Personal Wealth Management / Economics

Quick Hit: About the US Manufacturing PMI’s Contraction

When manufacturing sneezes, the broader economy doesn’t automatically catch a cold.

Recession Watch 2019 continued this week, this time with pundits fixating on a manufacturing survey that indicated contraction. Headlines abounded claiming manufacturing is a leading indicator and it is only a matter of time until the mighty services sector falls, too—and with it, the economic expansion. However, we don’t see anything new here for stocks—or any evidence that this is anything more than a soft patch in one part of the US economy.

The reading in question was a purchasing managers’ index, or PMI. PMIs are surveys that aim to measure whether businesses overall are seeing more or less activity. Readings over 50 indicate expansion, and under 50 suggest contraction. But that isn’t airtight, as PMIs indicate only how many firms grew, not by how much. Two outfits produce national US PMIs: the Institute for Supply Management (ISM) and IHS Markit. Neither is inherently superior. ISM’s has the longest dataset, but IHS Markit’s covers more companies, and only it has an early “flash” reading. That is what garnered Thursday’s headlines.

August’s flash manufacturing PMI fell below 50—to 49.9—a slight contraction. The report also noted weakening new orders, which happen to be the survey’s most forward-looking input. The main drags, according to survey respondents: a “soft patch” in automotive industries and a weaker global economy.

Yet a global manufacturing and industrial downturn isn’t exactly new or surprising—and markets, which generally reflect all widely known information, move most on surprises. Ever since China cracked down on “shadow banking” last year, crimping credit to the country’s vast legions of small private firms, global industrial output has felt the chill from weak private sector demand in the world’s second-largest economy. Along with some other one-offs—including new EU and Chinese emissions rules—global industrial production has slumped somewhat, with automakers noticeably weak. Yet auto sales slowdowns are normal in maturing expansions. They aren’t recession triggers or indicators.

Neither is weak manufacturing overall. People presume trouble in manufacturing could spread. But manufacturing, as a narrow slice of the economy, naturally has more ups and downs than services, which are more diverse. It is just harder to see industry-specific dips within the broader services category since economic data haven’t caught up with economic evolution. Overall and on average, though, while US factories might be more vulnerable to weaker demand for physical goods in China and parts of Europe, the services and information-based industries are more immune. Their demand drivers are largely intact. This is why PMIs globally show services growing apace.

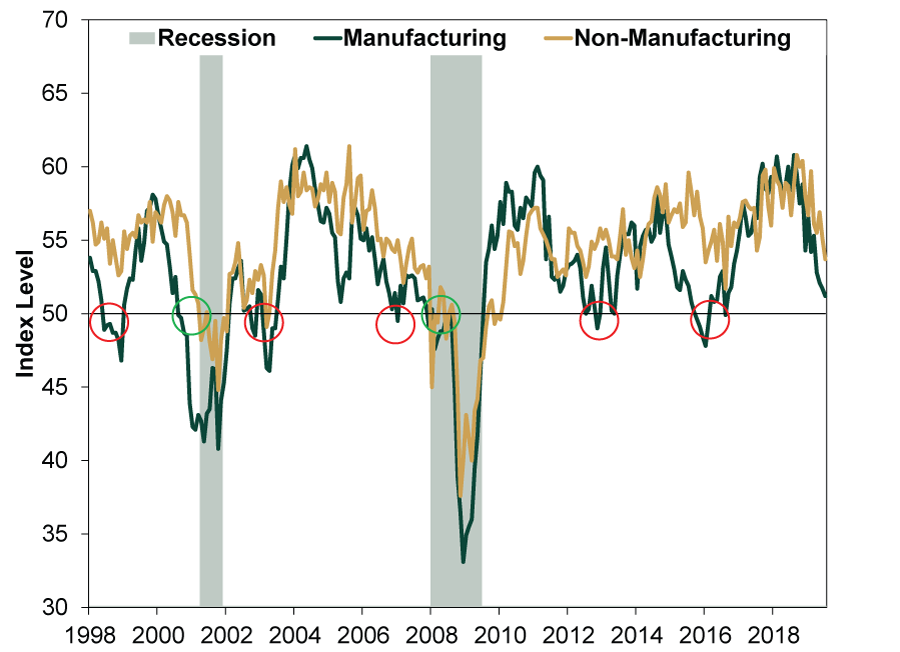

As we detailed recently, industrial activity isn’t a big growth driver in the US or the rest of the developed world. This might be the first time IHS Markit’s US Manufacturing PMI contracted during this expansion, but ISM’s has endured prior pullbacks. It dipped below 50 in 2015, causing similar alarm. But the US economy didn’t fall into recession. As Exhibit 1 shows, ISM’s manufacturing PMI had 7 contractionary spells in the last 21 years. Only two accompanied recessions (green circles). The other five were false reads—soft patches amid a broad economic expansion.

Exhibit 1: ISM Manufacturing and Non-Manufacturing PMIs

Source: FactSet, as of 8/22/2019. Institute for Supply Management manufacturing and non-manufacturing purchasing managers’ indexes, January 1998 – July 2019.

American manufacturing only accounts for 11% of GDP. Services—70% of US GDP—carried on growing. We expect similar this time. Both July’s ISM non-manufacturing PMI and IHS Markit’s flash August services PMI show ongoing growth for the bulk of America’s economy. The global services PMI indicates the same for the world. Moreover, their forward-looking new orders show they likely continue to grow. Credit continues flowing to households and businesses. Broad money supply is rising.

Markets look forward, pricing in the probable economic outlook 3 to 30 months ahead. What moves them most is how reality squares with expectations. The gloom surrounding manufacturing weakness right now suggests a low bar for reality to clear—a fine environment for stocks, which like positive surprise.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today