Personal Wealth Management / Market Analysis

Oil Prices’ Plunge Is Benign

Softer than expected US sanctions on Iranian oil exports sent oil sliding—but in context, global oil markets don’t look all that different.

Just a few weeks ago, oil market prognosticators were penciling in big price increases once US sanctions on Iran took effect on November 5. Instead, prices plunged, falling -12.2% from November 2 to November 20.[i] Given this drop comes alongside stock market volatility, many fear oil prices’ dive signals trouble for the global economy or stocks. However, we encourage investors not to buy the hype. In our view, Iran’s influence on global oil production is overstated, and falling oil prices don’t automatically bode ill.

The Trump administration had been planning to re-up sanctions on Iran since the US withdrew from the Joint Commission Plan of Action (or JCPOA)—an agreement suspending sanctions in exchange for Iran halting its nuclear program—on May 8. Now, the US hasn’t imported Iranian oil for decades, so sanctions don’t affect US trade directly. However, the primary way they work is by blocking international banks’ access to US markets if they finance transactions involving Iranian oil (or other economic entities).

Since businesses can’t simply change suppliers on a dime when sanctions are officially implemented, they frequently do so well in advance. This appears to have happened here: Iranian oil exports fell -29.6% in advance of sanctions’ November 5 implementation (that is, between June and September).[ii] While actual output data aren’t yet available, the US Energy Information Administration forecasts a marked decline in overall Iranian production (not just exports) by the end of October.[iii]

Likely anticipating sanctions’ advent would further choke off Iranian production and crimp global supply, investors bid up oil prices 16.1% between May 8 and October 4.[iv] Coverage hyped the increase, and our own Brad Rotolo penned an article addressing fears of runaway oil prices on these pages on September 21.

But then a funny thing happened: Prices began falling amid reports of higher inventories, worries over lower future demand and the growing possibility of forthcoming US sanctions exemptions. Sure enough, on the eve of sanctions’ implementation,[v] the Trump administration issued waivers to eight countries: China, India, Italy, Greece, Japan, South Korea, Taiwan and Turkey. They may keep buying Iranian crude for 180 days at least. All but Greece and Taiwan are among Iran’s top 10 oil export partners this year to date.[vi]

As markets priced in the new, pretty milquetoast sanctions reality, crude prices declined further. On cue, headlines pivoted to anticipating an Iran-fueled oil supply glut and fretting an “oil bear market.” (See here for why that is something of a misnomer.) In our view, though, short-term commodity price swings aren’t all that meaningful—oil markets remain roughly balanced despite all the Iran hoopla.

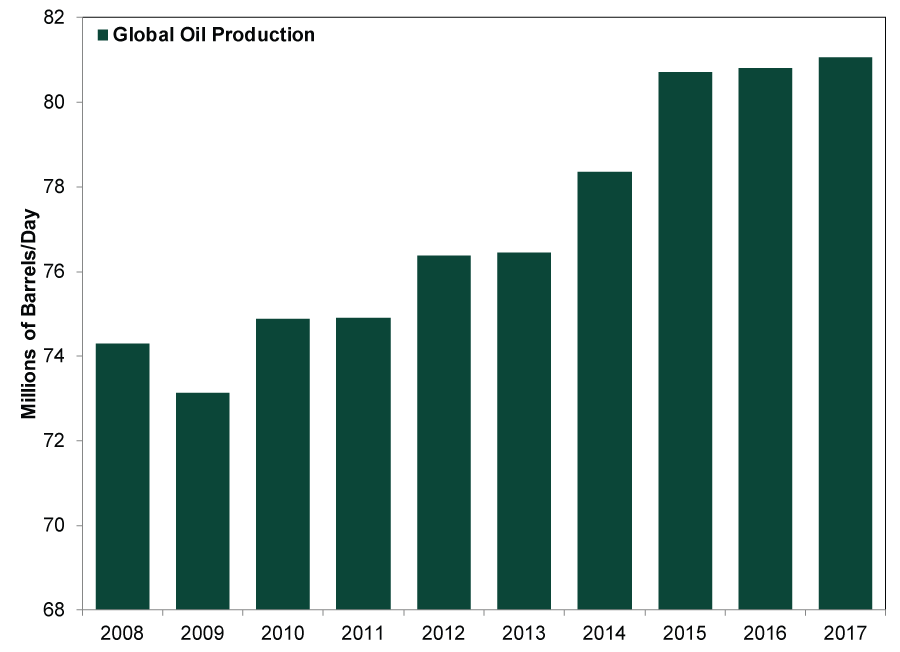

A cornucopia of fun facts and stats support this view. In 2011, Iran represented 5.6% of global oil production at 4.2 million barrels per day (bpd).[vii] By November 2013, US sanctions had subtracted about a million bpd from Iranian production—which stayed around that level until the JCPOA took effect in January 2016.[viii] Yet per Exhibit 1, global oil production rose significantly during that time, underpinned by surging US shale output. Prices, meanwhile, fell roughly 80%—funnily enough, bottoming out right around the JCPOA’s birth.[ix] This shows Iranian oil output isn’t make-or-break for global supply (or prices).

Exhibit 1: Global Oil Production

Source: FactSet, as of 11/16/2018. Global oil production, 2008 – 2017.

A similar pattern is seemingly playing out today. As Iran’s production slipped by 325,000 bpd this year, US production alone is up 1.3 million bpd, more than offsetting it.[x] In a global oil market, no one country controls prices. Cuts by one producer are often another’s opportunity to boost production and take market share.

With stock market volatility picking up again, falling oil prices are one ingredient in a stew of reasons media coverage offers for the bumpiness. Folks fear they signal weakening global demand, a sign of looming global economic weakness. But in our view, oil’s recent run-up and decline stems mainly from markets adjusting oil supply expectations—and possibly overshooting as equity market volatility roils sentiment.

History backs up this view. Again, look no further than 2014 – 2016’s oil downturn. “Weakening demand” worries raged then, too—and indeed, many US Energy firms had to retrench, drastically scaling back investment. But despite a much-hyped “earnings recession” (which, for the record, isn’t a true recession), the broader economic damage many anticipated never came. The global economy kept growing and the bull didn’t end. And that oil-price decline was over three times the current one’s size!

There could be more short-term swings yet to come—in stocks as well as oil prices. But extrapolating recent (or further) oil price dips into prolonged, deep stock market declines is groundless, in our view. For one, media have talked this topic near to death, likely mitigating surprise power. Second, although headlines often bandy about the notion oil prices are reacting to information broader markets haven’t yet priced in, energy and stock markets are both highly liquid. They price this stuff in more or less simultaneously. Third, falling oil prices aren’t bad for all industries. They benefit a huge number, too, particularly energy-intensive ones like manufacturing, oil refining, plastics and chemicals producers. Lower fuel and shipping costs also benefit many firms and industries. Ultimately, we believe the oil price fear about-face in recent weeks reflects still-skittish sentiment around a correction, not a threat to the bull market.

[i] Source: FactSet, as of 11/21/2018. Brent crude prices, 11/2/2018 – 11/20/2018.

[ii] “Iran has produced and exported less crude oil since sanctions announcement,” Matthew French, The US Energy Information Administration, 10/23/2018.

[iii] Source: FactSet, as of 11/21/2018.

[iv] Source: FactSet, as of 11/16/2018. Brent crude prices, 5/8/2018 – 10/4/2018.

[v] Sanctions Implementation Eve is way less festive than Christmas Eve.

[vi] “Iran has produced and exported less crude oil since sanctions announcement,” Matthew French, The US Energy Information Administration, 10/23/2018.

[vii] Source: FactSet, as of 11/16/2018.

[viii] Ibid.

[ix] Source: Federal Reserve Bank of St. Louis, as of 11/21/2018. Crude Oil Prices: Brent – Europe, 11/2011 – 1/2016.

[x] Source: FactSet, as of 11/16/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today