Personal Wealth Management / Politics

Previewing the 116th Congress

A divided legislature likely paves the way for traditional interparty gridlock—historically beneficial for stocks.

Editors’ note: Our political analysis is intended to be nonpartisan and focuses exclusively on political developments’ potential market impact. We favor no party, politician or ideology and believe political biases cause investing errors.

Last Thursday at noon Eastern, 10 newly minted senators and 101 new representatives were sworn in alongside their returning compatriots, officially kicking off a new Congressional session. Democrats took control of the House, while Republicans slightly increased their Senate edge. This is the classic recipe for gridlock—unpopular with many voters but positive for stocks, in our view. As the two parties butt heads and do little of substance, we expect markets to benefit.

Congressional gridlock isn’t new. Even with control of the House, Senate and presidency for the previous two years, Republicans didn’t pass much, as internal disagreements and their tiny Senate majority proved big obstacles—intraparty gridlock. Just a couple Republican defections could—and did—scuttle bills. The highest profile signed legislation was 2017’s tax reform—and even that wasn’t as sweeping as supporters and detractors portrayed. It also got watered down during passage. Heck, the 115th Congress closed amid a partial government shutdown—the third in a year—as the GOP didn’t have sufficient votes to overcome a partisan divide on border wall funding.

Post-midterms, gridlock comes in a more traditional form: Republicans hold a six-seat Senate advantage (that counts independents Bernie Sanders and Angus King as Democrats, based on their voting histories), while Democrats enjoy a 36-seat margin in the House. It is difficult to envision this split Congress uniting on landmark legislation. Even in less rancorous times, getting a divided legislature to agree on significant reforms is a tall order. Republican-sponsored Senate bills likely find a cold reception in the Democratic House and vice versa. President Trump can also veto.

In our view, current signs point to more acrimony and division, not harmony and compromise. Exhibit A: The partial shutdown, which continues with no end in sight. While not a material negative for the economy or markets, it indicates this new flavor of gridlock looks pretty similar to the old. Second, House Democrats could prepare a raft of investigations of the Executive branch, which doesn’t strike us as a prelude to bipartisan kumbaya. It also distracts from legislating: Hearings take time and drain political capital.

The 2020 presidential election is another distraction—even now, 22 months out. One prominent Democratic senator, Massachusetts’ Elizabeth Warren, has already announced an exploratory committee—and many others are rumored to be considering a run. A pair of partially overlapping CNN tallies—one in December,[i] one in January[ii]—included 12 potential candidates. The Hill put out a top-10 ranking, with 10 additional possibilities thrown in for good measure.[iii] The Washington Post cited 16 potential hopefuls from Congress alone.[iv] This affects doings on Capitol Hill because candidates tend to focus on publicity and broad statements of principle rather than putting their names on potentially controversial legislation. The latter could alienate centrist voters—too risky! Besides, legislating leaves fewer issues to campaign and fundraise on.

This applies to presidents seeking reelection, too. Incumbents know their political capital is higher in their first two years in office, so that is when they usually try to cram in bold policy agendas. In their term’s second half, attention usually shifts to campaigning, fundraising and avoiding unnecessary electoral risks.

All these factors foster political inaction, which stocks typically prefer. Major legislation creates winners and losers by redrawing property rights—and given people’s tendency to fear losses more than they appreciate gains, the losers’ distress usually knocks sentiment. Even winners often fret what might change next. Gridlock mitigates this risk by keeping the rules of the game roughly stable, rendering planning easier and business investment more attractive. Importantly, few notice this upside, boosting its surprise power.

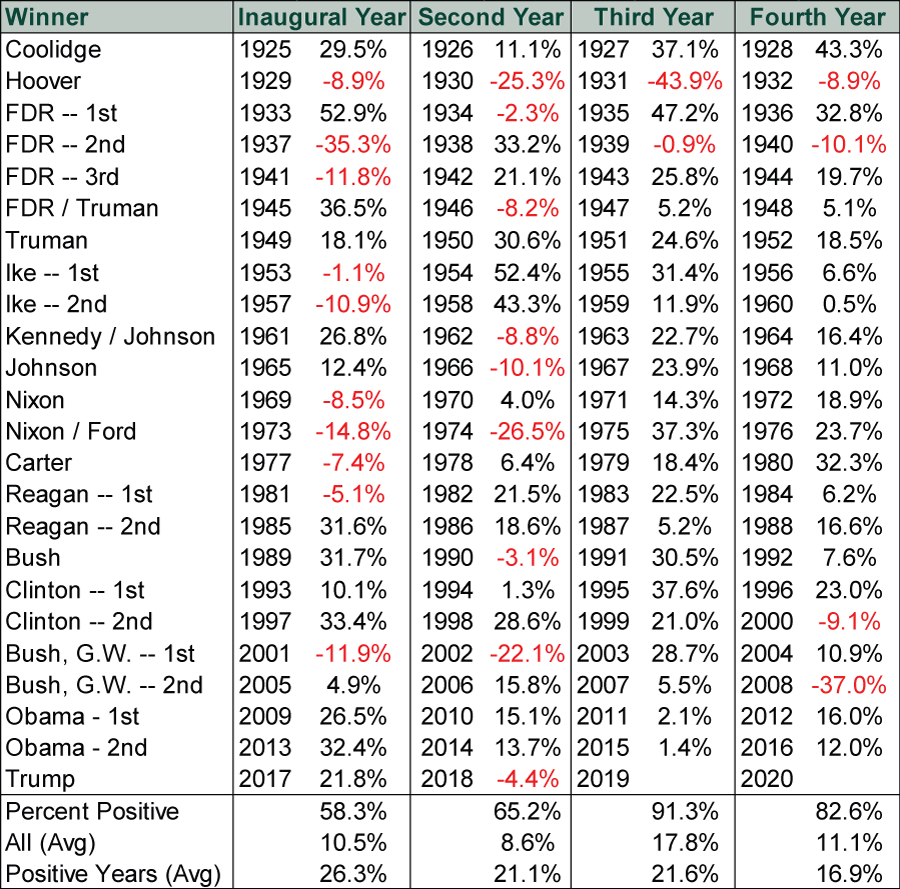

As last year shows, gridlock isn’t an automatic balm for market volatility. Politics are just one market driver, and dour sentiment can overwhelm positive fundamentals in the near term. That said, taking a longer view shows gridlock’s benefits. The third year of the presidential cycle—after midterms have boosted gridlock and candidates have begun eyeing the next election—has the highest frequency of positive returns and the highest average return. As Exhibit 1 shows, the only two negative third years came during the Great Depression and the dawn of WWII. This pattern may not hold in 2019, but we don’t discount the probability.

Exhibit 1: Returns in Presidential Third Years

Source: Global Financial Data, Inc. and FactSet, as of 1/7/2019. S&P 500 Total Return Index, 1/1/1926 – 12/31/2018.

While presidential third years aren’t necessarily super positive, their appeal is primarily about direction, not size—and direction matters more because it informs whether staying in stocks is wise. Absent material changes to your long-term goals or needs, we believe it is. Recent volatility has understandably rattled nerves, and it is impossible to say whether we have seen the last of it. But we think it is worth noting this stage of the political cycle has historically been kind to US stocks. Recognizing positives others miss—such as gridlock—can help you avoid reacting to panicked headlines and stay focused on what lies ahead. With global economic and political fundamentals mostly benign and pessimism abundant, we think a rebound is most likely.

[i] “Democrats are making moves behind the scenes to gear up for 2020,” Dan Merica and Arlette Saenz, CNN, 12/6/2018.

[ii] “Democrats are getting ready to run in 2020. Who has the money advantage?” Fredreka Schouten, CNN, 1/2/2019.

[iii] “The Top Ten Democrats for 2020,” Niall Stanage, The Hill, 1/1/2019.

[iv] “An ‘unprecedented’ number of Democrats in Congress want to be president,” Colby Itkowitz, The Washington Post, 12/7/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Expert says investors are ignoring a massive global rally2026-06-22

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US PCE Inflation, Annuities

2026-06-22

2026-06-22 -

Politics Revolving Door Turns, Uncertainty Starts Falling2026-06-22

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 15 - June 192026-06-22

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today