Personal Wealth Management / Market Analysis

Reports of Tech’s Demise Remain Greatly Exaggerated

Despite its late-2018 pullback, the sector appears in fine fettle today—illustrating the risks of reacting to passing sentiment-driven trends.

Editors’ Note: MarketMinder does not recommend individual securities. The companies mentioned herein merely represent a broader theme we wish to highlight.

For years, many have treated Tech and Tech-like stocks[i] as the only thing sustaining the bull. Headlines hype FAANG[ii] fluctuations and treat daily Tech news as make-or-break for markets. So when the sector’s stocks tanked amid late-2018 volatility, folks feared they—and the bull—were running out of steam. We believe these concerns are too hasty. Recent Tech news highlights the sector’s strong fundamentals and the importance of looking past short-term sentiment swings.

Tech stocks ended 2018 on a sour note. As global stocks sunk during what we believe was a correction—a sharp, sentiment-driven decline of -10% to -20% or so—Tech underperformed, falling -22.8% between US markets’ most recent peak on September 20 and the correction’s low on December 24, trailing most sectors.[iii] Many blamed slowing global growth—particularly in China. There, folks fear US tariffs are sapping Chinese growth—dinging demand for Tech goods and services—and disrupting Tech firms’ supply chains. But when markets rebounded, Tech surged 19.6%, topping all sectors but Industrials.[iv] While not predictive, we think this highlights the perils of drawing large conclusions from short-term, largely sentiment-driven swings.

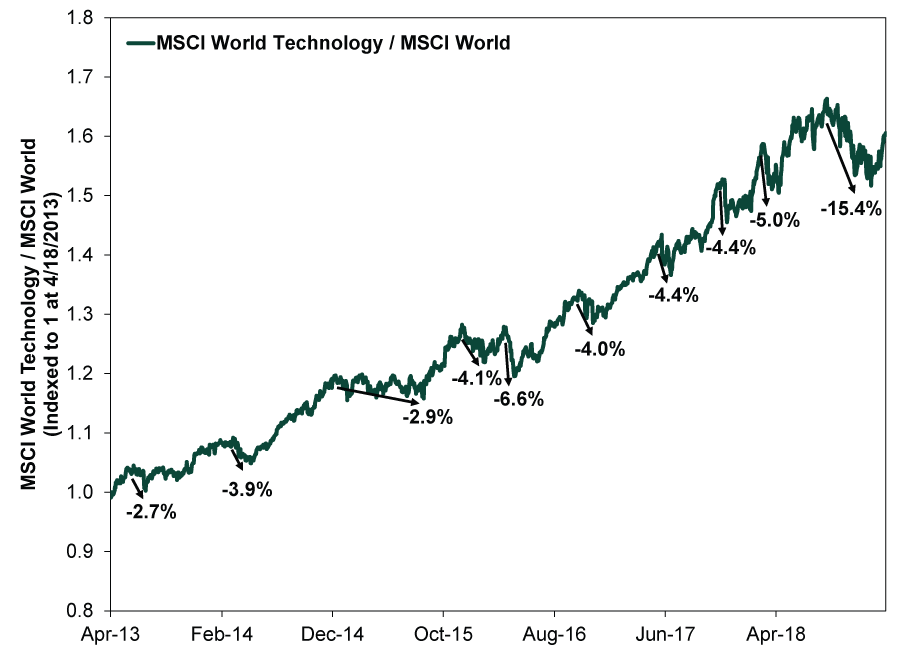

Brief shifts in leadership, whether tied to broad market volatility or no, happen regularly in bull markets. Case in point: Tech has mostly outperformed broader markets for years—but still lagged for several stretches along the way.

Exhibit 1: Tech Outperforming Overall, But Not All the Time

Source: FactSet, as of 2/13/2019. MSCI World Index return with net dividends and MSCI World Technology Index return with net dividends, 4/18/2013 – 2/12/2019. Series indexed to 1 at 4/18/2013, when Tech’s broad outperformance during the bull commenced. Tech is outperforming when the line is rising.

Throughout, media touted many reasons why Tech’s heyday was past—and why this threatened the bull. These included too-high valuations, narrow market breadth (meaning too few—mostly Techish—stocks driving overall markets higher, setting up pain for market returns when the party stopped), flagging investor enthusiasm for Tech firms and regulatory risk. Extrapolating from any would have proven an error. We think the same applies now.

Sadly, many investors react to short-term moves—a product of humans’ tendency to flee losses. One way to see this: Technology-sector linked ETFs experienced outflows throughout Q4, paralleling the sector’s recent underperformance.[v] While fund outflows miss what investors do with the proceeds, this suggests the sector’s Q4 woes rattled many. Such reactions often produce regret, as a correction’s worst performers frequently rebound fastest. This time, Tech, Energy and Industrials led the way down and back up.[vi]

Since leadership countertrends can come and go quickly, we believe the key question for investors isn’t, “How has (insert your choice of stock, sector or the overall market) done lately?” or, “What are headlines saying?” Rather: “How does sentiment compare to reality?” Applying this question to Tech, we think the sector’s fundamentals look robust presently—and sentiment, still skittish from Q4’s deep correction, seems far from overstretched. Instead, many apparent Tech headwinds—and alleged threats to the global expansion—appear overstated. Tariffs are relatively easy to sidestep and just 0.3% of global GDP (per IMF figures) if all threatened duties took effect at 25% rates. China is slowing, but gradually, in line with its years-long trend. With the government ramping up stimulus, a “hard landing” doesn’t seem any closer today. Global growth worries mostly seem a rehashing of Chinese slowdown fears, as folks fret contagion. However, we see plenty of data suggesting the global expansion is in fine shape.

Recent industry metrics also surprised to the upside. Take earnings beats with a grain of salt—companies routinely steer estimates down beforehand to boost the odds of exceeding them—but 83% of Tech companies have surpassed Q4 earnings expectations thus far, above most sectors.[vii] Business demand for cloud services—in which a company houses data and software on remote servers maintained by a third party—is strong, according to industry earnings reports.[viii] Many companies appear in the early stages of transitioning to these cloud services—a shift that bodes well for Tech companies’ future revenue streams and margins, in our view.

Semiconductor and computer chip production—which some consider a bellwether of Tech demand—also stirred worries after several chipmakers (e.g., Samsung, Intel and Nvidia) reported falling sales in Q4 and another (Micron) noted rising customer stockpiles.[ix] However, this isn’t necessarily predictive, in our view. Chip demand tends to come in bursts as major buyers—like cloud services providers—typically focus on finding customers to fill existing server capacity, then ramp up investment (and order more components, like chips) as they build new server facilities. Hence, reading into a soft patch seems mistaken to us.

So while many saw Q4’s volatility—and Tech’s weakness within it—as a sign the Tech-led bull was over, we suspect it is the latest in the sector’s series of headfakes. Market fundamentals—especially Tech’s—remain positive. Investors shell-shocked by recent volatility don’t seem to appreciate this yet. In our view, that is a sign more bull market lies ahead.

[i] Like those looped into the new Communications Services sector last September.

[ii] This is a popular moniker for Facebook, Apple, Amazon, Netflix and Google coined by well-known television personality Jim Cramer.

[iii] Source: FactSet, as of 2/13/2019. S&P 500 Total Return Index by sector, 9/20/2018 – 12/24/2018.

[iv] Ibid. S&P 500 Total Return Index by sector, 12/24/2018 – 2/12/2019.

[v] Ibid. Net share issuance for Technology sector ETFs, monthly, October 2018 – December 2018.

[vi] Ibid. Statement based on S&P 500 Total Return Index by sector, 9/21/2018 – 2/12/2019.

[vii] Source: FactSet Earnings Insight, as of 2/8/2019.

[viii] “Cloud-Computing Giants Keep Growing Despite Slowdown Fears,” by Matt Day and Jeran Wittenstein, Bloomberg, 2/5/2019.

[ix] “Samsung Logs Weak Fourth-Quarter Net Profit,” Timothy W. Martin, The Wall Street Journal, 1/30/2019.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

-

Expert Commentary This Week in Review | Energy Markets, Fed Meeting, Earnings Reporting

2026-03-20

2026-03-20 -

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today