Personal Wealth Management / Financial Planning

Targeting the Wrong Objective

While the SEC mulls whether target-date funds require more disclosure, there is a much bigger flaw in these investments.

According to a recent survey of 401k participants investing in target-date funds (TDFs), 56% believe they’ll be able to meet their retirement goals—a 15 percentage-point spread over workers who don’t use TDFs. But in our view, the TDF investors may have fallen prey to a myth and have a false sense of retirement-investing security as a result. While TDFs may seem appealing, we believe they aren’t a blanket solution—a position we aren’t alone in, it seems. The SEC is mulling over requiring TDFs to display more detailed and easier-to-understand depictions of their approach. Further disclosure would provide investors with more information—a positive, in our view. But this doesn’t change the fundamental flaw in target-date funds: Automated, cookie-cutter asset allocation tweaks based on a targeted calendar year run the risk of not reflecting your long-term goals.

Target-date funds—mutual funds often dubbed “Retirement” and a year (e.g., “Retirement 2025”)—have grown in popularity as a retirement investing tool, stemming from their seemingly easy, straight-forward approach. Invest your money in a TDF, and it will automatically adjust your asset allocation—the mix of stocks, bonds, cash and other securities—over time, based on your planned retirement date. Each TDF has a “glide path” that determines when the fund’s asset allocation changes.

For example, if you’re 40 right now and you plan to retire at age 65, your asset allocation might initially start at 80% stocks and 20% bonds. In 5 years, it may readjust to 70% stocks/30% bonds, in 10 years 60%/40%, etc. Theoretically, you “set it and forget it” and by the time you reach the targeted year, your allocation will have been tweaked to boost bonds and reduce stocks. The sales pitch argues you should just pick a TDF dated around your desired retirement year, and the deed is done.

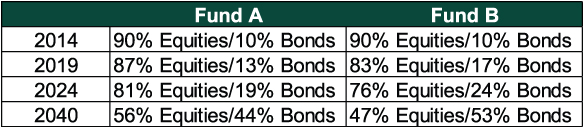

Though the concept may seem logical, these funds are some of the least-understood investments on the market. For example, the difference of one preposition (“to” vs. “through”) is a subtle but crucial distinction. A “to retirement” TDF will be constructed very differently than a “through retirement” TDF. The former ratchets down its equity allocation more quickly before reaching its lowest point in the target year. The latter is theoretically built to meet the needs of the investor throughout retirement, so it glides down more slowly—and keeps reducing equity exposure after the target year. Glide paths differ from fund to fund and company to company, even if the target year is the same. For example, consider two different through-retirement TDFs, both with a target date of around 2040.

Exhibit 1: Comparison of Two 2040 Through-Retirement Target-Date Funds

Asset allocations are approximations. MarketMinder does not recommend any specific companies or funds; rather, they are listed here for illustrative purposes only. You can see these allocations here.

It may seem like just a few percentage points’ difference over each year, but over time, the differences in allocation can materially affect expected risk and return characteristics—even though the target date is the same.

In an effort to add clarity, the SEC has reopened the public comment period on its 2010 TDF regulations. The proposed rule would require a TDF’s target date be more prominently displayed on marketing materials, visuals depicting a TDF’s glide path, disclosures about how investments aren’t guaranteed and any changes in the fund, among others. The SEC’s Investment Advisory Committee has additional suggestions for rulemaking, including disclosing fund risk and changes in management strategy, publishing regular updates based on recent market experience and revising fee disclosure requirements to show fees’ impact on returns. Giving investors additional info would be a plus, and no small one at that. But more disclosure, however much, won’t change TDFs’ inherent flaws—particularly in arbitrarily shifting asset allocation.

TDFs’ alleged appeal is also their fatal flaw. There is no one-size-fits-all solution for determining your portfolio’s asset allocation—in our view, the most important determinant in a portfolio’s return. Studies have shown asset allocation can be responsible for as much as 90% of your long-term portfolio return—whether it’s exactly that figure or some similar figure isn’t our point. Rather, there is ample evidence this decision will play a big role in determining whether you reach your goals or not.

And that brings us to another flaw: TDFs revolve around your retirement date, but in doing so, they may ignore your actual goals and time horizon, which rest on many factors far more nuanced and unique to you. Retirement means many different things to many different people. Let’s say two investors planning to retire in 10 years purchase the hypothetical “Retirement 2025” TDF. Will it actually let them retire in 2025 with reasonable confidence their savings will meet all their needs? What if one investor is 49 and has a 39-year-old spouse while the other investor is 62, single and aiming for retirement at 72? If the fund they buy is a “through retirement” TDF, should they be weighing potential differences in needed cash flows? What if two investors are the same age but have very different health? What if one investor plans to leave the remainder to his or her heirs, while the other has no heirs and wouldn’t mind if his or her last check bounced? These are vastly different goals and objectives—and no one product can hit all of these needs for everyone. The hypothetical fund “Retirement 2025” doesn’t target your unique retirement that you may or may not commence in 2025—it targets a specific year.

Your life savings deserve much more hard analysis than this, in our view. No matter what the long-term financial goal is—a comfortable retirement or a gift for family, for example—confidently buying a TDF and hoping you’ll glide your way to or through your golden years is just too simplistic.

4 Ways to Avoid Running Out of Money During Retirement

To investors who want to retire comfortably. Download the guide by Forbes columnist and money manager Ken Fisher's firm. It's called "The 15-Minute Retirement Plan." Even if you have something else in place right now, it still makes sense to request your guide! Click Here to Download!

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News What ‘IPO’ really stands for — and whether you should be buying SpaceX and the AI giants2026-06-23

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-23

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US PCE Inflation, Annuities

2026-06-22

2026-06-22 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 15 - June 192026-06-22

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today