Personal Wealth Management / Market Analysis

Random Musings on Markets Episode VII: The Footnotes Awaken

A chain-chain-chain of musings on political bias, an avocado caper, central banking shenanigans and more!

In this week’s surely-not-weekly roundup of random market news, a survey shows Americans are really politicized (duh), Kiwi avocado theft shows the perils of market restrictions, the BoJ swallows Japan, the UK’s real wages may or may not be falling, Karl Marx’s 200th birthday party in Germany proves capitalism’s superiority, and we bid sad farewell to a Queen.

Survey Says Americans Are Too Political

As folks who spend a considerable amount of our workweek reading and analyzing financial media, we are often asked, “Who can you trust? What sources are reliable???” An Ipsos survey published August 7 answered that resoundingly with, “The Weather Channel.”[i] The poll showed the home of reporters getting battered by gale-force winds scored the highest favorability rating and trustworthiness rating of 33 news outlets (including, oddly, Barack Obama and Donald Trump). It was the only outlet 80% of respondents in all three categories—Republicans, Independents and Democrats—held a favorable view of. TWC was also the only media outlet over 90% of respondents in all three categories said they find trustworthy.[ii] Maybe folks just love to Wake Up With Al [Roker]. Or maybe it is something else. Like, we don’t know, the fact the Weather Channel doesn’t do politics?

You see, Ipsos also found American’s trust in media has dropped 30 percentage points since the late 1970s, and there is a significant and growing partisan divide regarding faith in—and protections for—media. For example, while 68% of Democrat respondents agreed that “Most news outlets try their best to produce honest reporting,” only 29% of Republicans concurred. And if you look at the opinion by media outlet, it further breaks down along party lines—which echoes something we have long argued ’round here: Much of news media today is entertainment. If you don’t like the coverage on one channel, they aren’t targeting you.

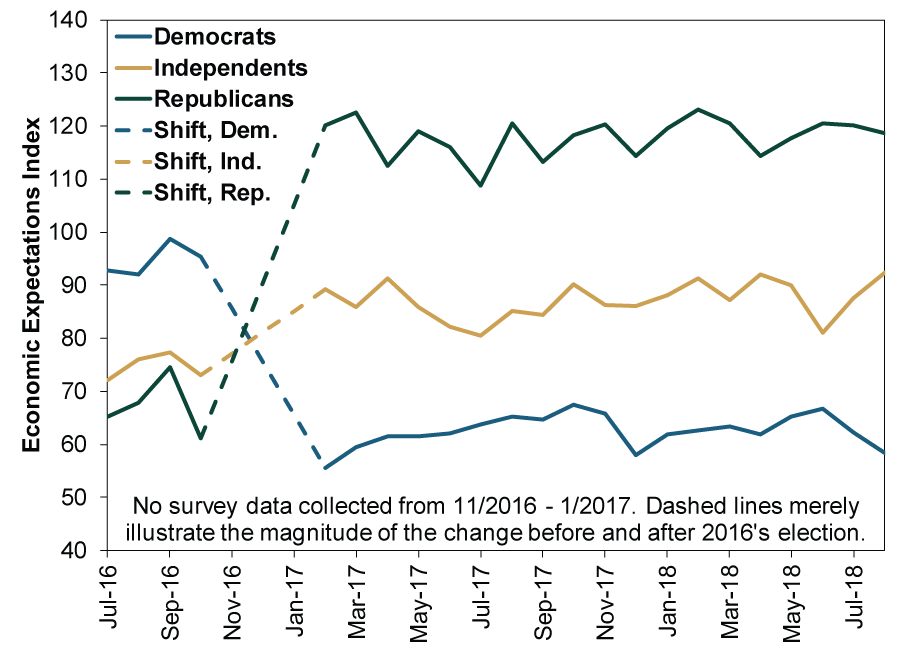

This survey echoes another one, conducted by the University of Michigan. On occasion, U-Mich researchers have asked respondents their political affiliation as part of their Consumer Sentiment Survey. This has been very irregular historically, but the Wolverines seem to have changed tack starting in February 2017—they have asked every month since. Of interest to us here is the subcomponent tracking folks’ expectations. In Friday’s report, Republicans’ expectations hit 118.7, suggesting strong optimism. Democrats’ were over 60 points lower, at 58.3. That is pessimistic! On par with readings in the fall of 2008!

As Exhibit 1 shows, economic expectations appear to be heavily influenced by political party affiliation. Note the huge flip around the election, when Republicans suddenly became more optimistic—and Democrats more pessimistic. (Sadly, we can’t compare to past elections, as regular data don’t exist.)

Exhibit 1: Partisan Politics Drive Economic Expectations (Wrongly!)

Source: University of Michigan, as of 8/17/2018. Survey of Consumers, Economic Expectations by Political Affiliation, July 2016 – October 2016 and February 2017 – August 2018.

This highlights what we think is a key investor risk these days: Falling prey to partisanship in your investment outlook. If you let political views infect your sense of where the economy is heading, it stands to reason you may do so with investments, too—after all, markets are forward-looking economic indicators. This is an area rife with bias! If you suddenly became bullish or bearish when Donald Trump won 2016’s vote, there is a strong chance your emotions will betray you later.

Avocadon’t Steal, Please

If we could travel the world and teach governments basic economics, lesson three would be this: Artificial scarcity creates black markets and rampant crime. We would tell colorful stories about John Dillinger[iii] and Prohibition-era outposts like Drawbridge, the San Francisco Bay Area’s ghost town. We would highlight the perils of drug mules. And then to lighten the mood, we would talk about Auckland, New Zealand’s seedy underbelly of avocado crime.

To Americans, the avocado is the luscious fruit that millennials spread on toast instead of saving money to buy houses.[iv] To Kiwis, the avocado is a scarce, expensive delight that must be kept behind razor wire so that no one steals it. While avocados are abundant for most of the world, New Zealand’s strict food laws prevent avocado imports. Folks there must make do with locally grown fruit. And because New Zealand is a hop, skip and a jump away from avocado toast’s birthplace, Australia, avocados are in sky-high demand and currently selling for $3.30 a pop—a 37% year-over-year rise, according to The New York Times.[v] The obvious solution is to grow your own, but that is easier said than done when garden centers are sold out and have long waiting lists.

Where enterprise isn’t an option, criminal enterprise usually results. And so it is with avocados. Criminals have started robbing orchards and suburban growers alike and selling their booty on the black market. In one particularly amusing tale, some allegedly “older” gentlemen stripped hundreds of avocados off one suburban tree and hightailed it in their getaway vehicle of choice: a mobility scooter.[vi] As one police officer noted, convicting the thieves is difficult because it generally takes a few weeks to track them down: “The evidence would be well and truly devoured by then.” To battle the thieves, homeowners have started installing fancy security systems and fencing off trees with barbed wire—an example of well-intended laws causing otherwise unnecessary expense if ever there was one.

So the next time you hear new regulatory rumblings from Congress, and you wonder about the potential market impact, remember the avocados. Think about whether anything lawmakers propose will force business owners to buy some proverbial razor wire or security cameras in order to withstand its effects.

This Week in Central Bloating

A couple weeks ago we joked that the Bank of Japan had assumed Japan Post’s old honorary title of “The Bank That Ate Japan.” If it wasn’t official then, it surely is now: The BoJ’s assets officially exceed Japanese GDP. Yes, you read that right. After nearly eight years of the world’s largest quantitative easing (QE) program, the BoJ has about ¥548.94 trillion in assets on its balance sheet. That tops Japan’s 2017 nominal GDP, ¥546 trillion.

Now, comparing a level (total assets) with a flow of economic activity (GDP) is flawed, as we mused here recently. It is always cleaner to keep like with like—hence why, when scaling Japan’s QE Monday, we compared annual asset purchases to GDP instead. But let us have some fun anyway. Thus far, the ECB has bought only about €2.5 trillion in assets, far below its 2017 GDP, €11.2 trillion.[vii] At its peak, the Fed owned about $4.5 trillion in assets—well below US GDP for 2017, about $19.5 trillion.[viii] This speaks volumes about how long the BoJ has been gobbling up assets. It presently owns nearly half of all Japanese government bonds in existence, and Japan happens to have the world’s second-largest bond market. Sometimes, days go by without a single Japanese bond changing hands. The nerdier one of us imagines the Japanese bond market as a big empty videogame arcade with one kid in the corner playing Teenage Mutant Ninja Turtles alone because the kid hoarded all the tokens.[ix]

Back to the original metaphor, we suspect Japanese markets and investors will be much happier once the BoJ stops eating all the bonds and starts, umm, releasing them. Bond markets will have more supply. Banks won’t have to deal with a market meddler. Things will look more normal. Life will be good.

What Most Folks Miss About “Falling” Real Wages

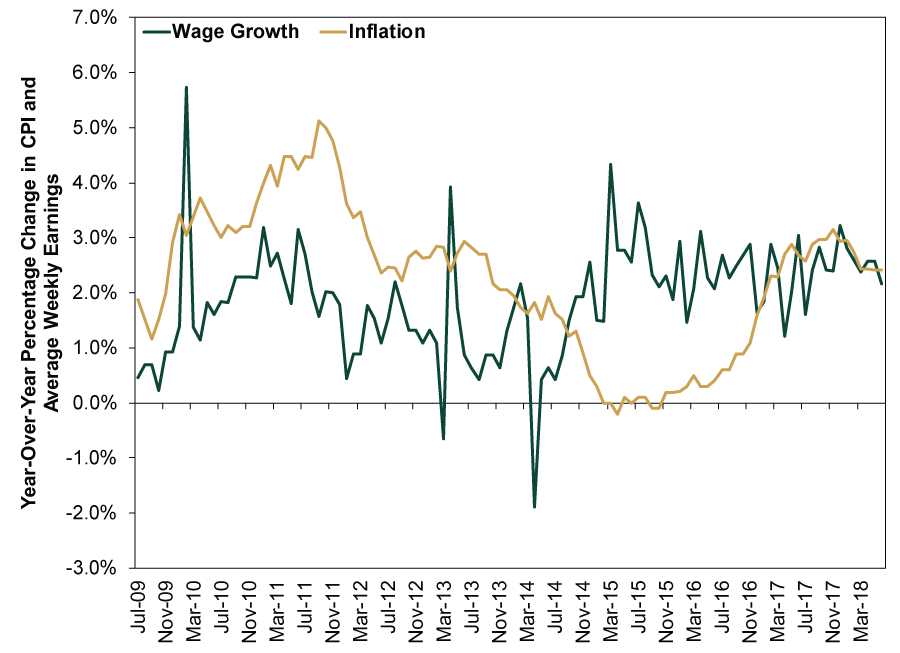

With the news that UK wage growth averaged 2.4% y/y in the three months through June and CPI inflation hit 2.4% y/y in June, worries of flat and potentially falling “real” wage growth returned—echoing similar fears in the US. The logic is simple: 2.4% nominal wage growth minus 2.4% inflation = zero. No growth. And bad news for a country where real wages fell for much of 2009 – 2014.

The trouble with this argument is that it presumes household finances during this expansion look like this:

Exhibit 2: UK Wage Growth and Consumer Price Index, Year-Over-Year % Change

Source: Office for National Statistics, as of 8/16/2018. Year-over-year percentage change in Consumer Price Index (all items) and average total weekly earnings of private-sector employees, July 2009 – June 2018.

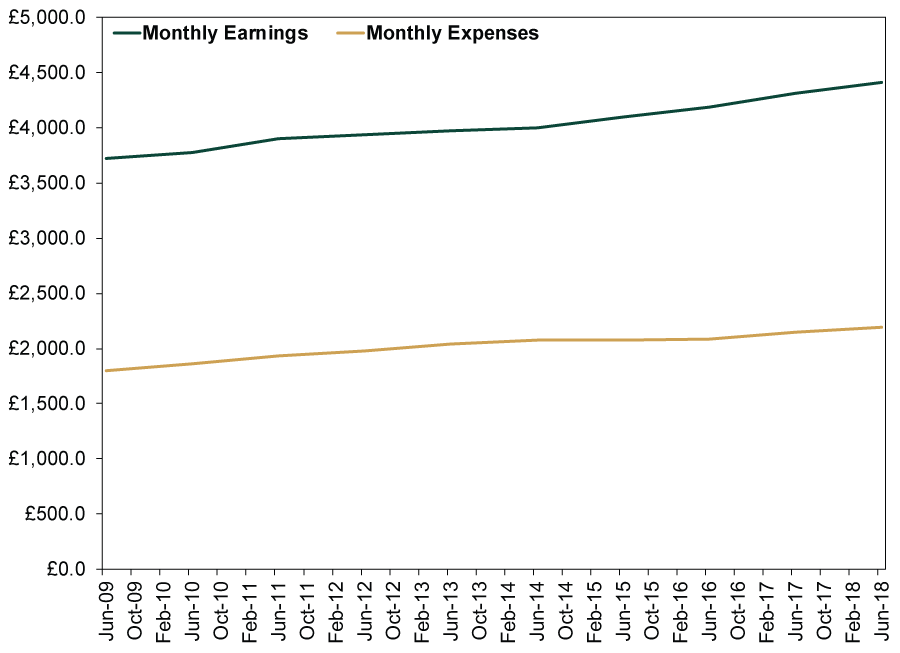

But that isn’t real life! Even if a person’s earnings and household expenses rose at the exact average rates, they likely would not find inflation repeatedly eroding all of their pay gains. While inflation’s rate of increase might exceed the rate of pay increases, that doesn’t mean the actual rise in earnings, measured in pounds, is below their actual rise in living expenses. According to a 2010 ONS report, average weekly expenses for an average city dweller were about £450, while their average weekly pay was about £930. Multiply each by four, and we get average monthly expenses of £1,800 and pay of £3,720 when this expansion began in mid-2009. Apply average wage growth and inflation each June (once a year suffices since these are year-over-year growth rates), and you get this:

Exhibit 2: UK Monthly Earnings and Expenses

Source: Office for National Statistics, as of 8/16/2018. Based on year-over-year percentage change in Consumer Price Index (all items) and average total weekly earnings of private-sector employees, July 2009 – June 2018. Starting values come from “Family Spending 2010 Edition: A Report on the Living Costs and Food Survey 2009,” published by the ONS on 11/13/2012.

Earnings grew more than expenses! Even though their growth rate frequently lagged, because they were growing off a higher base, the increase in pounds was bigger. Start to finish, our hypothetically very average Brit’s monthly expenses rose from £1,800 to £2,196, but their monthly pay jumped from £3,720 to £4,410. That means, over the course of these nine years, their monthly savings rose from £1,920 to £2,213. That, dear readers, is how consumer spending could keep driving the UK’s expansion without destroying household finances. And, it is why another lull in official measures of real wages shouldn’t be a threat.

Capitalism Wins!

In a delightful development that may have Communist Manifesto author Karl Marx rolling in his grave, his hometown of Trier, Germany is proving the capitalist maxim that there is a market in everything. You see, this May 5 marked Marx’s 200th birthday. To “celebrate,” Trier is selling a slew of somewhat kitschy knick-knacks akin to what you might find in a typical American tourist trap. Mugs, stickers, magnets, pens. We imagine small-business folks hawking t-shirts saying, “My parents went to Marx’s 200th birthday party and all I got was this lousy t-shirt.”

But it seems the most popular knick-knack is a curious €0 bill featuring Marx’s likeness on purple, euro-like security paper including security features reminiscent of real currency. As Deutsche Welle reported this week, for the privilege of owning this €0 bill featuring the father of communist theory, you will pay €3. Seems like a fat profit margin! Anyway, these bills are apparently very popular, with more than 100,000 selling this year. Ironically, it seems they are particularly popular in China.

Keep that in mind when you find coverage of socialism’s allegedly rising popularity, like those that followed Gallup’s poll Monday.[x] People may say they don’t like capitalism, but their actions seem to show they sure enjoy practicing it. As ever, we think actions speak louder than words, implying the Revolution isn’t close to wiping out your portfolio.

Remembering and R-E-S-P-E-C-T-ing Royalty

Thursday was the best of times and the worst of times. To celebrate the 50th anniversary of Elvis Presley’s 1968 televised concert—aka the legendary ’68 Comeback Special—movie theatres nationwide held special screenings of what your friendly Musers consider the greatest concert video of all time[xi] (if you missed it, fear not—they’re doing it again Monday). But alongside this joyous celebration of the King came a wave of sadness with the news the Queen of Soul, Aretha Franklin, passed away the same day. We hope everyone will symbolically join us in popping “Chain of Fools” or “(You Make Me Feel Like) A Natural Woman” on the turntable, cranking the volume to 11 and lifting a glass to this great lady. If we may borrow from Shakespeare:

She was a lady. Take her for all in all.

We shall not look upon her like again.[xii]

Enjoy your weekend!

[i] “Americans’ Views on the Media,” Ipsos, August 7, 2018. https://www.ipsos.com/en-us/news-polls/americans-views-media-2018-08-07. Not to editorialize, but this also strikes us as really odd. We mean, it’s sort of a cliché that weathermen have the easiest job in the world, as they never have to be right.

[ii] Of course, this poll was conducted during the summer. Who knows how the weather may influence this! Perhaps their rank would plummet when a forecasted winter storm misses estimates big time?

[iii] No relation to Elisabeth. We think.

[iv] Disclosure: It would take more than giving up avocado toast for anyone to save for a down payment.

[v] Avocado prices denominated in US dollars. In Kiwi terms, they are running more like $5.06, per Statistics NZ. Currency fluctuations between the US and Kiwi dollars may impact the avocado return on your investment.

[vi] Where are Jack Lemmon and Walter Matthau when we need them?

[vii] Source: ECB and FactSet, as of 8/16/2018.

[viii] Source: St. Louis Federal Reserve and US Bureau of Economic Analysis, as of 8/16/2018.

[ix] The other of us hates analogies only slightly more than the nerdier one and threatened to delete this sentence but accepted an endnote objection as a compromise.

[x] Yes, yes, we know: Many argue socialism and communism are different and folks frequently characterize socialism in vastly different ways than the traditional definition. Anyway, we aren’t wading into that heavy philosophical territory here. This is Random Musings, not Deep Thoughts.

[xi] Ok, other than This Is Spinal Tap.

[xii] Paraphrasing Hamlet, Act I, Scene II.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today