Personal Wealth Management / Market Analysis

Searching for Meaning in ‘Quiet’ Times

Should stocks' recent "boring" streak worry investors?

By a show of hands, who finds recent market movements boring? If your hand is up right now, you aren't alone-many in the financial media agree. To us, stocks are stocks and there is pretty much always something interesting, but we'll grant that narratives about stocks can be boring. And news in August tends to hit a bit of a lull as families fit in that last vacation before school begins. That said, some pundits argue boredom will soon beget excitement of a bad sort, claiming stocks' historic sleepy streak portends trouble for markets soon. For investors, beware reading too much into short-term market movement: Recent stock bounciness (or lack thereof) means nothing for future direction.

Experts' divining meaning from short-term market movement isn't new-not this current market cycle, not ever. Back in May 2014, we dubbed this an attempt to search for meaning in bouncy times.[i] Two months later, that shifted to "uppy times[ii]." And of course, lots of folks attempted to find meaning in the couple days' swings around Brexit, the correction before that and even just assets trading similarly (oil and stocks, bonds and stocks). Now, in our view, all these analyses are much too myopic. Stock returns are variable, full stop. They come in unpredictable clumps, and currently, we are in a positive clump, even if that positivity isn't galloping every day. That's a good thing. However, analysts can't help themselves, arguing stocks are again too quiet today.

Specifically, some point out this has been the least volatile 30-day period in more than 20 years, with "volatile" defined as a daily move of +/- 0.5%. Others cite the CBOE's Volatility Index (commonly known as the VIX), near two-year lows, as another sign of market boringness. Some pundits view the lack of movement as a potentially ominous sign. Those concerns include certain assumptions, like a low VIX indicates market complacency-suggesting a spate of volatility is due. Another common media theory: Current market tranquility depends on central banks, which could quickly lose control should they shift monetary policy in a way markets dislike.

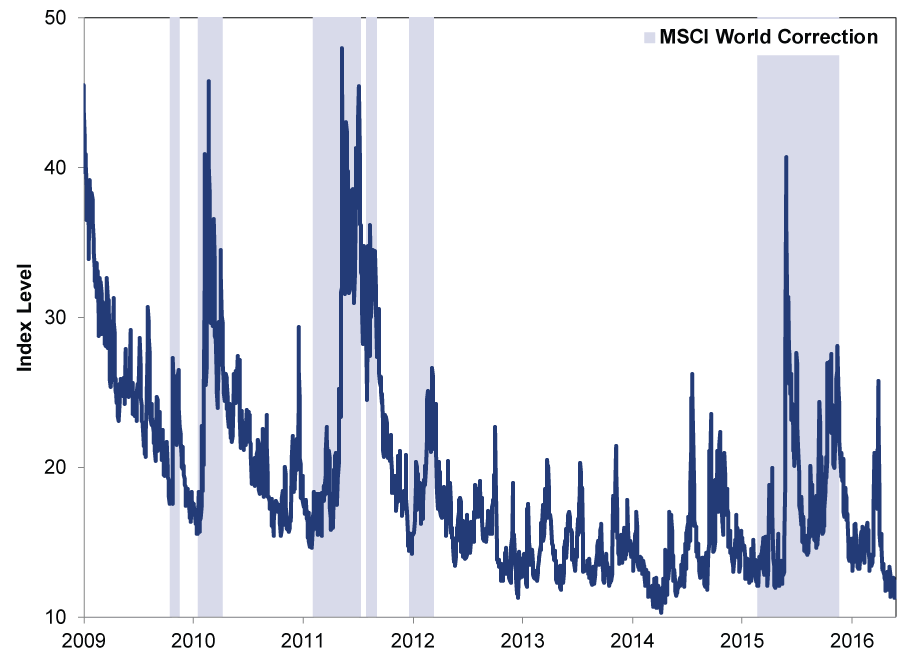

However, these analyses seem flawed. First, the VIX isn't predictive. Of anything. Dubbed the "volatility" or "fear" index, the VIX is an attempt to forecast upcoming volatility in the next 30 days by looking at S&P 500 option premiums. This presumes option traders possess some insight about future volatility, whether it's based on an upcoming event (e.g., Brexit) or some other intuition (e.g., "I feel like it's going to be volatile soon"). However, options markets don't possess more insight than others, as all liquid markets discount opinions and widely held information near simultaneously. One isn't more prescient than the other, making this theory bunk. That's evidenced by the fact the VIX hasn't exactly forecasted corrections (short, sharp, sentiment-driven drops exceeding -10%) in the bull market. (Exhibit 1)

Exhibit 1: VIX During the Bull

Source: FactSet, as of 8/23/2016. From 3/31/2009 - 8/23/2016.

There are some big spikes in 2010, 2011 and 2015-not surprisingly occurring during[iii] corrections-but there are also lots of other jumps accompanying regular market movement. More importantly, none of these moves, big or small, signaled the end of the bull.

As for the notion central banks are propping up equity markets, we humbly ask a couple questions. Like, if "easy" monetary policy is a boon to stocks, why aren't Japanese stocks the best in the world, given the BoJ's massive "Qualitative and Quantitative Easing" program? Why have US stocks led during the current bull market, even though the Fed not only ended its quantitative easing (QE) program but also actually hiked rates?[iv] These are just two examples, but they are counterpoints to the allegedly mystical powers of monetary policy for stocks.

Plus, for all the focus on today's "boring" market, it wasn't too long ago when many were freaking out about how volatile stocks were-which kind of makes you wonder exactly when these folks will be happy? (A global theme.) Let's take a stroll down memory lane and revisit two months ago. Remember the Friday[v] following the Brexit referendum result? Headlines screamed doom, Leave voters were having buyers' remorse and British markets were turbulent. The MSCI UK fell -3.1% that Friday and another -2.5% on Monday, June 27.[vi] Likewise, the MSCI World dropped -4.2% and -1.8%, respectively.[vii] Since that rough Friday, the MSCI UK is up 12.3% while the MSCI World gained 7.8%.[viii] The short spurt of negative volatility didn't prevent stocks from rising over the following two months.

We can take this back further, too. A year ago, markets were roiled by concerns about a potential Fed interest rate hike and China's currency devaluation. The widely watched yet broken index known as the Dow plunged more than 1,000 points after the opening bell on August 24 (finishing the day down 588 points). The MSCI World fell -4.3% that day, and panic seized investors. The negative volatility didn't immediately subside, either. After dropping further in September, global markets mostly recovered their losses by the start of December ... before the correction's final downdraft, which bottomed on February 11, 2016. Unlike several US indexes, the MSCI World has yet to register a new record high. However, it has made up its losses since those sharp pullbacks from a year ago. Since 8/24/2015, the MSCI is up 11.3%. From the bottom of February's correction? 18.6%.[ix]

For investors, this recent history lesson is a keen reminder of how quickly volatility-up or down-can strike (and subside). We suggest not reading too much into markets' current "calm." It could change tomorrow, or it could remain quiet for another several weeks. That's the thing about volatility: It's, well, volatile.

[i] A technical term.

[ii] See footnote i.

[iii] Note "during"-present tense. These sharp jumps didn't anticipate the correction, they occurred while it was happening.

[iv] Granted, it was probably the least surprising and meekest hike in the history of hikes. But still.

[v] Our fearless MarketMinder editors surely do!

[vi] FactSet, as of 8/24/2016. Daily move of the MSCI UK for 6/24/2016 and 6/27/2016.

[vii] Ibid., for the MSCI World.

[viii] Ibid. From 6/24/2016 - 8/24/2016.

[ix] Ibid. From 2/11/2016 - 8/24/2016.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Inflation Data, Currency Reset Risks, Commodity Opportunities and More– April 20262026-04-17

-

Market Analysis Foraging Through Japan’s February Data2026-04-17

-

Expert Commentary This Week in Review | Iran Conflict Update, Canada Election, UK GDP

2026-04-17

2026-04-17 -

Market Analysis An Economic Check In on the UK2026-04-16

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today