Personal Wealth Management / Market Analysis

P/Es Are Above Average and That’s OK

Don't read too much into recent Fed comments about overheating stocks.

For years, folks have feared stocks are too expensive. Such worries seem ever-present, but they get renewed attention when various financial luminaries add their own warnings. Last week, for example, multiple Fed members commented on asset prices, using phrases like "somewhat rich," "running very much on fumes" and "close monitoring is warranted." Sounds worrying! But valuations alone don't predict market direction. They are merely a sign of where sentiment is now: warming, but not close to euphoric.

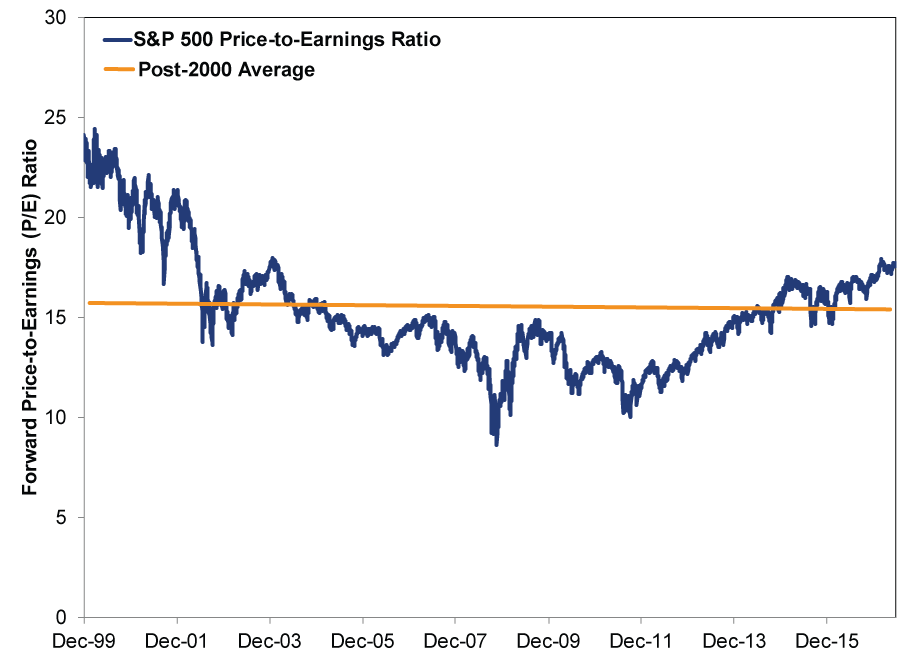

The S&P 500 forward 12-month price-to-earnings ratio (which compares current stock prices to forecasted earnings) is above its post-2000 average-but only just! It stands at 17.6 today versus the post-2000 average of 15.4.[i] This is pretty unremarkable and not a sharp break from the recent past, either: the forward P/E first breached 17 on February 24, 2015 and has averaged 16.5 since.[ii] US stocks returned 21.3% over that time-gains that folks freaked out by "too high" valuations missed.[iii]

Exhibit 1: S&P 500 Valuations' Mild Rise

Source: FactSet, as of 6/23/2017. S&P 500 12-Month Forward P/E Ratio, 12/31/1999 - 6/23/2017.

If P/Es have been so boring recently, why all the attention? Chatty central bankers, that's why. In recent interviews, Fed members purportedly talked up "frothy asset prices" and "watching for bubble trouble." Chair Janet Yellen caused quite the stir during a Q&A at the British Academy in London:

"The so-called equilibrium rate of interest, not just in the United States but globally, looks like it may stay low for a long time. But there's a lot of uncertainty around that. Now, asset valuations are somewhat rich if you use some traditional metrics like price-earnings ratios, but I wouldn't try to comment on appropriate valuations and those ratios would depend on long-term interest rates, and, you know, of course there's uncertainty about that. So yes, by standard metrics some asset valuations look high, but there's no certainty about that." (Emphasis ours.)

You might notice[iv] Yellen repeating her uncertainty three times in as many sentences, which sounds to us like she really didn't want folks to take her comments as an authoritative declaration P/Es are too high. Yet headlines did just that:

- "Yellen Fed Ramps Up Attention Over 'Somewhat Rich' Asset Prices"

- "Don't Ignore Yellen's Valuation Warning"

- "Rich Valuations Get Richer as Yellen's Words Fall on Deaf Ears"

But Yellen isn't a valuations Cassandra who is warning heedless investors of expensive markets. This was a tentative and carefully hedged observation. The notion stocks might be a tad pricey isn't a shocking discovery either. Headlines have blared about high P/Es for years, giving markets ample opportunity to price in this worry. The Fed itself has contributed to this too: March Fed meeting minutes noted that "some participants viewed equity prices as quite high relative to standard valuation measures." Surprises move markets, not long-running and widely publicized fears amplified by prominent policymakers.

More importantly for investors, above-average valuations don't bode ill for markets because P/Es aren't predictive. At best, the forward P/E is a snapshot of sentiment, not a market timing tool.[v] "Expensive" markets can get more expensive-sometimes for years-as markets keep gaining. And because markets don't mean revert, long-term averages don't exert a gravitational pull, so stocks are never "due" to return to a certain valuation level. Moreover, history shows Fed members citing higher P/Es isn't necessarily telling, either. One of the most prominent examples: when former Fed chair Alan Greenspan famously chalked up buoyant markets to "irrational exuberance" in December 1996. Yet that 1990s bull market continued for more than three years and US stocks more than doubled. Heeding a Fed member's valuation prognosis then was costly for investors.

And for all the warnings that valuation levels portend ill for stocks, the data don't back that claim up. Consider some recent global bull market corrections-steep, sentiment-fueled declines of -10% or more.[vi] During 2010's April - July correction, global stocks fell -16.7% as the MSCI World forward P/E slid from 14.0 to 11.2. In 2011's steep summertime pullback, the MSCI World dropped -22.8% and the P/E went from 12.0 to 9.7, while 2012's correction saw a -13.2% slip and a P/E down to 10.6 from 12.3. Heck, we can even go back to 2006's correction, when global stocks fell -11.5% and the P/E followed it down from 14.9 to 13.1. Our point: None of these sharp market pullbacks saw valuations above their long-term historical average (15.0 for the MSCI World since 2000). Thus, if low valuations didn't equate to calm markets, we fail to see how rising valuations foreshadow greater negative volatility.

This also holds up for bear markets-longer, fundamentally driven declines of -20% or more. Both the MSCI World and S&P 500's forward P/E ratios hovered around their long-term historical averages right before the 2007-2009 bear market started. Why? Because the preceding bull didn't die from euphoria. Instead, it was caused by an unexpected wallop, driven by $2 trillion in unnecessary writedowns banks had to take and the government's haphazard handling of the fallout. Juxtapose that with the 2000-2002 bear market, when P/Es rapidly climbed to the mid-20s range right before the Tech bubble popped. Yet at the time, many investors were blinded by greed and promises of the "new economy," where clicks mattered more than cash and few noticed or cared about deteriorating fundamentals.

These examples illustrate when P/Es are most meaningful: when they're surging, few notice and those who worry are roundly mocked. This extreme disconnect between sentiment and reality can help show a bull's days are numbered. Today, we don't see such a big disconnect. Gradually rising valuations show investors are increasingly warming to an eight year-old expansion, typical in a maturing bull market. Myriad headlines, meanwhile, keep fretting allegedly expensive stocks-another sign euphoria is nowhere in sight.

Today, firms globally are doing well. US earnings growth hit 14% in Q1, the fastest pace since 2014. Analysts expect slower but still nicely positive profit growth in Q2. Against this backdrop, barely above average valuations aren't very concerning. Another reason for globally minded investors to be positive: Forward eurozone P/Es are lower relative to the US at 14.2,[vii] suggesting they have more room to climb. With sentiment toward the Continent still in the nascent stages of optimism-and plenty of reasons to be optimistic about Europe in the near term-we believe eurozone stocks are set to do well for the rest of this year.

[i] Source: FactSet, as of 6/26/2017.

[ii] Ibid. S&P 500 daily average 12-month forward P/E, 2/24/2015 - 6/28/2017.

[iii] Source: FactSet, as of 6/29/2017. S&P 500 total return, 2/24/2015 - 6/28/2017.

[iv] Partly because of that helpful emphasis we added.

[v] And don't get us started about how folks use other valuation metrics (like the strangely inflation-adjusted CAPE)!

[vi] For the rest of the data in this paragraph, source: FactSet, as of 10/3/2016. Stock returns are the MSCI World Price Returns, valuations are the MSCI World 12-month forward P/E.

[vii] Source: FactSet, as of 7/3/2017. MSCI European Economic and Monetary Union daily average 12-month forward P/E.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today