Personal Wealth Management / Market Analysis

October’s Less Gloomy Business Surveys

Strengthening services help pick up the slack for weak manufacturing.

When last we looked at US and eurozone purchasing managers’ indexes (PMIs) in August, US manufacturing was in slight contraction and Europe was also facing industrial headwinds. Many saw—and still see—this as a sign of impending recession. Now October’s PMIs indicate a pickup in overall business activity despite continued global manufacturing weakness. In our view, this cuts against widespread fears of a manufacturing slump spreading to the broader economy—potentially a bullish surprise for investors.

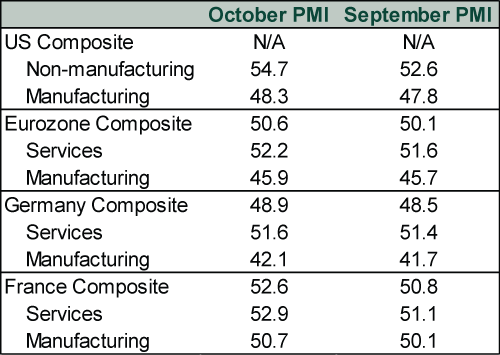

PMIs are surveys gauging how many businesses in a given sector—typically manufacturing and services—are expanding or contracting, with 50 the dividing line between the two. The below snapshot of four major developed-world PMIs shows all improved from September.

Exhibit 1: October’s PMIs Are Up

Sources: IHS Markit and the Institute for Supply Management, as of 11/6/2019.

We aren’t trying to make a ton out of this. Just as we wouldn’t overthink incrementally lower PMIs, small upward moves aren’t all that significant. While moves above or below 50 are notable, reading too much into a single month’s move is an error. PMIs measure only growth’s breadth (how many firms are expanding), not its magnitude (by how much). PMI surveys weight all respondents equally, even though just a few big firms can sway quantity-based output measures far more than many smaller firms can.

Hence, the overall trend matters more. In the US, October’s manufacturing PMI ticked up for the first time since March but remained below 50, suggesting factories still feel the crunch from softer demand from China and the eurozone. Meanwhile, the majority of non-manufacturing firms reported growth, as they have for the better part of a decade. Forward-looking new orders’ 55.6 October reading also suggests the sector isn’t about to stumble. Given services’ economic footprint is far larger than manufacturing’s, this seems like a recipe for continued growth.

Across the pond, pundits focused on Germany’s contractionary composite PMI, but the readings weren’t all that different from September’s. Manufacturing PMI edged higher, but at 42.1 it remains near levels last seen around 2008 – 2009’s global recession. German factory orders perked up in September, potentially signaling output is starting to stabilize. But it was one positive month in a volatile series, suggesting it is premature to declare it a sign a full-fledged industrial recovery is in the offing. Importantly, German manufacturing weakness didn’t infect October’s services PMI, which ticked up and remained in expansionary territory. The composite PMI—which combines manufacturing and services—stayed below 50, but we wouldn’t read a ton into that. Even if German GDP contracts again, it seems clear the bulk of its economy (read: services) is doing ok.

More broadly, the eurozone composite PMI improved to 50.6 in October. Nothing stunning, but contrary to headlines fretting stagnation, most eurozone businesses are growing—led by France. While the 1.8 point jump in France’s composite PMI in October merely returned it to this summer’s levels, rising new orders hint at more activity to come. As IHS Markit’s PMI report noted: “The overall rise in activity was broad-based, as manufacturers posted a return to growth in production and service providers saw output increase at a faster pace. … New order growth accelerated in October. … Underlying data revealed a recovery in international demand, as composite new export business rose slightly.” While France isn’t growing gangbusters, this is merely the latest data pointing to improved economic conditions in the country. With many seemingly unable to fathom growth accelerating, we think this highlights the potential for a positive shock.

Taking a step back, the economic outlook in America and Europe doesn’t seem to have changed much. Manufacturing is still in a soft patch globally, but services—more than two-thirds of developed-world GDP—appears to be buoying growth.[i] For stocks, what matters is how expectations square with reality. Many believe the manufacturing-led global slowdown is a prelude to recession in much of the world. But the data—including October’s PMIs—don’t appear to support this. From a sentiment perspective, we see this as bullish. In our view, reality should keep clearing expectations, boosting stocks.

[i] Source: Organisation for Economic Cooperation and Development, as of 11/6/2019. Simple average of services industry gross value added as a percentage of GDP for all developed countries except Hong Kong and Singapore, which are not tracked by the data provider. Average blends results from 2018, 2017 and 2016 due to data availability.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today