Personal Wealth Management / Market Analysis

The ECB Hike-Inspired Table of the Day

Another perspective on rate hikes and returns.

As the world mourned the passing of Her Majesty Queen Elizabeth II Thursday, markets did what they always do at such times: got on with the job. In a way, it is a fitting tribute to the steadfast woman who exemplified this attitude during her remarkable 70 years on the throne. Yet a stiff upper lip doesn’t quite describe the way headlines reacted to the day’s biggest financial news: the European Central Bank’s (ECB’s) decision to raise its benchmark interest rate by 75 basis points (0.75 percentage point) from zero to 0.75%. There was much chatter about the tricky position the bank finds itself in as the eurozone economy seemingly teeters on the brink of recession as inflation accelerates. Most agreed rate hikes won’t do much on the inflation front and raised the likelihood of an economic downturn. Perhaps both of those prove true—and perhaps not. We have written at length about what rate hikes can and can’t do in this environment, and there is mounting evidence that inflationary forces outside central banks’ control are starting to turn, albeit to varying degrees in various regions. And, crucially, there is also evidence the broader fallacy underlying these fears—a mantra known as Don’t Fight the Fed—is as off-target now as ever.

Don’t Fight the Fed—which may as well be Don’t Fight Central Banks[i]—holds that stocks should generally party when monetary policymakers are cutting rates and struggle when central banks are hiking. This year, it might even seem to hold true, given central banks have tightened during a bear market, which is typically a prolonged decline of -20% or worse with a fundamental cause. To us, this bear market seems much more sentiment-driven, with about eight different issues weighing on investors’ minds. Rate hikes are one of those, so from that standpoint we will concede they bear some blame. But that doesn’t mean rate hikes—even big ones—are negative from a fundamental standpoint.

We generally don’t like looking to short-term returns to prove a point, as they are myopic and happen for any or no reason. Yet we also think it is fair to presume that if rate hikes were fundamentally bad for the economy or stocks—the bear market’s trigger—we would see a consistent pattern of negative returns in their wake. Thing is, we haven’t.

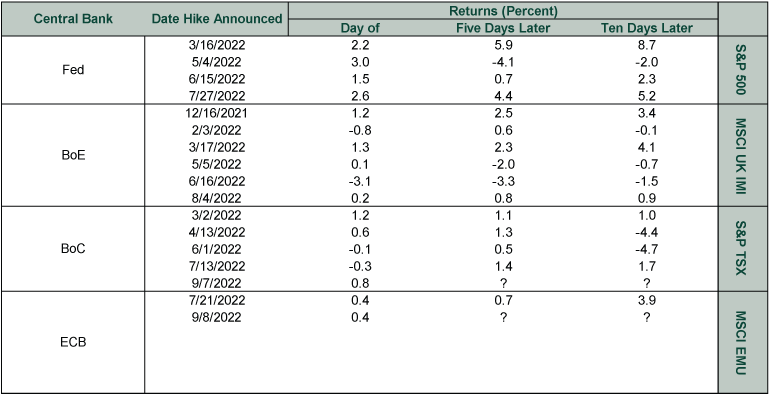

Exhibit 1 shows returns immediately following major central banks’ rate hikes this year (in local currencies to avoid skew from currency swings), and as you will see, they have been positive much more often than not. Returns on the day of the announcement were up 13 of 17 times, a 76% frequency of positivity. After five trading days (a week, give or take the occasional holiday), returns were positive 12 of 15 times, an 80% frequency. Positivity was less common after 10 trading days, but stocks were still up more often than not at 9 of 15 times, or 60%.

Exhibit 1: Rate Hikes and Returns

Source: FactSet, as of 9/8/2022. S&P 500 total returns in USD, MSCI UK IMI total returns in GBP, S&P TSX Composite total returns in CAD and MSCI EMU Index returns with net dividends in EUR, from market close the date before each rate hike announcement through the following 1, 5 and 10 trading days. Currency fluctuations between the US dollar and pound, Canadian dollar and euro may result in higher or lower investment returns.

Now, we realize that as the longer-term returns surrounding these rate hikes were negative, the shorter-term resilience is probably cold comfort. But we show you these figures to help frame your perspective moving forward. There remains a consensus view that for as long as central banks are raising rates, a new bull market can’t get underway. That is leading to some general gloom as policymakers on both sides of the Atlantic jawbone about more rate hikes to come. In our view, stocks’ lack of consistent negativity after rate hikes argues against this. It suggests the fear of the thing had a bigger bite than the thing itself, which is in keeping with the long history of rate hike cycles and stocks. This year, we think this speaks to how disconnected sentiment has become from reality. Falling uncertainty, regardless of what central banks do from here, is probably all stocks need to climb again.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics The Tenth Question Facing Alberta2026-08-06

-

Market Analysis Western Oil and Gas Producers Are Ramping Up2026-08-06

-

Corporate Information How You Benefit from Fisher Investments' Transparent Fee Structure

2026-08-04

2026-08-04 -

Corporate Information How Fisher Investments' High-Touch Service Helps You2026-08-04

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today