Personal Wealth Management / Market Analysis

The Case for Stocks Outside America

Don’t let US stocks’ recent leadership persuade you to ditch the rest of the world.

Last week, financial media were abuzz over US stocks’ bull market record. Amid the cork-popping, though, headlines made a few jabs at other major developed countries’ stock markets. The latter have broadly lagged the US this year—and have done so overall in this bull market—leading some to conclude all the action is in America. Others look askance at stocks outside America and question the upside of global diversification. In our view, however, recent US leadership actually reinforces these benefits. A look at this whole bull market indicates country and regional leadership rotation is still very much a thing, and we don’t believe investors benefit from ditching recent underperformers.

Since this bull market began on March 9, 2009, US stocks have returned 418%, while developed markets outside the US have managed “just” 179%.[i] Media coverage of the gap highlights seemingly plausible reasons for it. For the US, coverage cites faster GDP growth, last year’s tax reform supposedly goosing economic activity,[ii] rapid earnings growth, a faster recovery from the 2008 – 2009 recession, Tech sector strength (since US markets tilt more towards this sector), plus some good old-fashioned American ingenuity and entrepreneurialism. For the rest of the developed world—especially the eurozone—headlines tend to fret lingering crisis-era weaknesses, ascendant populist and anti-euro politicians, Brexit, slower GDP growth and more. All this seemingly vindicates the US-only approach many American investors favor.

However, this approach ignores the fact leadership rotates—both in terms of overall bull market returns and within a bull market itself. The latter holds in this bull market, despite the media’s insistence on US perma-superiority.

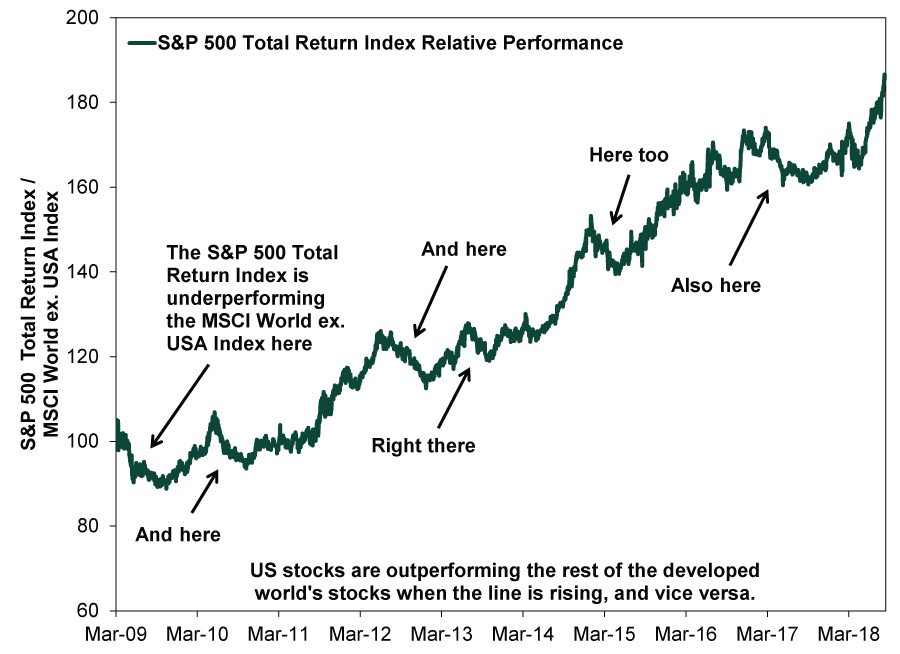

Exhibit 1: US Stocks Lead Sometimes, Not Other Times

Source: FactSet, as of 8/27/2018. S&P 500 Total Return Index and MSCI World ex. USA Index return with net dividends, both in USD, 3/9/2009 – 8/24/2018. Indexed to 100 at 3/9/2009.

While the line in Exhibit 1 slopes up and to the right most of the time, signaling US stocks’ cumulative leadership, there are also plenty of times they didn’t. Take 2017, for example—early in the year, media made much of an (in our view, fictitious) Trump Rally/Trump Bump/Trump Trampoline.[iii] Yet during that time (and for most of the year), major stock indexes elsewhere in the world led. Or what about 2012, when the eurozone was in the throes of a regional recession—one the US avoided. But as Exhibit 1 shows, the US-listed stocks trailed from June – December of that year. Even further back: US markets lagged the rest of the developed world from the bull’s start through September 9, 2011—30 months later. In our view, the awesome power of hindsight shows the folly of extrapolating the most recent (or any) leadership trend blindly into the future.

We aren’t saying it is impossible to assess the likelihood one country or region fares better. But doing so requires more than projecting recent outperformance forward, which smacks of heat chasing. It actually takes more than tracking (perceived) fundamental factors. More meaningful and worth watching, in our view, is how fundamentals match up with sentiment in the US versus the rest of the developed world. As noted at the outset, headlines presently tout US economic strength and highlight weakness elsewhere. We could quibble with aspects of each, but more importantly, we think this analysis errs by discounting sentiment’s role. A massive omission! In our view, stock movements over the next 3 – 30(ish) months primarily hinge on the (ever-shifting) gap between reality and expectations. More optimism means reality has a higher hurdle to clear to positively surprise investors. Less optimism can mean more positive surprise. Presently, we think sentiment is warmer in the US relative to fundamentals than in many other major developed economies, particularly the eurozone.

The argument for global diversification goes beyond this or that market forecast, though. You may believe—with plenty of solid evidence—certain countries are poised to power higher. But what if you are wrong? (Which happens to the best of investors, by the way. A lot.) All countries have their days in the sun and rain—sometimes for extended periods. Shunning certain countries boosts the risk of missing out if/when the clouds part. Another reason to spread your portfolio worldwide: US stocks represent just 55% of global stock market capitalization.[iv] Ignoring abundant investment opportunities elsewhere makes little sense, in our view.

It is possible US markets don’t turn the floor over to other developed country markets just yet. But we suspect a prolonged stint of US underperformance is likely ahead, leaving your portfolio in the doldrums and your brain itching to chase recent winners. Hence our view that global diversification is essential for long-term investors. It may not feel great when markets in one part of the globe are making others look bad. But over the long haul, we believe it pays off handsomely and helps avoid dangerous investing pitfalls.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Chart of the Day: Oil’s Substitution Effects, Illustrated2026-06-03

-

Economics Rising Credit Card Delinquencies in Context2026-06-02

-

Market Insights Ken Fisher on Inflation, Sell America, US National Debt and More - June 20262026-06-01

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US Jobs, Estate Planning

2026-06-01

2026-06-01

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today