Personal Wealth Management / Economics

The Hints About Stock Leadership From Q2 US GDP

GDP is backward looking, but we think this week’s report hints at the trends that lie ahead.

Thursday, the Bureau of Economic Analysis (BEA) reported US Q2 GDP growth accelerated to 6.5% annualized, putting output 0.8% above Q4 2019’s pre-pandemic high.[i] Yes, the US economy, by this measure, is officially out of the recovery phase and into expansion. Most coverage honed in on the disappointing headline figure (expectations ran north of 8% annualized) and whopping 11.8% growth in consumer spending (the second-fastest rate in nearly seven decades, trailing only Q3 2020’s 41.4% pop). While all this is backward looking—and the details therefore not of major importance to forward-looking stocks—we think the report does hint at the trends that likely lie ahead.

The sources of headline disappointment aren’t too concerning, in our view. Private inventory depletion knocked -1.1 percentage points off annualized GDP growth, residential real estate investment subtracted half a point, trade detracted -0.4 points and declining government expenditures took it down another -0.3 points.[ii] Let us take each in turn. First, businesses’ drawing down stockpiles shouldn’t be surprising. Well-known supply chain bottlenecks make stocking warehouses challenging, but firms globally are working to fix—or adapt to—them. This is a case where inventories are falling because demand is up, not because companies are cutting back. Lack of housing inventory may be holding back new home sales, but again, that seems mostly temporary. It may take a while for builders to ramp up due to the aforementioned supply chain issues, but the demand is there—as evidenced by soaring prices. We suspect the supply to meet it will follow.

Meanwhile, although net trade subtracted from GDP growth, that is because imports rose more than exports. Rising imports signify higher demand, which is why we think it is more helpful to look at total trade. It rose, signaling broad economic strength. As for dwindling government spending, stocks care mostly about the private economy—whether federal outlays rise or fall doesn’t really impact them much.

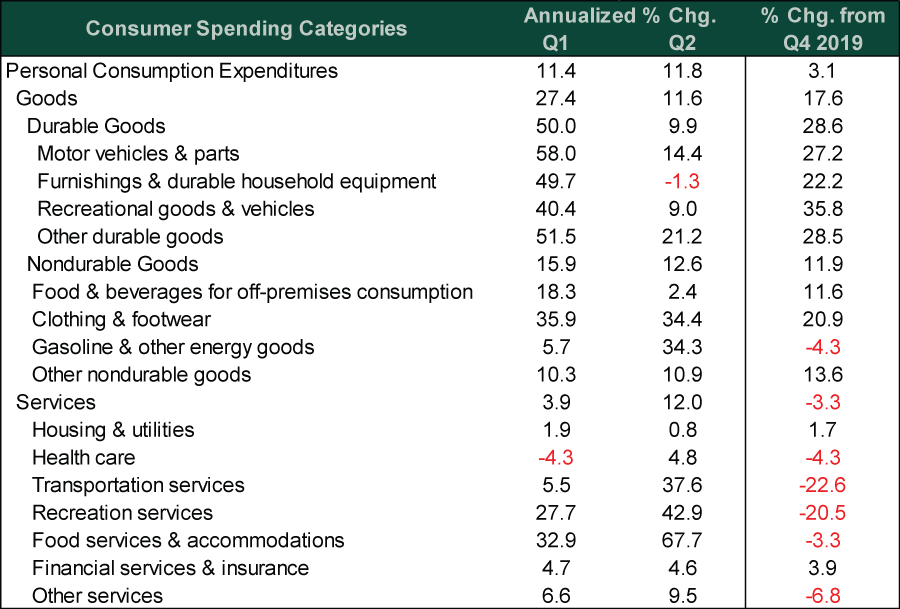

We think consumer spending, which comprised 70.6% of GDP in Q2, offers the most insight for investors in Thursday’s report.[iii] Within personal consumption expenditures (PCE, the BEA’s technical name for consumer spending), services—the lion’s share—grew 12.0% annualized, outpacing goods’ 11.6%. (Exhibit 1) Note the direction: Services PCE growth in Q2 more than tripled Q1’s 3.9% annualized rate, whereas goods’ growth rate more than halved from Q1’s 27.4%. Durable goods saw the steepest deceleration, from Q1’s 50.0% annualized growth to Q2’s 9.9%.

Exhibit 1: Most Consumer Spending Categories Now Exceed Pre-Pandemic Levels

Source: FactSet, as of 7/29/2021.

We think there are some interesting nuggets to glean about reopening’s economic impact. As you can see in Exhibit 1, goods tied to areas that reopened earlier this year, including cars, RVs and home furnishings, saw big booms and quick decelerations. Now services, which reopened later, are booming. But goods’ trajectory suggests these categories (e.g., travel, recreation and dining) will decelerate before too long. You can also see this reopening effect in line items like clothing and gasoline. With the return to offices—and commutes—happening alongside services’ reopening, apparel spending kept up a blistering pace, 34.4% annualized growth in Q2, just slightly off Q1’s 35.9%. Gas station sales growth raced to 34.3% last quarter from 5.7% prior—partly from higher prices and partly from higher demand. If ever you needed evidence that high gas prices don’t knock consumer spending, we reckon this report is it.

Stocks, though, are already looking past the reopening boom. With only a handful of subcategories’ output still below pre-pandemic levels—concentrated mainly in transportation and recreation services—the initial reopening rebound is probably mostly behind us. With slower GDP growth likely ahead, economically sensitive value stocks’ returns are wilting relative to growth stocks. On a sector basis, value-heavy Financials and Energy, which led early in the year, are now lagging as markets have seemingly already priced the factors that propelled their growth in Q2. For example, while gasoline demand surged in Q2—and Energy companies’ profits with it—Energy has been flat since March’s end and underperforming the S&P 500.[iv]

In contrast, with economic growth likely set to subside, big, global companies with revenue streams not tied to the economic cycle appear to be faring better, which we expect to continue. Tech and cloud-based platforms in Communication Services and Consumer Discretionary have led stocks higher since mid-May. In a late-stage bull market, which we think stocks are in, high-quality growth stocks should outperform, just as they have since last year’s bear market, intermittent countertrends notwithstanding. Slower growth may not be the most exciting outlook, but it is one that suits the bull market—and ongoing growth leadership—just fine.

[i] Source: BEA, as of 7/29/2021. Real GDP, Q4 2019 – Q2 2021.

[ii] Ibid. Contributions to Percent Change in Real GDP, Q2 2021.

[iii] Ibid. Real PCE as a percentage of Real GDP, Q2 2021.

[iv] Source: FactSet, as of 7/29/2021. Statement based on S&P 500 Energy and S&P 500 total returns, 3/31/2021 – 7/28/2021.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today