Personal Wealth Management /

I-P-O Doesn’t Spell E-Z M-O-N-E-Y

Investors looking to hit the jackpot with an IPO may end up disappointed.

The letters “I-P-O” have been flying off investors’ tongues lately, thanks largely to a little birdy nested in San Francisco. After this company took flight to much fanfare and a 75% gain, some investors were hot to find the next shiny new company. After all, who doesn’t want to be one of the first in on the next Apple? Think of the dazzling returns—and the bragging rights! But investors zeroing in on IPOs may end up losing sight of a larger issue: A portfolio’s success shouldn’t depend on the performance of a single stock. Doing so treats investing like a sprint, rather than the marathon it is.

If you try the sprint, it’s exceedingly tough to win. For one, as the old saw says, IPO stands for, “It’s probably overpriced.” Consider the primary reason a company decides to go public: to raise capital from investors. The initial share price determines the payout, so it’s in the company’s interest for the offering price to be as high as possible without crimping demand.

This offering price is what the media highlights. However, individual investors rarely buy shares at this price (or if they do, the number they receive is ordinarily tiny). Underwriting banks usually give preference to their own preferred clients along with institutional investors. Typical individual investors are much likelier to purchase an IPO after the stock has started trading on the secondary market.

There, sentiment can quickly create a high premium on IPOs. For example, let’s say a particular company—Energy Company X—is garnering a lot of buzz. You see headlines proclaiming it’s hot ... exciting ... people “in the know” sing about its potential. They’re everywhere! Which makes it a virtual certainty many other investors will see the same reports and want to get in on Energy Company X ASAP. Since the market is an auction place, you all compete for the same shares, and they go to the highest bidder, which pushes the price up—not for any sound fundamental reason, just because of the hype. Buying in when hype is hottest means you’re likely paying a premium for no great reason.

So why would an investor make an oversized bet in a company with no track record and, in some cases, no profits? Many just cling to the belief pursuing IPOs will eventually lead to that one magic company that yields super-duper returns—basically treating investing like a get-rich-quick scheme. But this assumes one stock (1!), chosen solely for its potential, can immediately make you set for life. Sure, some IPOs may eventually become awesomely profitable investments—the success stories are out there—but many won’t either. And the return on investment may not be as quick as expected—will you remain patient enough to be a part of that success story?

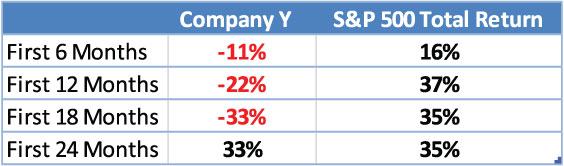

Let’s take a real-life example. A company has an IPO in August 1988, opening at $9.38 a share, and you buy in the first day. Here’s the performance for the next 24 months:

Source: Yahoo! Finance and FactSet Data Systems. Returns calculated using adjusted closing price from August 18, 1988 - August 17, 1990.

Imagine buying into this company solely because of its “potential” and then watching it fall by 33% for the next year and a half while the S&P 500 Total Return index rose 35%! Could you stomach watching this one company fall precipitously while markets were generally up big? Especially when you bought in solely because you expected an immediate pop? If you’re like most investors, probably not—think of all the other opportunities for gains!

Sometimes, selling is the right move. But other times, patience pays. It sure did for this mystery company. What was it? The stock to own during the 1990s: Dell. By the time it hit its all-time high on March 23, 2000, after years of split after split, the stock had returned an astounding 62,378% since its IPO.

Throughout the Tech bubble, many investors went on the hunt for “the next Dell,” but the vast majority missed. And even if they didn’t, few recalled Dell’s less-than-glorious rookie year and went instead for stocks they thought would hit it big immediately—and bought quite a few stinkers. Of the 154 companies that debuted in the bubble’s final three months, 15 are still listed. Investors kicking the tires on IPOs because they’re trying to “find the next Dell” will probably not get their dream returns immediately, if at all. Attempting to do so is like trying to win the lottery—and, as government regulators frequently warn, the lottery “should be considered a form of entertainment and should not be played for investment purposes.” Investing is a long journey toward goals and objectives, in my view.

And when you slow down and think about it, how much are you really going to put into a stock that just debuted? Concentration is risky, whatever the company. Would you put most or your entire portfolio into one Japanese Tech stock? Or one American Healthcare company? Or one Eastern European manufacturer? I wouldn’t think so. You’d want to diversify to reduce risk, just in case, especially if you need this money for the long term. Same with IPOs! Even if you pushed it, putting 5% of your portfolio into one IPO, it likely wouldn’t move the needle. If it worked out, it would help, but it wouldn’t make or break your total return.

So if you got in on Dell, Apple or some other superstar stock before everyone else, kudos to you! You hit a homerun! But investors don’t need the home run to achieve long-term growth. Singles and doubles win ball games, too.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16 -

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today