Personal Wealth Management / Economics

The Global Economy Is Growing at Now, Now

May's data show a blooming world economy.

Stocks have jumped higher to start this week, which is leaving our skeptical media grasping at straws trying to figure out what is behind the gains. Many seemingly settled early this week on Tuesday's strong US housing data. First, we caution investors from speculating about daily market movements due to any specific piece of news[i]-markets are far too complex to pinpoint an up or down day based on a single report. But among all the datasets out there, real estate is even more limited, given its small slice of the total economy. However, for you number munchers, fret not! May has provided a bounty of growthy data to enjoy.

First, let's start in the good ol' U-S-of-A. After Q1 GDP missed expectations in last month's release, May's news has been more upbeat. April industrial production (IP) rose 0.7% m/m, halting a two-month slide. Though mining output fell -2.3% m/m-reflecting Energy's long-running struggles-Utilities, bolstered by cooler weather, rose 5.8% m/m after falling the prior two months. Moreover, Manufacturing rose 0.3% m/m, bouncing back from March's -0.3% dip. Though this noisy gauge continues bouncing around, weak Mining has had an outsized impact on the headline figure. The more representative Manufacturing, which comprises nearly three quarters of IP, has steadily climbed throughout this expansion.

Elsewhere, April retail sales rose 1.3% m/m, the biggest monthly rise in over a year. Led by auto sales (3.2% m/m), growth was pretty broad-based, with food and clothing sales both up. Even gas station sales-a longstanding weak spot due to plummeting gas prices-rose 2.2% m/m thanks to oil prices' recent rebound. As always, we suggest investors refrain from reading too much into one monthly report, good or bad-especially since retail sales don't include services, a large swath of overall consumer spending. However, it does counter overly dour concerns about the US consumer's health. Finally, the April Institute for Supply Management's Purchasing Managers' Indexes (PMIs) for both manufacturing and non-manufacturing topped 50-50.8 and 55.7, respectively. Readings above 50 indicate growth, and more importantly, the New Orders subindexes for both gauges suggest continued expansion is likely.

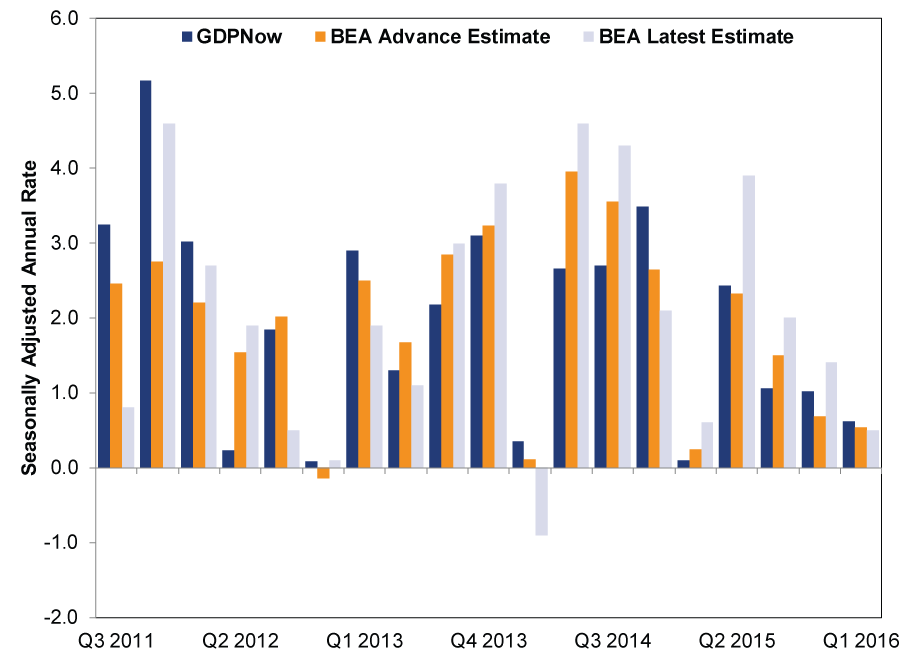

However, most folks seem preoccupied with GDP, with plenty of speculation about Q2's number. In particular, the Atlanta Fed's "GDPNow" and the New York Fed's "Nowcast" have garnered a lot of attention and analysis. These "nowcasts" attempt to provide an up-to-date estimate of GDP based on all available economic data-a rough live stream of growth, if you will.[ii] The latest read from the Atlanta Fed's gauge after Thursday morning's advance report on durable goods orders and shipments estimated Q2 2016 growth at 2.9%. Which seems dandy to us. However, there are multiple shortcomings with this approach. For one, though the sample size is small (the NY Fed's Nowcast just started about a month ago, while GDPNow goes back to Q3 2011), the predictive power isn't evident.

Exhibit 1: It's Hard to Forecast GDP

Source: Atlanta Federal Reserve and Bureau of Economic Analysis, as of 5/25/2016.

By our count, GDPNow overestimated the BEA's first estimate 10 times and underestimated 9 times-basically a coin-flip, and never spot-on. Moreover, it missed, sometimes badly, on future, revised estimates. Now don't get us wrong-we aren't criticizing GDPNow or the Nowcast for failing to hit the mark. Rather, for investors, we don't see their value. As James Hamilton of Econbrowser points out, the Atlanta model uses lagging data to make its forecast, while the New York model starts, "with a forecast of overall economic activity based on the best current assessment of overall activity." In other words, both use the past to make a forward-looking call. Though we understand the appeal of more timely economic data-after all, we are at now, now-nowcasts are essentially estimates of estimates, since they compile data (that get revised) to make a forecast about another dataset (that also gets revised). When considering GDP's significant limitations, a nowcast just isn't very helpful in gauging the future. Instead of looking to the past, we suggest consulting forward-looking indicators, like The Conference Board's Leading Economic Index (LEI). LEI rose 0.6% m/m in April and remains in a long uptrend-strong evidence against recession worries, given no US recession has occurred when LEI was high and rising.

Beyond the US, the rest of the world is largely growing, too. Across the Atlantic, the eurozone has grown for 12 straight quarters (0.5% q/q, 2.1% annualized in Q1), outpacing Japan, the UK and the US. We don't necessarily expect that trend to continue, but it does toss cold water on the many worries about the 19-member bloc. Germany, the region's strongest economy, reported Q1 growth of 0.7% q/q, up from 0.3% in Q4 2015. Moreover, the eurozone's flash composite PMI for May posted a 52.9, indicating more businesses grew than contracted, and its LEI was up in April-extending its uptrend.

In the UK, "Brexit" dominates all conversation, with pundits and pols alike warning uncertainty over the upcoming referendum is knocking growth. Yet the evidence for this is scant, and the actual data dispute it. Retail sales volumes rose 1.3% m/m in April, and though the dataset is limited since it only tracks sales of goods (not services), it's a counterpoint all the same. Even Japan, the developed world's weakest link in the last couple of years, avoided recession in Q1, growing 1.7% annualized. (Though this growth is not as strong as the headline figure appears, as it is underpinned mostly by government spending and calculation quirks.)

Growth isn't the domain of the developed world, either. Though some spots like Brazil-and its hectic political scene-are struggling, others are growing along just fine. For example, Brazil's northern neighbor, Mexico, grew 0.8% q/q (3.3% annualized) in Q1, buoyed by consumer spending. Plus, April data from much-maligned China show the world's second-largest economy continues growing at a slower, yet still robust overall, pace.

While most headlines bicker about political uncertainty, monetary policy and other false fears, the global economy continues chugging along. As we approach the year's halfway point, we understand why investors may be frustrated-flattish markets can do that. However, with global growth largely underappreciated overall, we are optimistic the bull will continue rising higher for the foreseeable future-especially if investors start noticing the better-than-appreciated reality.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Insights Ken Fisher on Inflation, Sell America, US National Debt and More - June 20262026-06-01

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US Jobs, Estate Planning

2026-06-01

2026-06-01 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 25 - May 292026-06-01

-

Market Analysis Big Gas Price Jump, Still a Small Spend2026-05-29

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today