Personal Wealth Management / Market Analysis

Reasons for Gratitude in a Challenging Year

Some positives to keep in mind this Thanksgiving.

To put it lightly, this has been a tough year. The global bear market has tested investors’ patience since February, and perhaps especially as a summertime rally gave way to new October lows. There is no shortage of things to fret, market-related or otherwise, and I don’t dismiss any of today’s problems or issues. But this week is a reminder, in my opinion, that things aren’t all bleak—there are some developments to be grateful for this Thanksgiving. Here are a few that leap to mind.

Europe’s Adaptation to the Feared Energy Crunch

After Russia’s invasion of Ukraine in February, many warned Western sanctions and Russian retaliation would drive oil prices to $200 a barrel—or even as high as $380 under a “worst-case” scenario—ensuring a eurozone recession in either case.[i] Yet after registering a year-to-date high of $133 on March 8, Brent crude prices have retreated (currently around $88) while eurozone GDP has grown through Q3.[ii]

Now, that doesn’t mean Europe will avoid recession. Soft patches have emerged, as soaring costs have forced some factories in Germany, the eurozone’s largest economy, to slash production and lay off workers.[iii] But there is also significant evidence the worst-case outcome isn’t coming to pass. Consider: The EU targeted an 80% filling level of gas storage sites by November 1. As of November 19, storage is at 95%.[iv] Some of it is luck—mild weather has kept energy use low—but people are also adapting.[v] The Continent has obtained some natural gas overseas, and households are participating in conservation efforts. Governments have also updated policies, targeting energy security. A new pipeline connecting central European nations like Poland to Norwegian gas suppliers is slated to come online prior to yearend—ahead of schedule. Germany’s nuclear plants—previously scheduled to go dark at yearend—will stay online for the foreseeable future, and the country opened its first liquefied natural gas (LNG) facility in just 194 days thanks in part to permitting exceptions. More LNG terminals are coming online across Europe in early 2023, helping further ease supply pressures. It seems to me like the seeds are sown for a better-than-feared outcome.

Travel Is Bouncing Back

I was in Los Angeles last weekend for some early Thanksgiving festivities, and I wasn’t alone—travel appears to be normalizing. Los Angeles International Airport officials expect more than 200,000 passengers daily from November 17 – 28—more than 20,000 passengers per day compared with the same period last year.[vi] On the roads, the American Automobile Association projects the Thanksgiving travel stretch to be the third-busiest ever.[vii] While nobody likes traffic, it speaks to a broader, little-noticed trend: a return to pre-pandemic norms. Remember November 2020 when government agencies discouraged travel—and recommended a two-week quarantine for those who did? Or what about when Omicron cooled some travel plans last year? After all that, you can see a silver lining to traffic on the Grapevine.[viii]

Other positive signs? According to global hospitality research outfit STR, US hotel occupancy was 0.9% higher in the week of November 6 – 12 versus the comparable week in 2019—even though the average daily rate for a room was 17.1% higher.[ix] Per the International Air Transport Association, September global air travel was up 57.0% y/y, and the month’s activity was close to 75% of September 2019 levels.[x] Up north, Canada lifted all cross-border travel limits, effective October 1, for the first time post-pandemic.

We aren’t back to normal yet, and some countries still have restrictions. But the fact people are both able and willing to brave the busy holiday travel season again to figure out who gets the turkey leg is worth being thankful for.

Other Reasons for Optimism

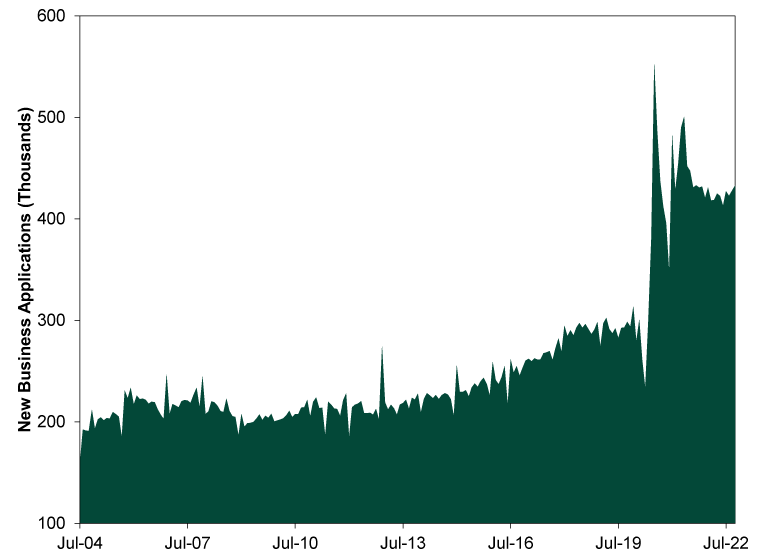

Two years ago, we wrote about the surge in new US business applications. That growth has continued into 2021 and this year, too. (Exhibit 1)

Exhibit 1: New Business Applications, July 2004 – October 2022

Source: US Census Bureau, as of 11/22/2022. Total New Business Applications, seasonally adjusted, monthly, July 2004 – October 2022.

Now, applications don’t mean a huge boost to GDP growth in the near term or even long term. It isn’t easy running a business: Of those that launched in March 2020, about 15% failed before March 2021.[xi] Going back to when data collection began, of the businesses that opened in March 1994, just 14% were still around this year.[xii] But the fact individuals remain eager and willing to chase their dreams despite regularly long odds—and all the tumult wrought by a once-in-a-century pandemic—speaks to the resilience of the American entrepreneurial spirit.

Another non-market driver but interesting long-term development: The global population recently hit 8 billion per UN projections.[xiii] Naturally, most focused on the negatives. Do we have too many people for the earth to handle? Or does slowing population growth set the stage for an “underpopulation bomb” that will sap the global economy of innovation and youthful energy?

But around the world, life expectancies are up over the longer term and poverty and famine are down. There are, of course, temporary setbacks that affect the quality of life. But if a growing population hasn’t caused calamity yet, we doubt it does now. And what of the unasked question: What about the positives? The world also has 8 billion people capable of devising creative ways to harness technology to address tomorrow’s issues.

A simple way to see this last point: 3D printing. The technology has been around since the 1980s, but it received a lot of buzz in the early 2010s after some companies took it mainstream and introduced do-it-yourself kits. Many investors thought the industry would print money, which seemed a tad overstated. No, 3D printing hasn’t proven to be The Next Big Thing, but it is having a positive imprint on everyday life. 3D printers can make athletic shoes, prosthetics and mouth guards—like the one I picked up from my dentist recently. We don’t know how today’s individuals and businesses will meet future problems. But I am optimistic humanity will be up for the challenge—just as it has always been.

Now, don’t get my optimism twisted: I am not ignoring the world’s problems. War is ongoing in Ukraine and elsewhere. That is tragic. Elevated inflation means economic hardship for many. There are also way too many senseless acts of violence that forever alter victims’ lives, as well as their families and local communities. The world isn’t a perfect place. Nor will it ever be. But I think it is a mistake to let the negatives obscure the positives, especially now. In my view, that is worth reflecting on this Thanksgiving week.

[i] “JPMorgan Sees ‘Stratospheric’ $380 Oil on Worst-Case Russian Cut,” Joe Carroll, Bloomberg, 7/1/2022.

[ii] Source: FactSet, as of 11/22/2022. Statement based on Crude Oil Brent Global Spot Price on 3/8/2022 and 11/22/2022 and eurozone GDP, quarterly growth rate, Q1 2022 – Q3 2022.

[iii] “Rocketing Energy Costs Are Savaging German Industry,” Anna Cooban, CNN Business, 10/28/2022.

[iv] “95.0% of EU Gas Storage Is Filled,” Staff, Reuters, 11/19/2022.

[v] “Europe Predicts Milder Winter, a Boost for Its Energy Security,” Yusuf Khan, The Wall Street Journal, 11/14/2022.

[vi] Source: Twitter, as of 11/23/2022. Tweet from @flyLAXairport, posted at 7:30am on 11/16/2022.

[vii] “LAX Holiday Travel Is Underway With Mornings Expected to Be the Busiest,” Staff, CBS Los Angeles, 11/21/2022.

[viii] You have to look really hard, but it’s there.

[ix] “STR: U.S. Hotel Results for Week Ending 12 November,” STR, 11/17/2022.

[x] “September Passenger Demand Stays Strong,” International Air Transport Association, 11/7/2022.

[xi] Source: BLS, as of 11/22/2022.

[xii] Ibid.

[xiii] “Are 8 Billion People Too Many — Or Too Few?” Bryan Walsh, Vox, 11/21/2022.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Excess Fear Over ‘Excess’ Profits2026-06-25

-

In The News What ‘IPO’ really stands for — and whether you should be buying SpaceX and the AI giants2026-06-23

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-23

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US PCE Inflation, Annuities

2026-06-22

2026-06-22

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today