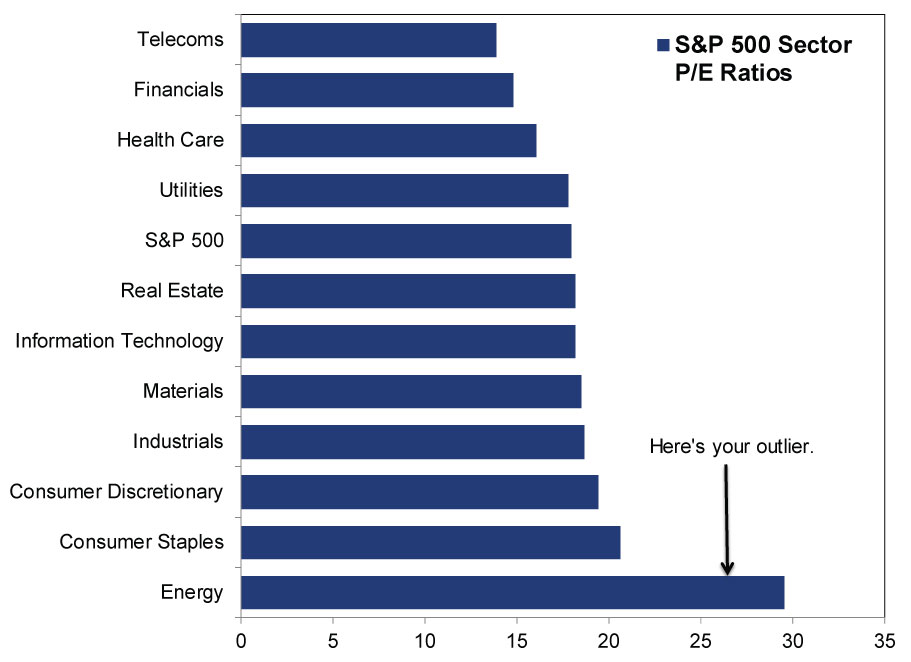

Plus, most sentiment metrics today are only showing nascent optimism, not exuberance. US forward price-to-earnings ratios barely exceed historical averages, and have only recently turned higher after an extended flattish stretch. And as Exhibit 3 shows, even those figures are skewed upwards by Energy-the sector's profit collapse from 2014 - 2016 slammed the P/E denominator, elevating the measure.

Exhibit 3: Energy Leads P/Es

Source: FactSet, as of 3/3/2017. S&P 500 sector forward 12-month P/E ratios.

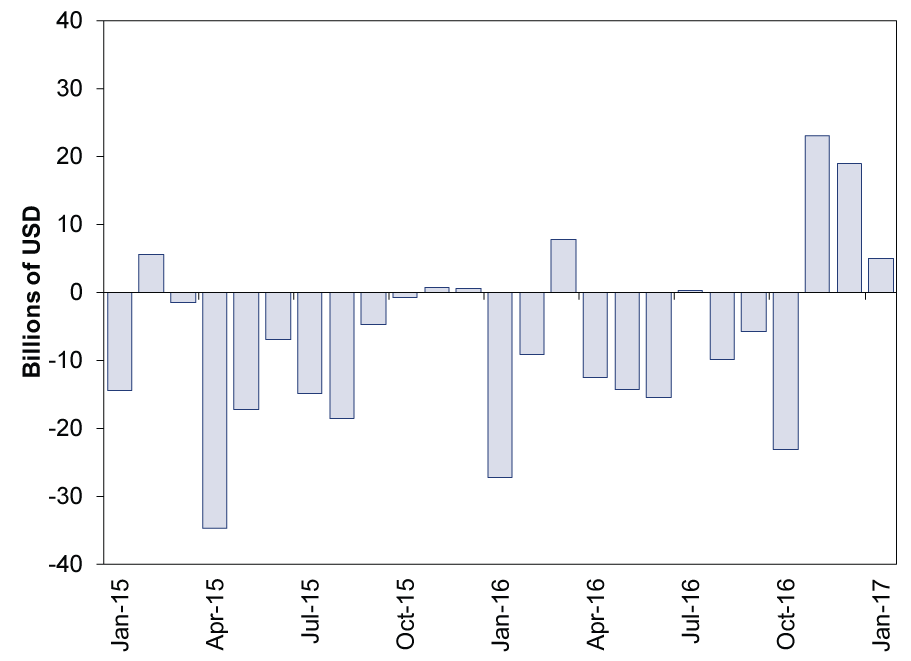

Ditto for other barometers of investor mood. US equity mutual fund and ETF flows have been positive in 2017-another sign of percolating optimism-but this follows a very long streak of net outflows and amounts to only $46 billion total to date.[iv] (Exhibit 4)

Exhibit 4: US Equity and ETF Net Fund Flows

Source: The Investment Company Institute, as of 3/7/2017.

Rather than suggesting sentiment is stretched, these gauges suggest optimism. And it looks like pretty rational optimism, when you consider the US and Europe are growing, business surveys show expansion, loan growth is steady and leading economic indexes are trending up. Heck, Citigroup's US Economic Surprise Index-a measure comparing professional expectations to economic data-has trailed European versions lately, but it is still solidly positive. Reality is better than pros anticipated. Meanwhile, the media frets over European elections, "Trump trades," inflation and allegedly too-low volatility.[v] To this we say: Where's the exuberance?

With that bullish backdrop in place, it seems to us yet more arbitrary markers of this bull market's progress in climbing the wall of worry are in store.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Oil prices will be lower in 6 months than when Iran conflict began, Ken Fisher argues2026-03-12

-

Market Analysis Rounding Up Odds and Ends From Global Energy Developments2026-03-11

-

Environmental, Social and Governance Insights Responsible Investment Newsletter 20262026-03-11

-

Economics Pain at the Pump Won’t Hurt the Global Economy2026-03-10

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today