Personal Wealth Management / Economics

Overlooked Earnings

Outside Energy, Corporate America continues chugging along.

If you're a regular consumer of the news, you may notice it seems more bleak than usual.[i] Fears about crashes, banking woes and the global economy overall dominate. That, coupled with sharp volatility, can test the patience of even the most disciplined investors. But to borrow a message from a presidential hopeful,[ii] perhaps we can shed some light in an overall dour and pessimistic environment: Despite all the hubbub, Corporate America continues besting low expectations. Now, growth isn't uniformly gangbusters, but the focus on the well-known struggles of a handful of sectors overlooks how the majority are doing-a sign of how dour sentiment is.

As of February 10, 345 S&P 500 companies have reported their Q4 2015 numbers. Earnings growth is -3.8% y/y while revenue growth is -3.7% y/y.[iii] Those figures may seem bad at surface level, but consider how they stack up on a relative basis. Just a couple weeks ago, with 200 companies reporting, earnings were down -5.8% y/y, revenues -3.5% y/y.[iv] Earnings improved by two whole percentage points while revenues were a smidge lower. And compare that to Q4 expectations at the reporting period's onset, when estimates had earnings growth at -4.4% y/y and revenues growth at -3.0% y/y.[v] Obviously, though, on an absolute level, both are still negative and revenues have dipped a bit more than initially expected, prompting murmurs about the "r" word.[vi] But here is the real kicker: the headline figures don't tell the whole story.

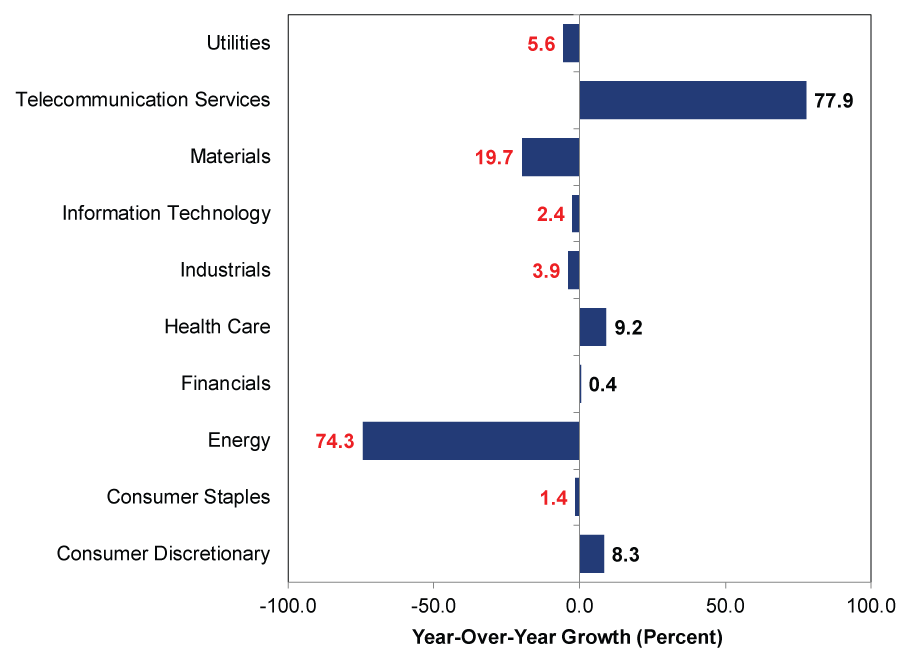

Overall corporate earnings reflect the struggles primarily of one sector-and its struggles are no surprise. As we have often written, the Energy sector has been slammed as ultra-low oil prices whacked revenues (which more price-sensitive than volume-sensitive). In Q4, Energy's earnings have plunged -74.3% y/y, while revenues have dropped -34.6% y/y. Here is a chart showing how much Energy's performance stands out relative to the other sectors. (Exhibit 1) Even Materials, which has faced some of the same headwinds as Energy, has not been hit as hard.

Exhibit 1: Q4 2015 Earnings Growth by Sector

Source: FactSet, as of 2/10/2016.

One note: The Telecom sector only has five companies (and only three have reported thus far), so outsized performance by a single company can produce huge skew. In this case, one company contributed 51.3 percentage points to Telecom's headline number in Q4-removing it would reduce the earnings growth rate to 26.6%. Compare that to the larger Energy sector, where 22 out of 40 companies have reported, constituting that -74.3% drop.

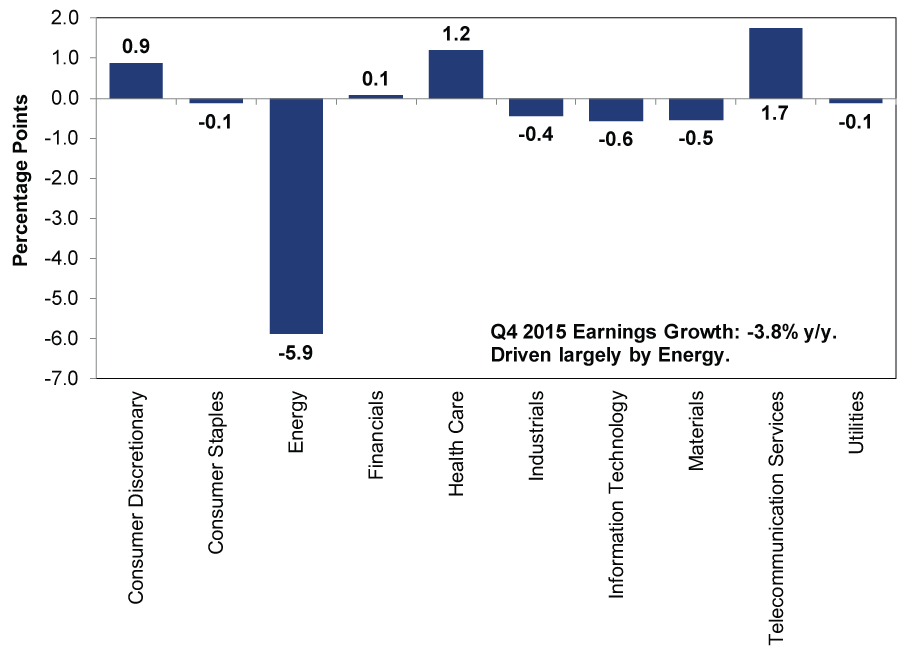

Here is another chart showing how the 10 different sectors have thus far contributed to/detracted from earnings growth thus far:

Exhibit 2: Q4 2015 Earnings Growth by Sector Contribution

Source: FactSet, as of 2/10/2016.

In other words, if you exclude Energy, earnings grew by 2.1% y/y. Similarly, revenue growth rose by 0.5% y/y after stripping away Energy's drag.

Now, we aren't arguing that sans Energy, growth is gangbusters-soft patches certainly exist. Despite its outsized positive contribution, there are Telecom's aforementioned caveats. Also, two of the biggest sectors are also struggling a bit. Info Tech earnings are down -2.4% y/y, and Financials are flattish. However, a handful of outliers-rather than broad-based sector weakness-explains that performance. In Financials, removing two companies-one facing a one-time settlement payment that knocked earnings-would boost sector earnings growth to 1.4% y/y from 0.7%. This is similar to Info Tech, as a handful of companies have weighed down headline growth. The larger point: these two sectors, which comprise almost 36% of the S&P 500, aren't broadly falling off. And earnings for other significant sectors-like Health Care (9.2% y/y) and Consumer Discretionary (8.3% y/y)-are growing nicely. So even though growth isn't uniform across all sectors, the private sector isn't flagging. The strong can pull along the laggards, so even slower earnings growth can mean a pleasant surprise for investors expecting recession.

We expect the US' private sector to continue plowing ahead, driving growth this year. As has been the case repeatedly through this expansion, we believe widespread dour investor sentiment is disconnected from reality. Remember 2010's double dip? 2011's euro-led global recession? 2012's? Folks have frequently feared economic data variability meant recession loomed. Yet consumer spending has risen throughout this expansion. Money supply is growing, as lending has accelerated since the Fed ended its quantitative easing bond purchases. Inflation, excluding the aforementioned weak Energy prices, is benign. Businesses have oodles of cash, and they are investing. Banks are better capitalized in most of the world. Point being, the foundation is in place for US firms' profits to grow, outside Energy. However, it seems to us many incorrectly equate the woes confronting commodity businesses like Energy weakness with the broader economy, setting up a low bar for reality to beat. Once investors realize growth is better than appreciated, we believe sentiment can finally turn to optimism-a reason to be bullish today.

[i] And that's saying something!

[ii] Full disclosure: We do not endorse any political candidate, as we favor no candidate or party and assess politics solely to analyze how it may impact markets (and to drop in the occasional joke). We believe political bias is blinding and dangerous for investors.

[iii] Source: FactSet, as of 2/10/2016.

[iv] Source: FactSet Earnings Insight for the Week Ending January 29, 2016.

[v] Source: FactSet Earnings Insight for the week Ending December 11, 2015.

[vi] The economic term that must not be named. Or recession. Oops.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Interesting Market History Six Years On, Lessons From the COVID-Lockdown Low Endure2026-03-25

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

-

Market Analysis The Golden Paradox2026-03-24

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today