Personal Wealth Management / Economics

Strengthy Banks

A closer look at US banks’ balance sheets suggests the institutions are stronger than some rating agencies seem to believe.

A closer look at US banks’ balance sheets suggests the institutions are stronger than some rating agencies seem to believe.Photo byCentral Press/Getty Images.

The annals of odd ratings agency moves got a bit fatter Friday, when Moody’s threatened to downgrade some of the biggest US banks. Not because balance sheets are shaky now—but because the government seems more apt to let them fail if they ever get in trouble. To each their own, we suppose, though it seems weird for banks to get dinged for this when most other big US firms don’t lose points for lacking a government backstop. Moreover, US bank balance sheets are pretty darned healthy. US Financials are profitable and flush with cash, and US Financials stocks face fewer headwinds now than at any point in recent years, regardless of what the raters say.

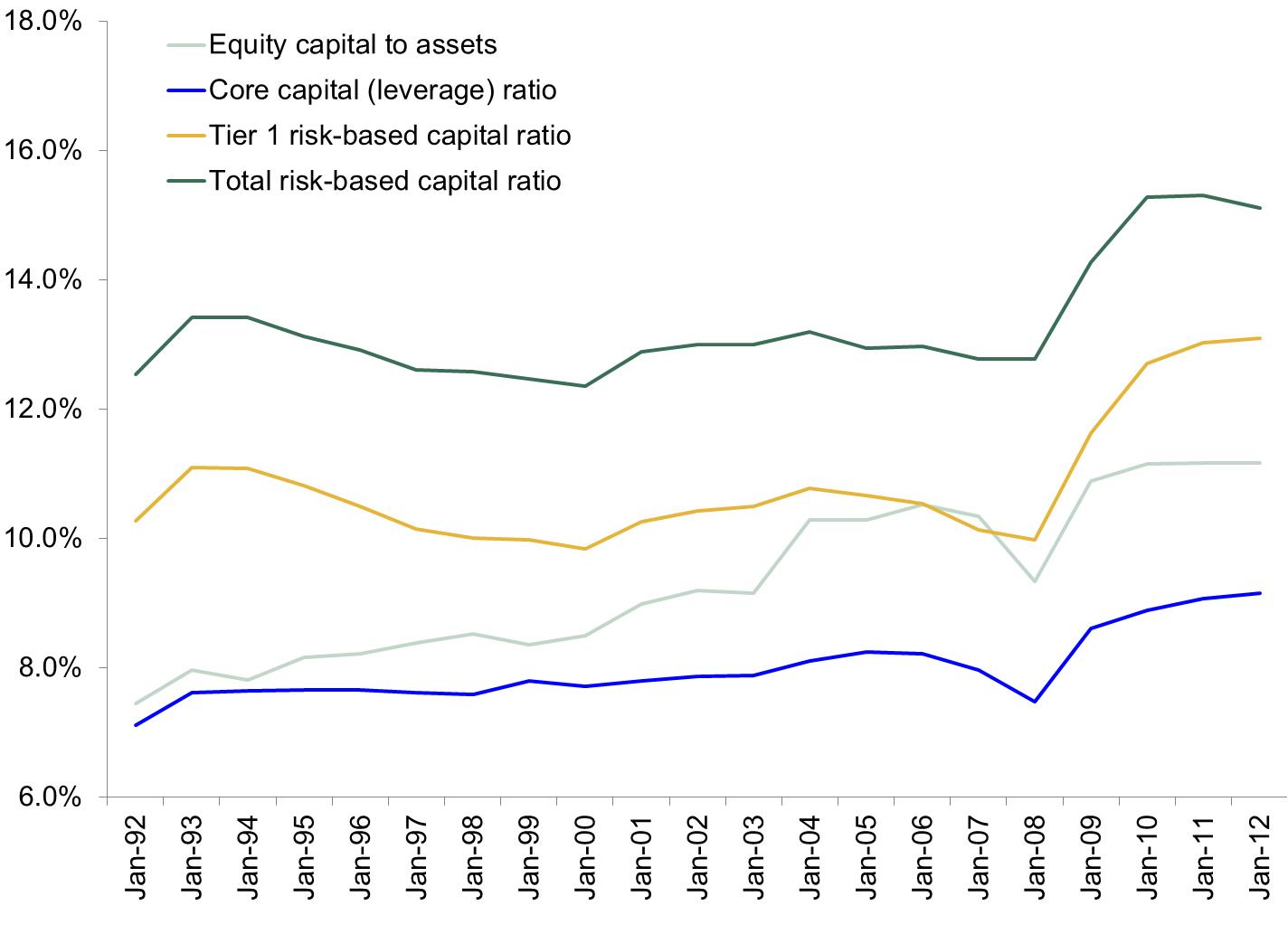

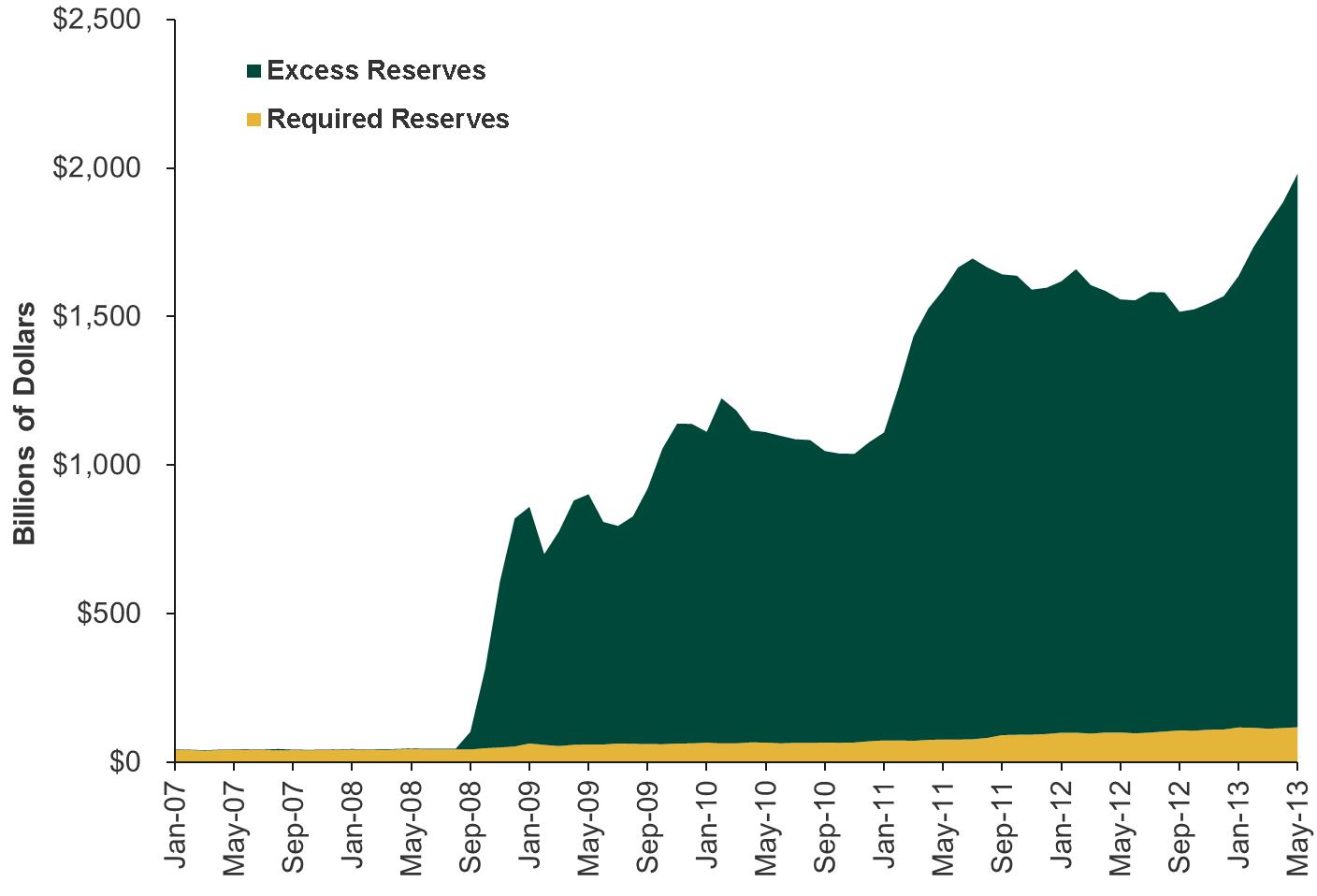

By most measures, US banks are the strongest they’ve been in decades. Regulatory capital ratios are at or near all-time highs (Exhibit 1). Excess reserves have jumped from $1.87 billion (with a b) in August of 2008 to $2.03 trillion (with an r... and a t!) in July (Exhibit 2).

Exhibit 1: US Banks' Regulatory Capital Ratios

Source: FDIC, as of 8/23/2013.

Exhibit 2: US Banks' Excess Reserves

Source: Thomson Reuters, as of 8/23/2013.

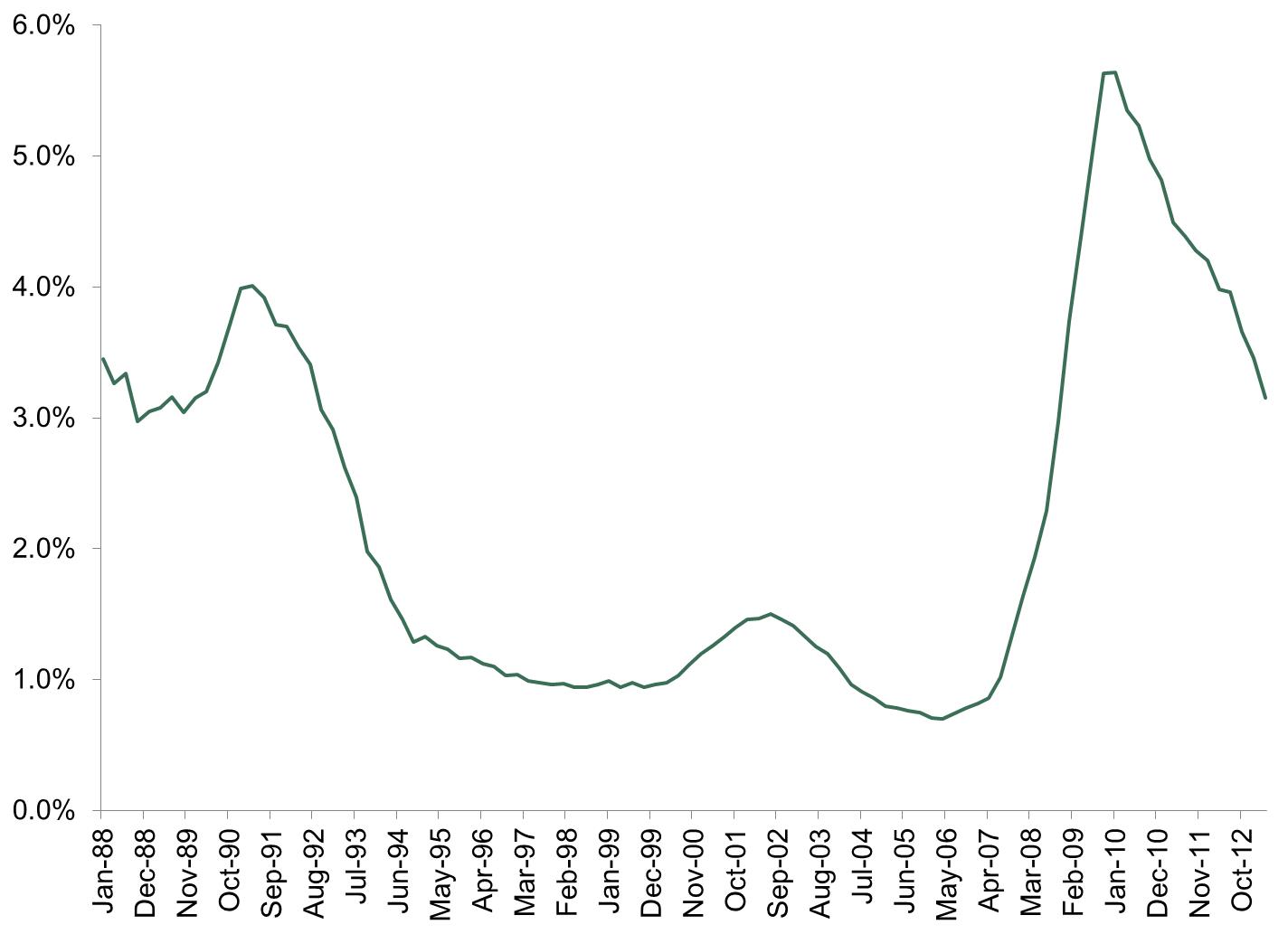

With such big buffers, banks seem well-equipped to absorb potential losses and weather deposit outflows. Not that they’ll need to any time soon, though. Nonperforming loan ratios are way down from 2010’s peak (Exhibit 3).

Exhibit 3: US Banks' Nonperforming Loan Ratios

Source: Federal Reserve Bank of St. Louis, as of 8/26/2013.

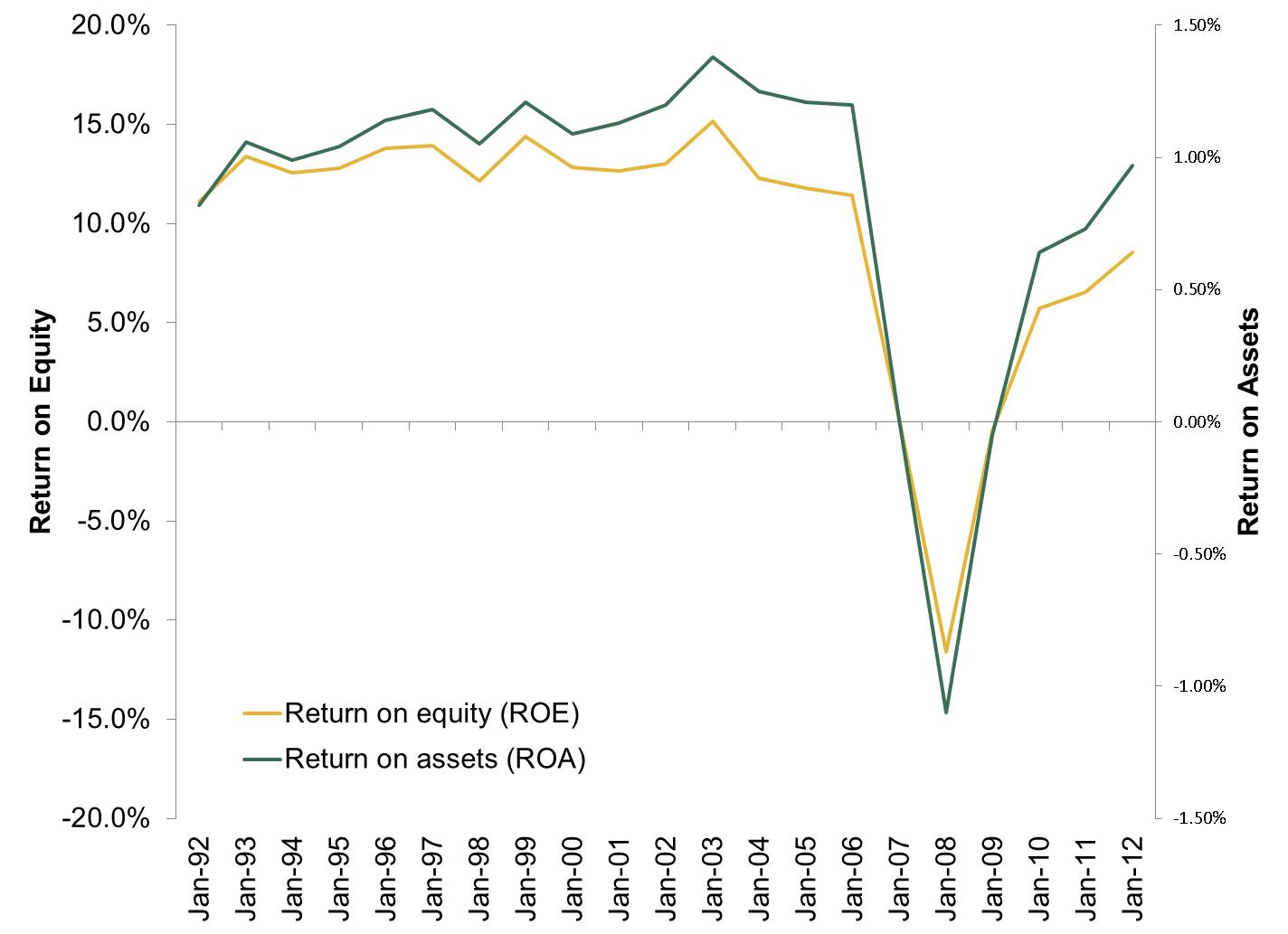

Banks are also quite profitable. Financials earnings surged 28.1% y/y in Q2, with 79% beating estimates. Granted, growth rates were skewed by some big, one-off losses in 2012, which made the y/y comps easy to beat, but easy comps aren’t solely responsible for earnings growth. Revenues were up big, too—7.1% y/y. Other measures, including return on equity and return on assets, also show improving profitability (Exhibit 4).

Exhibit 4: US Banks' Returns on Equity and Assets

Source: FDIC, as of 8/23/2013.

Looking ahead, Financials earnings should keep growing. Net interest margins are starting to widen as long rates increase, making future lending more profitable. This should keep up as the Fed starts tapering (and eventually ends) its quantitative easing program, giving banks incentive to lend more aggressively. As banks lend more at higher margins, profitability should improve further.

That’s true even with higher regulatory capital requirements taking effect in the coming years. Many banks are already capitalized above and beyond Basel III requirements. Some speculate the Fed’s decision to impose higher leverage ratios on the biggest banks will weigh on lending, but the eight qualifying banks don’t have a huge shortfall. They also have five-and-a-half years to meet the higher threshold, and they should be able to get there by retaining earnings. The likelihood they need to issue new equity or cut lending to comply with tougher standards appears slim to none.

As these regulatory and other jitters fade, Financials stocks should feel some nice tailwinds. Sure, the sector isn’t without risk—no category is—but overall and on average, US banks are moving past the issues plaguing them in recent years and likely beat too-dour expectations.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Bourse : pourquoi l’impact de la guerre en Iran sera moins important que prévu – par Ken Fisher2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 4/1/2026

New to Fisher? Call Us.

Contact Us Today